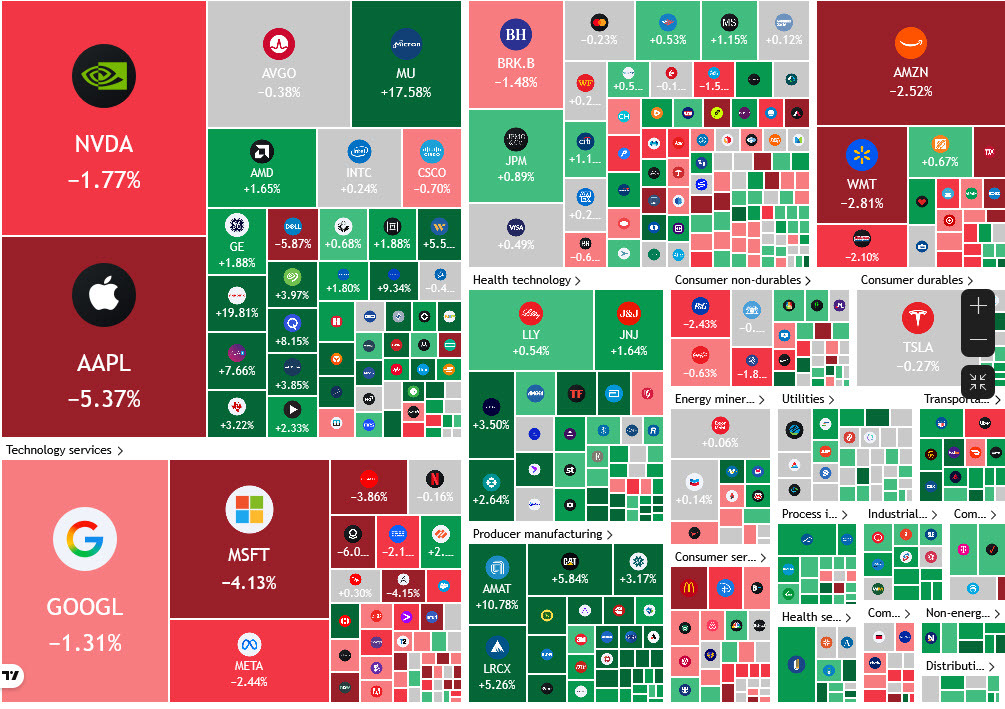

Greg wrote a great post about the technicals for megacap tech and how they're a problem. All of Nvidia, Alphabet, Meta, Microsoft, Apple, Amazon and Tesla are looking tired.

When you zoom out and look at the market heatmap today it's a completely bifurcated market where the largest companies in the world are struggling and smaller ones are climbing. This is a result of the megacaps spending all of their free cash flow on products from the suppliers, and often at huge markups. It's a win-at-all-costs war for AI and shareholders are starting to get fed up.

This is a problem. I highlighted the issue earlier with Meta as Micron passed it in market cap. The megacap names are the ones that are buying things from the smaller companies and if they decide to stop spending, then the massive jump in profits from the suppliers evaporate. At some point that's inevitable and it won't take all of the hyperscalers quitting at once to make it happen.

1) Someone drops out

The odds on favorite to pull back on spending is Meta but it is locked into some multi-year commitments so that could be promblematic. Microsoft's AI strategy is also looking like a mess right now and Google is hemorrhaging talent to Anthropic. If just one of the big spenders drops out, it can turn an undersupply of chips into an oversupply or something closer to a balanced market and you better believe that when the big names get a chance to reverse the pricing leverage, they will.

2) Stocks continue falling

If the market is no longer rewarding AI capex, it will kick and scream until someone listens. There isn't a great fundamental floor under any of the hyperscalers right now because all of their free cash flow is going to capex. Meta looks like it will spend $135-145 billion on capex this year from $39B in 2024 and the numbers look even worse when you break it down into discretionary capex (vs the usual server replacement cycle). If shares continue falling, then the pressure will build to pivot.

3) The money runs out

Perhaps the watershed moment was earlier this month when Google decided to raise cash for capex via equity. Previously, companies had tapped circular financing, vendor financing and debt to pay for all the spending. That might be running out and if so, they will struggle to keep the party going.

4) IPOs suck up the money

The other two big spenders in the AI capex race are OpenAI and Anthropic. Those two are also continuing to beat the hyperscalers' models and planning go public, likely late this year. The IPOs could raise some money but most of it is likely to be exit liquidity for employees and early investors. That's a problem because there is only a limited amount of money to go around and the AI capex story is proving that cash is harder to find than smaller investments at inflated valuations.

5) The tech doesn't deliver

This is the ultimate nightmare. AI is amazing but it might not deliver the ROI to justify the spending. It could become a commoditized product, open source Chinese models could win or it could simply fail to deliver in terms of valuable use cases. Spending $1 trillion in capex a year had better have an amazing return because if it doesn't, then it gets ugly fast.

In short, a lot can go wrong here and the market is pricing some of those risks.

What's also problematic is that it's not just the AI race. Apple is the big loser today and it's not developing a model. Still, it announced price hikes due to memory costs today and they're significant. That could dampen demand and it is assuredly hurting margins.