- Prior month composite 51.5

- S&P global composite PMI final 51.9 versus 52.2 preliminary

- S&P global services PMI 51.2 versus 51.3 preliminary and 50.7 last month.

S&P Global US Services PMI (June) – Key Takeaways

- Services activity improved modestly, with the Business Activity Index rising to 51.2 from 50.7 in May, marking a third consecutive month of expansion, though growth remained below post-pandemic norms.

- New business accelerated to its fastest pace since February, supported by new project wins, improving domestic demand, and a boost from FIFA World Cup-related activity.

- Export demand remained weak, falling for a seventh straight month, as businesses cited uncertainty surrounding government policy and tariffs.

- Employment declined for the third time in four months, as firms remained cautious about hiring and often chose not to replace departing workers.

- Backlogs of work increased for a sixteenth consecutive month, reflecting ongoing capacity constraints, supply chain disruptions, and longer project lead times.

- Input cost inflation remained elevated, driven by labor costs, tariffs, and higher fuel prices, although the pace of cost increases eased to its slowest since February.

- Selling prices continued to rise at a historically elevated pace, with little change from May as firms passed through higher costs.

- Business confidence improved to its highest level since February, supported by expectations for better economic conditions, easing price pressures, and new project launches.

Bottom line: The US services sector continued to expand in June, with stronger new orders and improving business confidence offset by weak export demand and ongoing job cuts. Inflation pressures remained elevated but eased somewhat, while firms stayed optimistic that activity will strengthen further over the coming year.

Details:

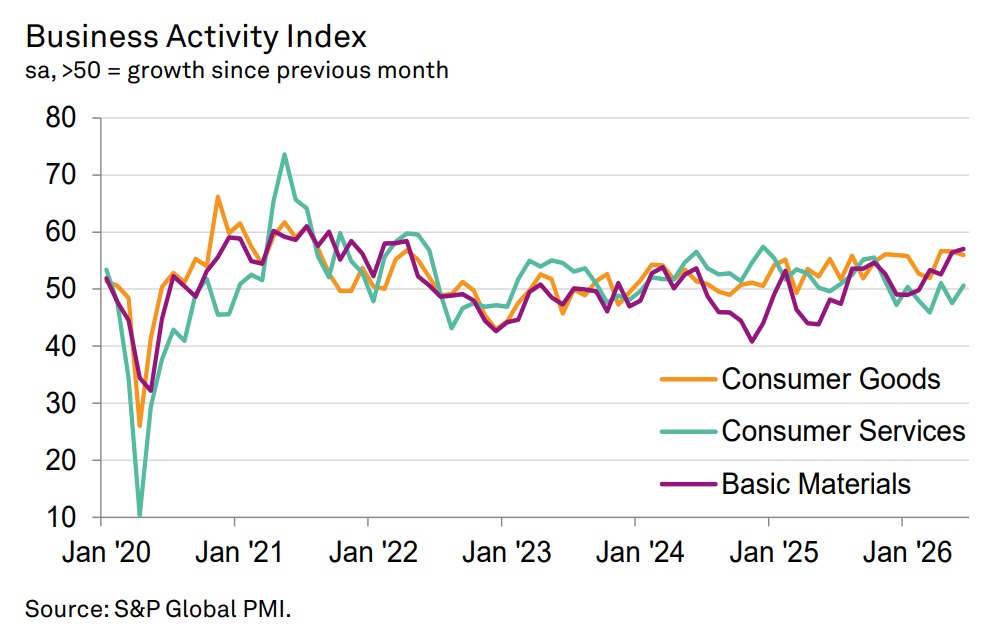

- All seven major US sectors expanded in June, up from only four sectors in May, marking the broadest growth since November 2025.

- Basic Materials led all sectors with the strongest output growth (57.0), posting its fastest expansion in more than four years.

- Consumer Goods remained a strong performer, recording the second-fastest pace of output growth.

- Healthcare continued to grow at a solid pace, although expansion eased from May's 4½-year high.

- Industrials also expanded but lost momentum, with growth slowing to its weakest pace since October 2025.

- Technology returned to growth for the first time since February, though the expansion remained modest and below the long-run average.

- Financials also returned to growth, but the pace was only modest.

- Consumer Services moved back into expansion (50.6), but growth was barely above breakeven and the weakest among all seven sectors.

Bottom line: June's report points to a broader improvement in US business activity, with every major sector expanding. Strength was concentrated in Basic Materials and Consumer Goods, while Technology, Financials, and Consumer Services returned to growth but remained relatively subdued. Healthcare and Industrials continued to expand, although both showed signs of slowing momentum.