- Prior month 54.5

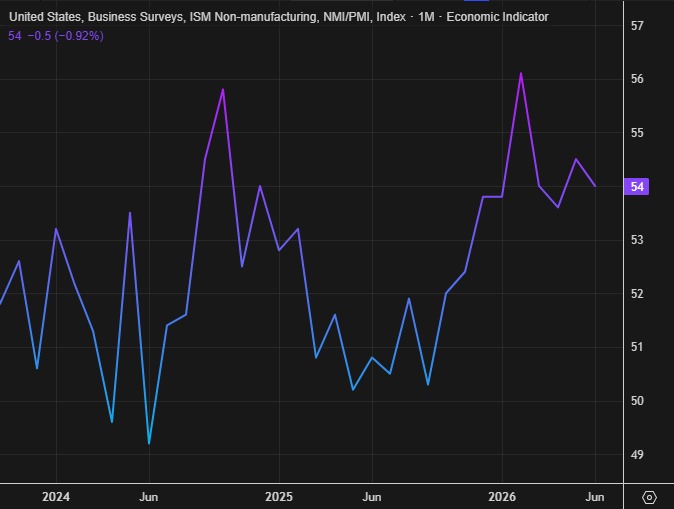

- ISM non-manufacturing PMI for June 54.0 vs 54.0 last estimate

- Business activity index 55.4 vs 57.7 last month

- Employment index 51.2 versus 47.9 last month

- New orders index 55.1 versus 57.3 last month.

- Prices paid index 67.7 versus 71.3 last month

- supplier deliveries 54.4 versus 55.2 last month.

- Inventories 51.2 versus 62.5 last month.

- Backlog of orders 54.9 versus 51.3 last month.

- New export waters 50.4 versus 50.0 last month.

- Imports 49.4 versus 51.1 last month.

- Inventory sentiment 52.6 versus 55.2 last month.

Detail sumary

Higher (3 of 9)

- Employment: 51.2 vs 47.9 (+3.3) ✅ Largest increase

- Backlog of Orders: 54.9 vs 51.3 (+3.6) ✅ Best-performing component

- New Export Orders: 50.4 vs 50.0 (+0.4)

Lower (6 of 9)

- New Orders: 55.1 vs 57.3 (-2.2)

- Prices Paid: 67.7 vs 71.3 (-3.6) (Largest decline; easing inflation pressures)

- Supplier Deliveries: 54.4 vs 55.2 (-0.8)

- Inventories: 51.2 vs 62.5 (-11.3) ❌ Worst-performing component

- Imports: 49.4 vs 51.1 (-1.7)

- Inventory Sentiment: 52.6 vs 55.2 (-2.6)

Biggest Movers

Strongest Improvement

- Backlog of Orders: +3.6 points (54.9 vs 51.3)

- Employment: +3.3 points (51.2 vs 47.9)

Largest Declines

- Inventories: -11.3 points (51.2 vs 62.5) — by far the biggest drop.

- Prices Paid: -3.6 points (67.7 vs 71.3), suggesting inflation pressures eased, though the index remains elevated.

- Inventory Sentiment: -2.6 points (52.6 vs 55.2).

Overall, the report was mixed. Employment and backlogs improved notably, pointing to firmer labor demand and work pipelines, while the sharp decline in inventories suggests businesses continued to work down stockpiles which could ultimately be a positive for the economy on a rebuild.

The drop in the Prices Paid index is a favorable sign on the inflation front, even though price pressures remain relatively high.

What are respondents saying:

WHAT RESPONDENTS ARE SAYING

“We continue to experience higher prices due to the Persian Gulf conflict through rising diesel fuel costs and increased input costs for resin-based packaging. The brunt of the impact will be experienced in the third quarter (Q3) of 2026, but we are feeling the impact now. Suppliers are aggressively attempting to pass through price increases.” [Accommodation & Food Services]

“Extreme drought in Virginia is creating financial problems for farmers and the agricultural industry. Dramatically reduced spring crops harvest has created significant cost increases in feed expense. The barley grain crop was nearly totally lost due to the early hot weather and spring freeze. High fertilizer cost increases due to the war in Iran and increased freight cost has driven cost for crops above breakeven levels on many farms. Many dairy farmers are struggling with crop shortages, high input cost and below milk price breakeven. The financial stress from higher cost due to the Iran war and drought-related forage losses has resulted in decreased spending in the agricultural sector.” [Agriculture, Forestry, Fishing & Hunting]

“In general, our company (commercial construction) is doing well. Pipeline is healthy for current and future work. Material pricing is higher and lead times on certain components in support of data center piping is elongating.” [Construction]

“In addition to the known semiconductor manufacturing issue, now there are concerns regarding memory availability that is materially impacting our OEM’s purchasing patterns, which is affecting availability and driving my company’s purchasing decisions, including how much longer we are sweating our assets, how frequently we refresh, and how we approach maintenance contracts.” [Finance & Insurance]

“Despite economic headwinds like persistent inflation, patient volumes and overall business activity remain strong reflected mainly by outstanding revenue performance. Supply chains remain resilient as well; back orders are at a historical low, and few if any critical products are experiencing difficulties. Labor is steady, as we continue to add full-time workers while the forecast remains positive. Given the continuation of the conflict in the Middle East, we are beginning to hear that cost of goods increases are on the horizon but have yet to materialize. Cost increases are in focus for the next quarter.” [Health Care & Social Assistance]

“From a strategic supply chain perspective, we are seeing increased complexity in managing total landed cost due to tariffs, import/export constraints and duty recovery mechanisms, requiring more proactive coordination across sourcing, logistics and compliance teams. Recent discussions internally also highlight the impact of tariff programs and duty drawback evaluations on purchasing strategies.” [Mining]

“Demand remains strong in infrastructure, environmental, and resilience projects, while procurement faces persistent labor inflation, supplier capacity constraints, and regulatory complexity—particularly in California and other high-cost markets. Labor-driven categories remain elevated despite easing goods inflation. The impact is higher rates, longer lead times, and increased importance of capacity assurance vs. lowest-cost sourcing.” [Professional, Scientific & Technical Services]

“Business has been very strong during what is usually a less active time of the year. Pricing is stable, and employment just where we want it to be. Supply chain strong with no challenges.” [Retail Trade]

“The utility industry continues to experience extended lead times, supply-chain constraints, material shortages, and pricing volatility. As a result, suppliers are often limiting quotation validity periods, with many RFQs carrying expiration dates as short as 24 hours. These conditions require timely evaluation and procurement decisions to mitigate the risk of price changes and availability issues.” [Utilities]

“We are experiencing continued sequential top-line growth driven mostly by increased prices.” [Wholesale Trade]