- Euro heavy across majors as Germany slashes growth outlook

- AUD: Australian pension funds rush to shield portfolios from Iran war currency shock

- Fed rate cuts pushed to late 2026 as Middle East war fuels inflation surge

- PBOC sets USD/ CNY reference rate for today at 6.8650 (vs. estimate at 6.8294)

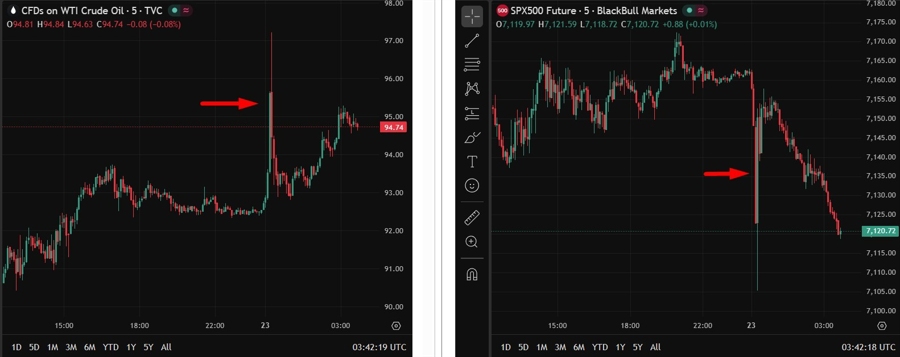

- Fake news (social media) on an attack on Tehran sent oil up, stocks down. Unwound now.

- Japan PMI shows manufacturing surge as services slowdown caps growth

- New Zealand Finance Minister on Iran war: Inflation could hit 7.4% (worst case scenario)

- Tesla to ramp capex to $25bn as AI push deepens despite strong Q1 cash flow

- South Korea Q1 growth surges past forecasts on semiconductor export boom

- Australian preliminary April PMIs jump back into expansion

- Gold steadies after drop as Iran tensions and dollar keep prices rangebound

- AI stocks near 45% of S&P 500 weight, Goldman flags rising concentration

- US crude stocks rise 1.9m vs draw expected as gasoline, distillates fall

- Commodity traders reap billions as Iran war drives oil market volatility (ps. its the job)

- investingLive Americas market news wrap: Stock markets rally even as oil prices climb

- More detail on the US seizing Iranian oil tankers all the way over in Asia

Summary

- Unverified social media rumours of a fresh Iran attack caused a brief spike in oil and dip in stocks, both of which quickly reversed when the reports were not confirmed

- USD edged higher with Middle East newsflow quiet

- Asia-Pacific equities finished mostly lower despite Wall Street having closed positively

- South Korea Q1 GDP came in well above forecasts, driven by a surge in semiconductor exports tied to AI demand

- Australian flash PMIs improved; Japan manufacturing picked up while services softened slightly

Markets across the Asia-Pacific region had a largely quiet session, though not without a moment of drama. Rumours circulating on social media suggested a fresh attack on Iran was underway, triggering a sharp but short-lived reaction, with energy prices jumping and equities pulling back before stabilising as the reports failed to gain any official confirmation. The episode was a reminder of how quickly unverified information can move markets in the current environment, where geopolitical nerves remain close to the surface.

Away from the noise, the US dollar found modest footing through the session. There was an absence of any new developments out of the Middle East.

Regional equity markets struggled to build on a constructive overnight lead from Wall Street, mostly in the red as caution prevailed. The positive handover from the United States was not enough to shift the mood.

On the data front, South Korea delivered the session's most notable result, with first quarter growth coming in comfortably ahead of expectations. Strong overseas demand for its technology exports, particularly semiconductors, was the key driver, reflecting the ongoing global appetite for AI-related hardware. The result did, however, point to a continuing dependence on external demand to power the economy.

Purchasing managers index readings (April, preliminary) from Australia came in better than the previous period. In Japan, factory activity improved while the services sector lost a little ground.