- Prior 50.2

- Manufacturing PMI 52.2 vs 50.9 expected

- Prior 51.6

- Composite PMI 48.6 vs 50.1 expected

- Prior 50.7

Similar to the French and German reports earlier, the industry sector shows a modest jump in activity but again it likely owes much to a frontloading in the order books. That as clients are choosing to secure shipments as quick as they can amid fears of widespread supply shortages and rising expenses.

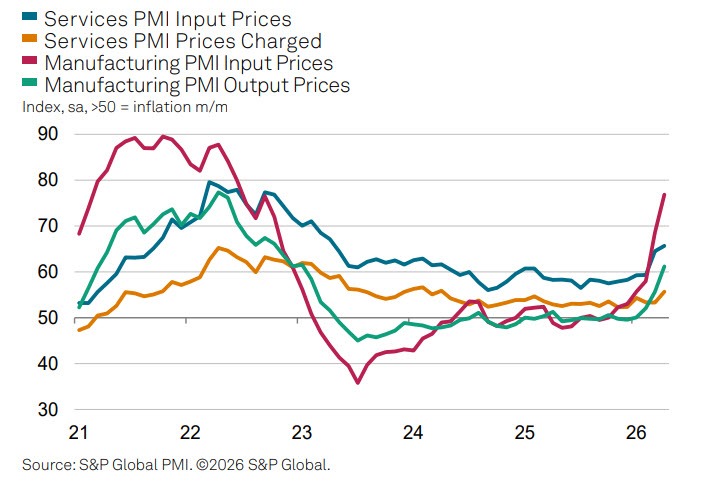

Meanwhile, surging input price inflation will be ultimate worry for businesses and also for the ECB. That will eventually have a much wider and bigger impact on the economy, as price pressures slowly trickle down to the consumer. For now, households have to deal with just higher fuel prices. But once businesses have to come to terms with rising operating costs, that will eventually be passed on to consumers and feed into core prices more prominently.

And amid the struggles, we're already seeing the services sector take a significant knock in April. So, that won't bode well for the economic outlook for the months heading into the summer.

HCOB notes that:

“The eurozone is facing deepening economic woes from the war in the Middle East, presenting a major headache for policymakers. The conflict has pushed the economy into decline in April, while driving inflation sharply higher. Increasingly widespread supply shortages meanwhile threaten to dampen growth further while adding more upward pressure to prices in the coming weeks.

“April’s flash PMI has moved into contraction territory for the first time since late 2024, signalling a 0.1% quarterly rate of GDP decline after a 0.2% gain had been signalled for the first quarter. The war is currently hitting the service sector hardest, where business activity is falling at a rate not seen since the pandemic lockdowns of early 2021. However, the sustained growth of manufacturing meanwhile seen in April comes with something of a sting in the tail, as demand for goods is being buoyed by stock building as companies scramble to secure purchases ahead of further price hikes or supply shortages. Manufacturers have increased their buying of inputs to a degree not witnessed since early 2022 as supply chain delays have also risen to the most widespread since the pandemic.

“Input costs and selling prices have already jumped higher not just in response to higher energy costs but in a reflection of a broader upturn in commodity prices and mis-match of demand against constrained supply. If the COVID-19 pandemic is excluded, this is the biggest surge in cost pressures that we have recorded since 2000.

“Not surprisingly, businesses are taking an increasingly gloomy view of the outlook, with sentiment now down to its lowest since late 2022.

“In this environment, the ECB once again has the unenviable task of deciding whether to raise interest rates in the face of the worrying inflation picture, or whether this price spike will prove temporary and its focus should instead be on the need to prevent the economy sliding into a deeper downturn. While postponing any decision could make either scenario worse, it would be understandable to see rate setters sit on their hands and await more clarity on the situation, both in terms of the conflict and the assessment of the eurozone’s economic health.”