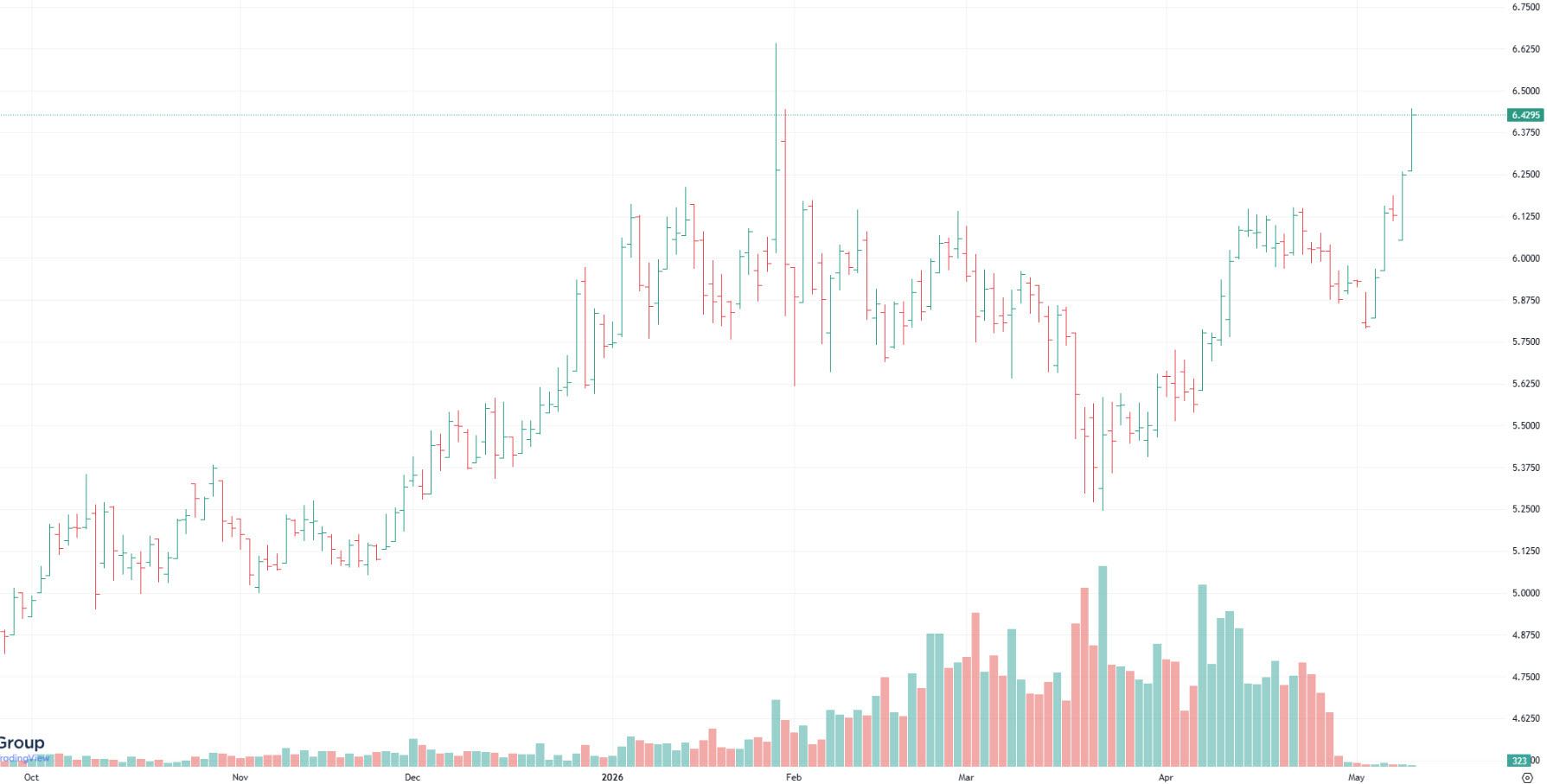

The remarkable thing about copper in 2026 isn’t where it’s trading—it’s where it isn’t. With the Strait of Hormuz still a battleground, oil dancing around levels that would normally crush industrial metals, and global growth forecasts being marked down by the week, copper is holding $6.45/lb on Comex and refusing to break. That’s a stone’s throw from the all-time highs set in late January, before the war even started. “Dr. Copper” is supposed to be the world’s most reliable economist. In this kind of macro environment—war in the Persian Gulf, blocked shipping lanes, energy shocks—the textbook says copper should be falling but it’s still threatening fresh highs.

The bear case wrote itself when the missiles started flying. Bloomberg Intelligence laid it out clearly: oil at $150-plus and curbed flows through Hormuz could drive copper below $10,000/t and tip the refined market into a 100,000–200,000 ton surplus. JPMorgan’s EMEA mining team noted that copper has historically troughed about 25% below peak during major macro shocks, with Dominic O’Kane flagging additional downside risk if global growth headwinds accelerate. The logic is straightforward—stagflationary energy shocks destroy demand. Copper, as a cyclical industrial metal, should follow. It hasn’t.

For context, $6.45/lb on Comex translates to roughly $14,200 per tonne—effectively aligning the US price with the upper end of recent LME trading ranges.

What’s emerged instead is a market that looks almost intellectually disorienting. Few spectacles in commodities are as puzzling as a metal trading near record prices while visible inventories build and macro conditions deteriorate. Yet that is precisely where copper sits today. On the LME, three-month copper recently pushed toward $14,000/t, brushing record territory even as the geopolitical backdrop deteriorates. Traders have effectively shrugged off the war, focusing instead on a more nuanced supply-demand balance that is tightening beneath the surface.

The explanation begins on the supply side—and ironically, the war itself is part of the bullish story. The Middle East conflict has disrupted shipments of sulphuric acid, a critical input in copper refining. Gulf countries account for roughly 45% of global sulfur supply, and the near-halt of tanker traffic through Hormuz has choked availability. In response, China has banned sulphuric acid exports from May through at least December, removing an estimated 3 million tonnes from the seaborne market. That hits major importers like Chile, Indonesia, and India directly.

This matters more than it initially appears. Roughly 15% of global copper production is directly reliant on sulphuric acid availability. Chile alone depends heavily on imported acid for leaching operations, and disruptions are already feeding through. Chilean production was down around 6% in Q1 2026 versus the same period in 2025, even before the acid shortage fully tightened the system. Costs are rising as well—Codelco estimated a roughly 5% increase in production costs tied to the war-related disruptions.

The second pillar holding copper up is demand—and specifically, the Chinese bid. Chinese buyers account for roughly 60% of global consumption, and they’ve been aggressively buying the dip. After being priced out during earlier rallies, they’ve used macro-driven weakness to rebuild inventories. O’Kane noted that copper held steady in mid-March at around $12,000/t despite severe macro tensions, largely explained by strong Chinese buying. That bid has acted as a floor under the market through the worst of the war headlines.

There’s also a structural demand component that is increasingly difficult to ignore. Citi points to three drivers: the energy transition, AI infrastructure buildout, and rising military demand. The last of these is underappreciated. Military-related copper consumption is estimated at roughly 2.5 million tons annually—about 9% of global demand—and modern warfare is becoming more metal-intensive. Drones, missiles, and electrified systems all increase copper intensity, and defense budgets are still expanding. Historical data from the Russia-Ukraine war suggests copper demand can grow faster than military spending itself.

On top of that, strategic stockpiling is emerging as a new layer of demand. The U.S. “Project Vault,” a $12 billion initiative aimed at building strategic reserves of critical minerals, adds another incremental buyer to the system.

The mine side completes the picture. Production has been constrained by a series of disruptions across key regions. Operational setbacks in Chile, Africa, and Indonesia throughout 2025 have already pushed the market toward its first annual contraction in output since the pandemic. Events like the Kakula earthquake and Grasberg mudslide are still working through supply chains and the full resumption of Grasberg was recently pushed further back. UBS has responded by raising its 2026 deficit forecast to around 520,000 tons, reflecting a widening gap between supply and demand.

The longer-term setup I've been writing about for years hasn’t changed—and if anything, it has tightened. The International Copper Study Group sees a 178,000-ton surplus in 2025 flipping to a 150,000-ton deficit in 2026. Morgan Stanley is more aggressive, forecasting the most severe copper deficit in more than 20 years, with demand exceeding supply by roughly 600,000 tons next year. Citi goes further still, suggesting that once the Strait of Hormuz reopens and sentiment improves, prices could push toward $15,000/t by year-end.

Not everyone is convinced. StoneX has warned that speculative positioning looks overdone, calling current price levels “unsustainable.” Goldman Sachs expects copper to trade in a $10,000–$11,000/t range next year, arguing that near-term fundamentals don’t fully justify the rally. There is also the issue of inventory—global visible stocks have climbed to around 1.5 million tons, though much of that build is geographically concentrated in the U.S. ahead of tariff risks, while other regions tighten.

Still, the key point is that copper has erased the losses sustained during more than six weeks of war—and then some. The market is no longer trading purely on macro fear. Instead, it’s pricing a structurally tight system where supply constraints, policy-driven demand, and opportunistic Chinese buying are offsetting what would normally be a deeply bearish environment.

That’s the paradox of copper in 2026. The macro says it should be breaking but it isn't and that might be a tell, particularly if this war ever ends.