Rate spread dynamics are reasserting themselves as the dominant EUR/USD driver now that Middle East risk premium has largely unwound from oil prices. A narrowing gap between US and European yield expectations, as Fed hike pricing fades faster than ECB pricing, points to scope for the pair to grind higher through 2026 and into 2027. The bund curve has flattened alongside the drop in crude, with the 10-year yield already easing to reflect reduced inflation risk. Positioning around a potential final ECB insurance hike will be a key swing factor for European rates markets into year end.

---

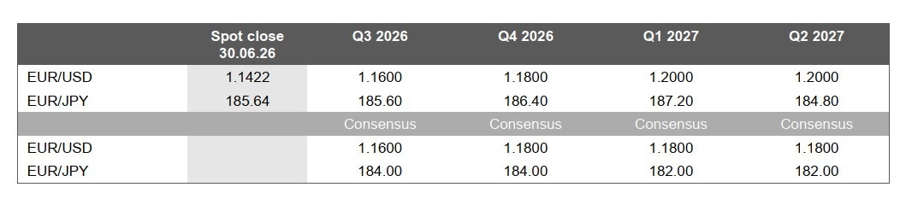

MUFG forecasts EUR/USD recovering to 1.20 by Q1 2027, above consensus, as fading Fed hike bets and one final ECB insurance hike reshape the rate spread outlook.

Summary:

- EUR/USD weakened from 1.1683 to 1.1422 in June, its longest stretch below 1.15 since June last year

- The ECB raised its deposit rate 25bp to 2.25% in June, its first hike since September 2023

- OIS pricing has fallen from close to three ECB hikes priced before June to roughly one now

- ECB Chief Economist Philip Lane said the top of the neutral policy range had likely drifted to 2.50%

- The 10-year German bund yield fell 8bps in June to 2.86% as crude oil declines eased inflation risk

- EUR/USD is forecast to recover to 1.1600 by Q3 2026, 1.1800 by Q4 2026 and 1.2000 by Q1 2027, above consensus

The euro is set to claw back recent losses against the US dollar and climb to 1.20 by early 2027, according to MUFG, as fading expectations for further Federal Reserve tightening outpace the diminishing but still live prospect of one more European Central Bank rate hike. The euro weakened from 1.1683 to 1.1422 against the dollar in June, its longest run below the 1.15 level in over a year, after the ECB raised its deposit rate 25 basis points to 2.25%, its first increase since September 2023.

The rate move followed a rapid unwind of the geopolitical risk premium built into oil prices earlier this year. Brent crude has largely reversed its US-Iran conflict driven surge, easing energy pass through pressure on inflation faster than had been anticipated. Options market pricing has adjusted accordingly, with OIS markets shifting from pricing close to three ECB hikes before the June meeting to roughly one now.

Even so, a further insurance hike remains plausible. ECB Chief Economist Philip Lane has said the top of the neutral policy range likely drifted higher to 2.50%, suggesting a relatively low hurdle to one more move, while flagging that energy related inflation pass through risks could persist for some time. ECB President Christine Lagarde has separately argued the euro area economy has grown more resilient to external shocks, implying it could absorb a further hike if required.

With crude oil stabilising near current levels, MUFG expects rate spreads to reassert themselves as the dominant driver of EUR/USD, arguing that pricing for a Fed hike now looks less realistic than pricing for a final ECB move. That dynamic underpins the bank's above consensus forecast profile, with EUR/USD seen rising to 1.1600 in the third quarter, 1.1800 by year end, and 1.2000 by the first quarter of 2027, a level it expects to hold into the following quarter. The 10-year German bund yield, which fell 8 basis points in June to 2.86%, is expected to ease further over the same period as inflation risks continue to recede.