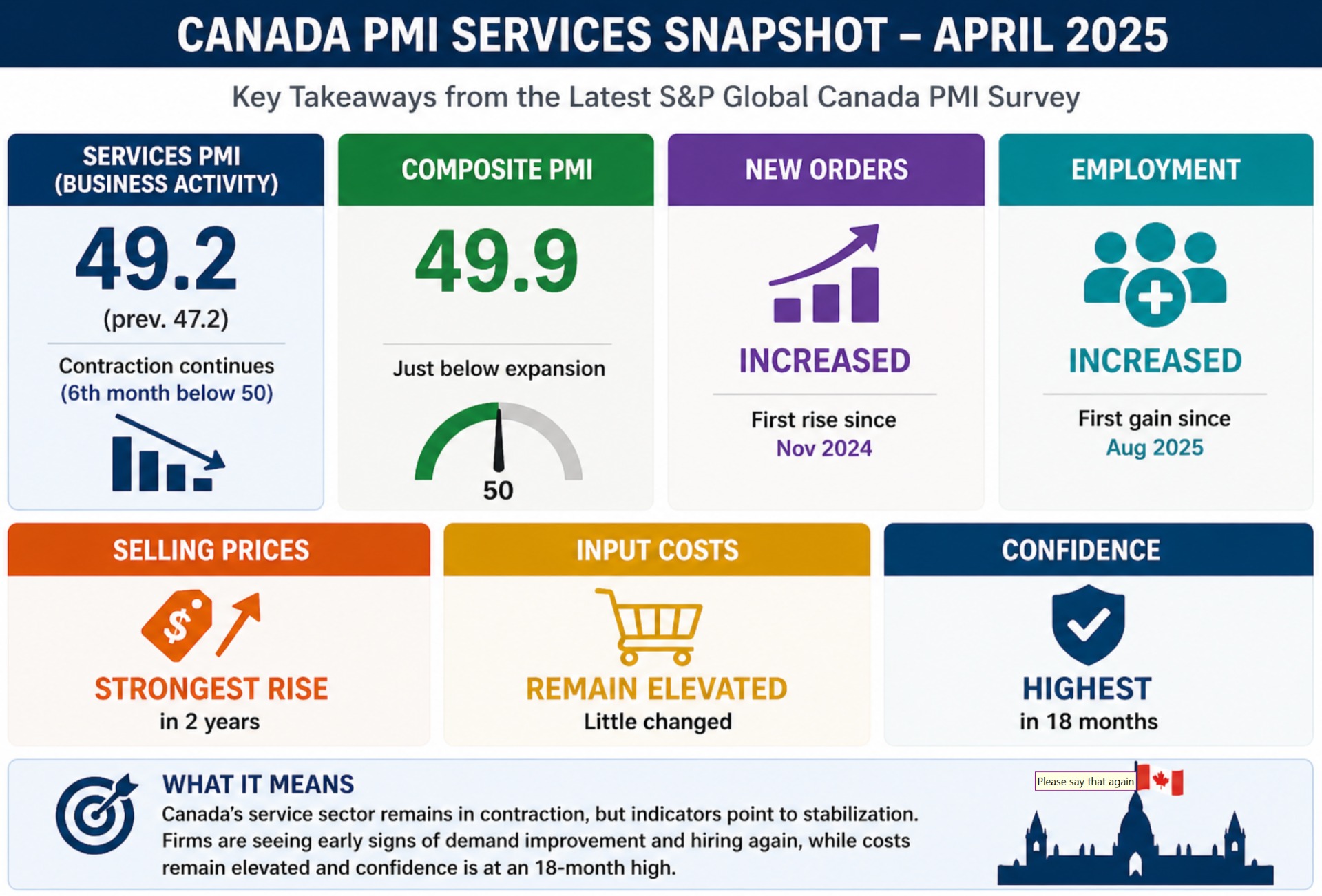

- Prior month 47.2

- Services PMI (Business Activity): 49.2 (prev. 47.2) → 6th month below 50 (contraction)

- Composite PMI: 49.9 → just below expansion threshold

- New Orders: Increased (first rise since Nov 2024)

- Employment: Increased (first gain since Aug 2025)

- Selling Prices: Highest increase in 2 years

- Input Costs: Remain elevated (unchanged vs prior month)

- Confidence: Highest in 18 months

Summary of the data

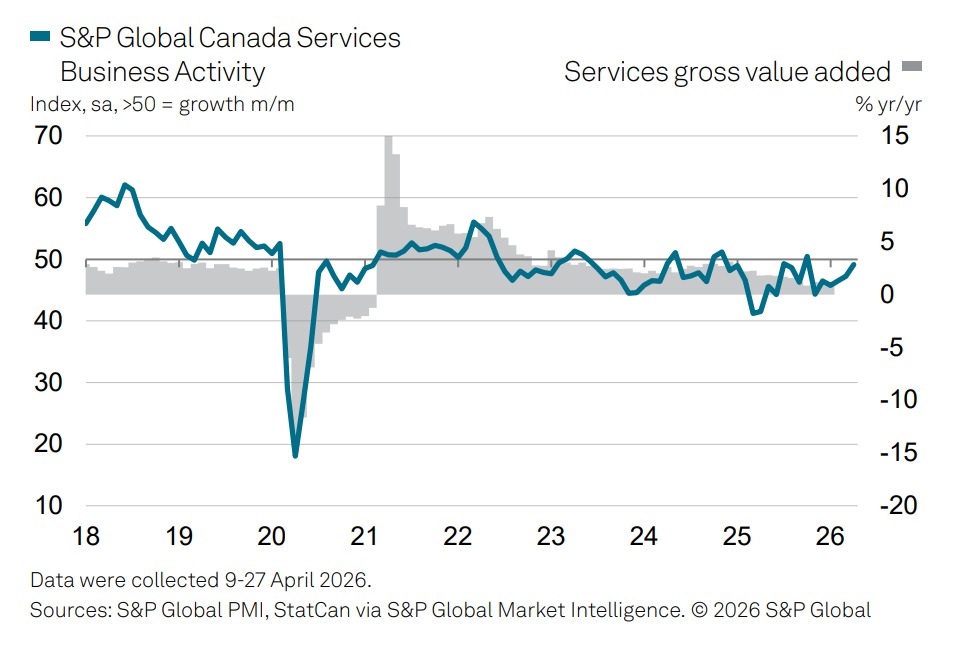

Activity & Growth

- Service sector still contracting, but decline is the slowest in 6 months

- Composite near stabilization as manufacturing strength offsets services weakness

Demand & Orders

- New business edged higher, signaling early stabilization

- International sales still falling sharply

- Weak activity tied to soft underlying demand and uncertainty

Employment

- Hiring increased modestly for the first time in ~8 months

- Additional staff helped reduce backlogs

Inflation & Costs

- Input costs remain elevated, driven by tariffs, energy, and wages

- Firms passed through higher costs, lifting selling prices sharply

Risks & Drivers

- Tariffs and Middle East conflict continue to raise costs and weigh on demand

Outlook

- Confidence improved to an 18-month high

- Firms expect gradual recovery in activity and demand

- Outlook remains uncertain due to geopolitical and trade risks

Bottom line

- Services sector still contracting but stabilizing, with early signs of improving demand and hiring, while inflation pressures remain elevated

Paul Smith, Economics Director at S&P Global Market Intelligence:

“Whilst Canada’s service sector continued to contract, it did so only marginally in April. Moreover, against the backdrop of tariffs and the war in the Middle East, overall performance wasn’t too bad when viewed in this context. Positively, new business volumes were up marginally, the first growth seen since November 2024 whilst there was also a small rise in employment. Confidence in the outlook also improved to an 18-month high with firms pointing to government initiatives as supporting wider economic growth in the year ahead.

“That being said, the sector continues to face noticeable headwinds, especially in relation to US tariffs and the war in the Middle East. Both continue to have inflationary implications, with firms signalling that operating expenses are rising sharply and at a rate just below March’s nine-month peak. The degree of pass through to clients also suggests that firms are keen to protect margins wherever possible, with selling price inflation picking up to its highest level in two years and raising some alarm bells for policymakers as they scour the economic news flow for signs of elevated inflationary pressures.”