- Prior 48.8

- Manufacturing PMI 52.8 vs 49.5 expected

- Prior 50.0

- Composite PMI 47.6 vs 48.6 expected

- Prior 48.8

French economic activity is seen contracting at its quickest pace in 14 months as the fallout from the Middle East conflict continues to bite at Europe's second largest economy. That comes despite some positive news from the industrial side of things, with stronger factory output growth recorded for the month.

That being said, the jump in factory order books owes much to some frontloading activity. It is the first time in nearly four years that the order book expanded but it is mostly due to clients bringing forward purchases ahead of expected shortages and price increases as supply issues arise from the Strait of Hormuz closure.

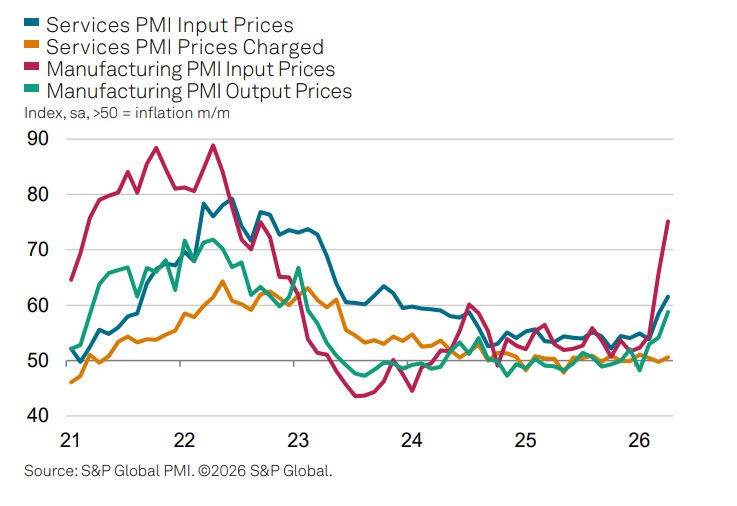

To nobody's surprise, input price inflation continued to surge higher in April - rising to a three-year high. A mix of higher costs for energy, fuel, transportation, chemicals and metals were commonly mentioned by panellists. So, just be mindful of that as it will eventually reverberate to all other aspects of the economy in due time.

HCOB notes that:

"There is a lot to unpack in the latest 'flash' PMI data for France. The service economy has deteriorated due to a diminishing willingness to spend – a typical consequence of uncertainty – pulling overall business activity levels lower. Preventing the headline 'flash' index from falling even further below 50.0 was the manufacturing sector, which saw a production rebound in April. However, this does not look like a turning point and will likely be temporary, as our survey respondents reported advance purchasing from customers in anticipation of price increases, shortages and logistics issues.

"Unsurprisingly, manufacturing inflation moved even higher in April as a range of raw material costs rose, transportation became more expensive and supply bottlenecks pushed up prices. Services companies are also feeling the pressure from higher transportation costs. What's most notable is that the passthrough to prices charged for goods and services remains contained. Services charges have barely moved since the outbreak of the war, which will be a welcome sight for policymakers in the European Central Bank. How long this continues remains to be seen, however, given the strain that corporate margins will be feeling."