NZ CPI held at 3.1% y/y in Q1, above target, with electricity and petrol driving gains. Quarterly inflation rose 0.9%, underscoring persistent price pressures and supporting expectations for a cautious RBNZ policy stance.

This is January - March data, ahead of the fuel shock. Bear that in mind...

Summary:

- Annual CPI holds at 3.1%, above RBNZ target band

- Electricity prices key driver, up 12.5%

- Quarterly inflation at 0.9%, led by petrol

- Underlying inflation remains firm even excluding fuel

- Rent growth slows to weakest pace in 16 years

- Data reinforces cautious RBNZ policy outlook

New Zealand inflation held above the central bank’s target band in the March quarter, with the latest New Zealand Consumer Price Index data from Stats NZ highlighting persistent cost pressures despite some pockets of easing.

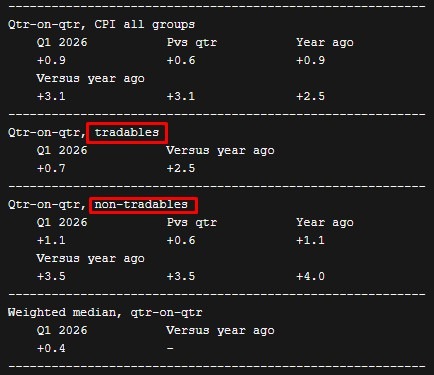

Annual CPI rose 3.1% in the year to Q1 2026, unchanged from the previous quarter and sitting just above the Reserve Bank of New Zealand’s 1–3% target range. The result underscores the stickiness of inflation, particularly in household essentials and administered prices.

Electricity costs were the dominant driver, rising 12.5% over the year and accounting for more than a tenth of the annual increase. This marks the third consecutive quarter in which electricity has been the largest contributor, pointing to ongoing pressure from energy-related costs.

Other key contributors included local authority rates, up 8.8%, alongside strong increases in food categories such as meat and poultry. Rent also continued to rise, although at a notably slower pace, with the 1.2% annual increase marking the weakest gain in 16 years, a sign that some domestic inflation components may be easing at the margin.

On a quarterly basis, inflation came in at 0.9%, with petrol prices the primary driver. Fuel costs rose 3.5% in the quarter, reversing earlier declines and reflecting renewed volatility in energy markets. Petrol alone, alongside a sharp rise in pharmaceutical costs linked to policy resets in prescription charges, accounted for more than a quarter of the quarterly increase.

Excluding petrol, CPI still rose 0.8% in the quarter, indicating that underlying inflation pressures remain firm. Additional upward pressure came from food and electricity, while declines in international airfares provided some offset.

Overall, the data suggest that while certain inflation components are moderating, core pressures remain resilient. The composition of the report, particularly the dominance of energy and administered price increases, is likely to keep policymakers cautious as they assess the timing and pace of further policy tightening.

---

This summarion via Reuters:

In CPI terms, tradables are goods and services whose prices are largely determined by global markets and can be imported or exported. This includes items like petrol, electronics, vehicles, clothing, and some food products. Because they are exposed to international competition and exchange rate movements, tradables inflation is heavily influenced by factors such as global commodity prices, shipping costs, and the strength of the New Zealand dollar. For example, a weaker NZD or higher oil prices typically push tradables inflation higher.

By contrast, non-tradables refer to goods and services that are primarily produced and consumed domestically, with prices driven by local economic conditions rather than global markets. This category includes housing-related costs (like rent and construction), local government rates, electricity, and many services such as healthcare and education. Non-tradables inflation tends to reflect domestic demand, wage growth, and capacity constraints in the economy. Central banks, including the Reserve Bank of New Zealand, often focus more closely on non-tradables as a gauge of underlying inflation pressure because it is less volatile and more tied to the domestic policy setting.

--

The report is modestly hawkish for RBNZ expectations. Inflation holding above target, combined with firm underlying measures, supports the case for continued policy tightening or at least a delayed easing cycle. Energy-driven components add volatility, but persistence in core pressures is likely to keep front-end rates supported and limit downside in NZD.