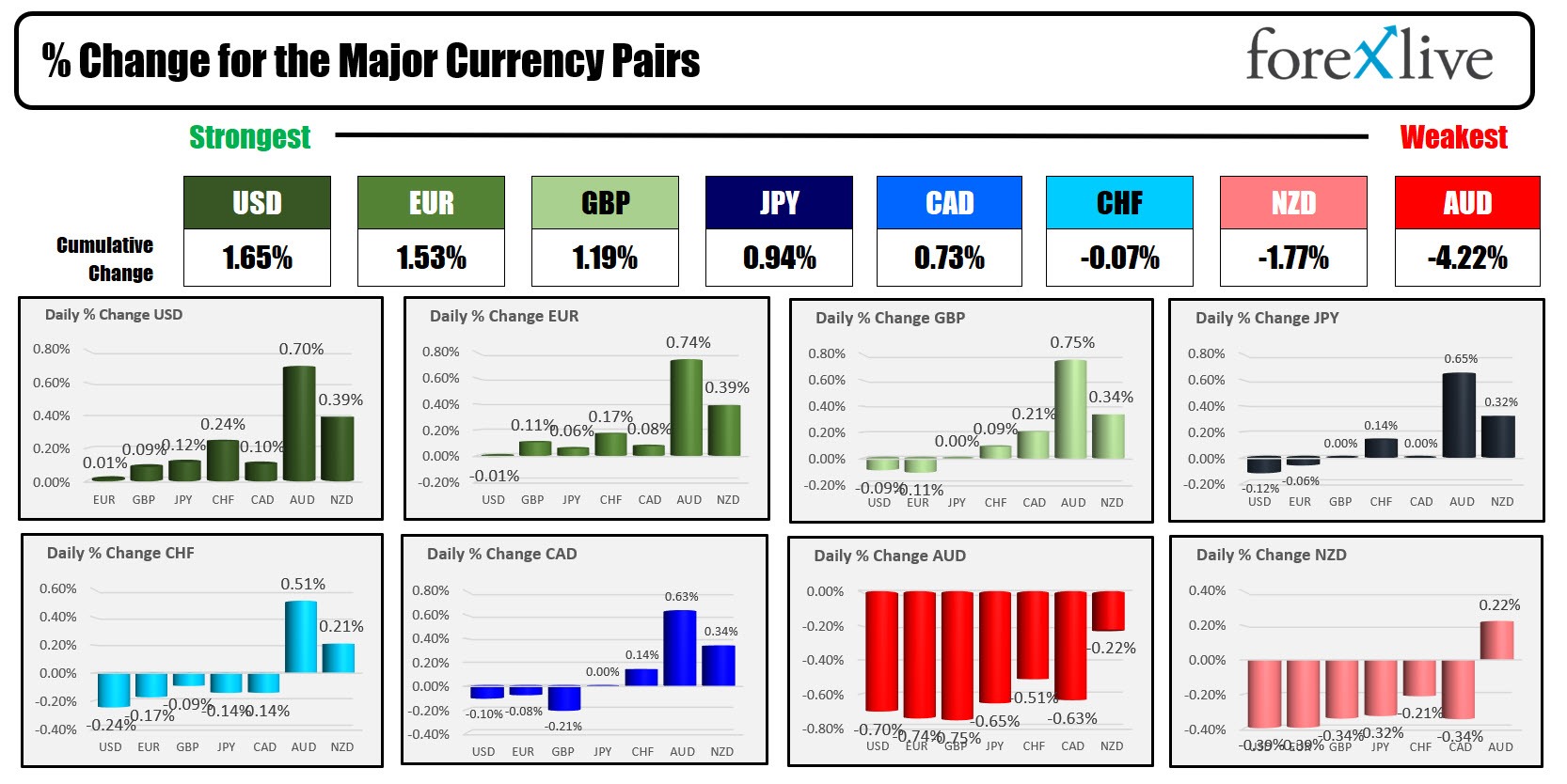

The USD is the strongest and the AUD is the weakest as the NA session begins.

Yesterday, the FOMC kept rates unchanged with Fed chair Powell saying that the base case is for no change in policy in March. That comment sent stocks lower into the close with the S&P index down the most since September 2023, and the Nasdaq down the most since October 2023. The USD traded higher on the comment. The estimate for the first cut is now shifting to May/June (Barclays moved from March to May as did Goldman. BofA moved to June from March.

The focus in the US will now shift to the jobs report which will be released tomorrow at 8:30 AM ET. The expectations are for a rise of 187K and a tick up in the input rate to 3.8% from 3.7%. Having said that there are a number of releases today including initial jobless claims (212K est), Q4 productivity (+2.5% vs 4.7%), Construction spending (est 0.5% est vs 0.4% last month), and ISM manufacturing PMI (47.0 vs 47.4 last month). Also after the close will be a number of earnings reported with Apple, Amazon and Meta the top 3 scheduled. Earlier today, the Challenger job cuts came in at 82.307K. That is the largest announced cuts since March 2023.

Today, the BOE kept rates unchanged today with the vote showing 2 dissenters to the upside, 1 dissenter to the downside and 6 for unchanged policy. Mann and Haskins called for the rate hikes, and Dinghra called for a cut. Bailey is saying that things are moving in the right direction. However, the BOE is not ready to start lowering rates.

In his press conference, BOE Governor Bailey emphasized the need for concrete evidence of easing services inflation, highlighting it as one of the most persistent elements of inflation. He stressed the importance of looking beyond short-term trends in policy-setting, cautioning that services inflation could remain sticky in the upcoming months. Bailey expressed hope that lower inflation would start to shape expectations within the real economy, though he noted the necessity for more evidence to support this shift. He firmly stated that an inflation rate reverting to around 2.7% would not be satisfactory and emphasized the goal of returning inflation to the 2% target as paramount for benefiting households. Bailey assured that the current policy stance would not be sustained longer than necessary, but he warned that following the market rate conditioning path could result in inflation staying above target for a significant portion of the next three years. He did say the MPC does not need to see the inflation rate at 2% to cut rates, but it just needs to show it is on that path.

In Europe today, the PMI data was released with mixed results vs the estimates. All the numbers, however, remain below the 50 level indicating a contracting manufacturing base:

Spanish Manufacturing PMI

- Actual: 49.2

- Estimate: 47.9

- Prior: 46.2

- STRONGER than the estimate

Swiss Manufacturing PMI

- Actual: 43.1

- Estimate: 44.5

- Prior: 43.0

- WEAKER than the estimate

Italian Manufacturing PMI

- Actual: 48.5

- Estimate: 47.0

- Prior: 45.3

- STRONGER than the estimate

French Final Manufacturing PMI

- Actual: 43.1

- Estimate: 43.2

- Prior: 43.2

- WEAKER than the estimate

German Final Manufacturing PMI

- Actual: 45.5

- Estimate: 45.4

- Prior: 45.4

- STRONGER than the estimate

Eurozone Final Manufacturing PMI

- Actual: 46.6

- Estimate: 46.6

- Prior: 46.6

- EQUAL to the estimate

UK Final Manufacturing PMI

- Actual: 47.0

- Estimate: 47.3

- Prior: 47.3

- WEAKER than the estimate

A snapshot of the markets as the North American session begins currently shows:

- Crude oil is trading up $0.24 at $76.11. At this time yesterday, the price was trading at $77.01 OPEC+ is to review extending 2.2M BPD voluntary cuts (due to expire at the end od Q1).

- Gold is trading down down $5.27 or -0.26% at $2033.71. At this time yesterday, the price was trading at $2038.60

- Silver is trading down -$0.30 or -1.32% at $22.62. At this time yesterday, the price was trading at $23.11

- Bitcoin traded at $42,059 At this time yesterday, the price was trading at $42,596.

In the premarket for US stocks, the broader S&P and NASDAQ indices are lower after mixed results yesterday

- Dow Industrial Average futures are implying a gain of 64.7 points. Yesterday the index fell -317.01 points or -0.82%

- S&P futures are implying a gain of 22.35 points. Yesterday the index fell -79.3 points or -1.61%

- Nasdaq futures are implying a gain of 108 points. Yesterday the index fell -345.89 points or -2.23%

In the European equity markets, the major indices are trading mixed with the UK,Spain and Italy indices higher:

- German DAX, -0.05%

- France CAC -0.63%

- UK FTSE 100, +0.23%

- Spain's Ibex, as 0.46%

- Italy's FTSE MIB, +0.20% (delayed by 10 minutes).

Shares in the Asian Pacific markets were mixed. The

- Japan's Nikkei 225, -0.76%

- China's Shanghai composite index , -0.64%

- Hong Kong's Hang Seng index, +0.52%

- Australia S&P/ASX, -1.20%

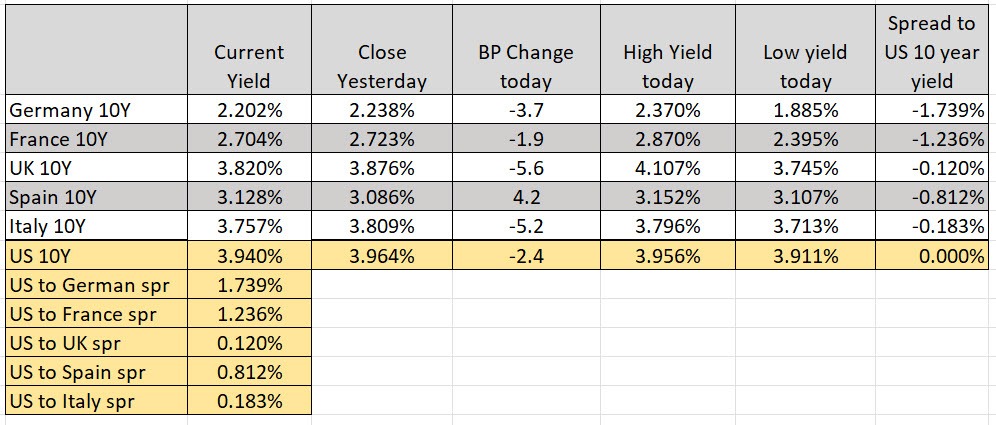

Looking at the US debt market, yields are trading lower to start the trading day.

- 2-year yield 4.243% +1.5 basis points. At this time yesterday, the yield was at 4.315%

- 5-year yield 3.868% -1.2 basis points. At this time yesterday, the yield was at 3.953%

- 10-year yield 3.940% -2.4 basis points. At this time yesterday, the yield was at 4.026%

- 30-year yield 4.183% -3.2 basis points. At this time yesterday, the yield was at 4.256%

- The 2-10 year spread is at -30.1 basis points. At this time yesterday, the spread was at -28.8 basis points

- The 2-30 year spread is at -0.6 basis points. At this time yesterday, the spread was at -0.6 basis points.

In the European debt market, the benchmark 10-year yields are mixed: