The USD is mixed with the EUR (+0.09%) and the GBP (-0.09%) little changed vs the greenback and the USD higher vs the JPY by 0.27% despite expectations leaning toward a BOJ hike again as a result of the weak JPY. In the video above, I take a look at each of those currency pairs - the EURUSD, USDJPY and GBPUSD - from a technical perspective.

In an unexpected early release “due to a technical issue,” the UK OBR published its full fiscal outlook ahead of the Budget, showing the government on track to run a £21.7 billion surplus by 2029–30, more than double the £9.9 billion headroom projected in March. The outlook details a major tax-heavy Budget, including a three-year extension of frozen personal tax thresholds (raising £8 billion), higher dividend/property/savings tax rates (£2.1 billion), NICs on salary-sacrifice pensions (£4.7 billion), and a total £14.9 billion rise in personal-tax receipts. Additional measures include a new property tax on homes above £2 million, taxes on electric and plug-in hybrid vehicles from April 2028 (£1.4 billion), and gambling-tax reforms (£1.1 billion). Despite these increases, spending rises in every year, reaching £11 billion more by 2029–30, with the package amounting to the third-largest medium-term tax increase since 2010. The OBR now sees a 59% chance of meeting fiscal targets (up from 54%), upgrades 2025 GDP growth to 1.5% but trims 2026 to 1.4%, expects inflation at 3.5% next year and back to 2% by 2027, and projects debt stabilizing near 95–96% of GDP.

The GBPUSD initially moved higher but reversed sharply lower. The premature release sent markets into disorder: GBPUSD briefly jumped above 1.3200 before sliding to 1.3136, while UK 10-year yields rebounded from 4.43% to 4.53%. The episode has created political embarrassment, and markets appear to be signaling that this may be the last budget Reeves delivers.

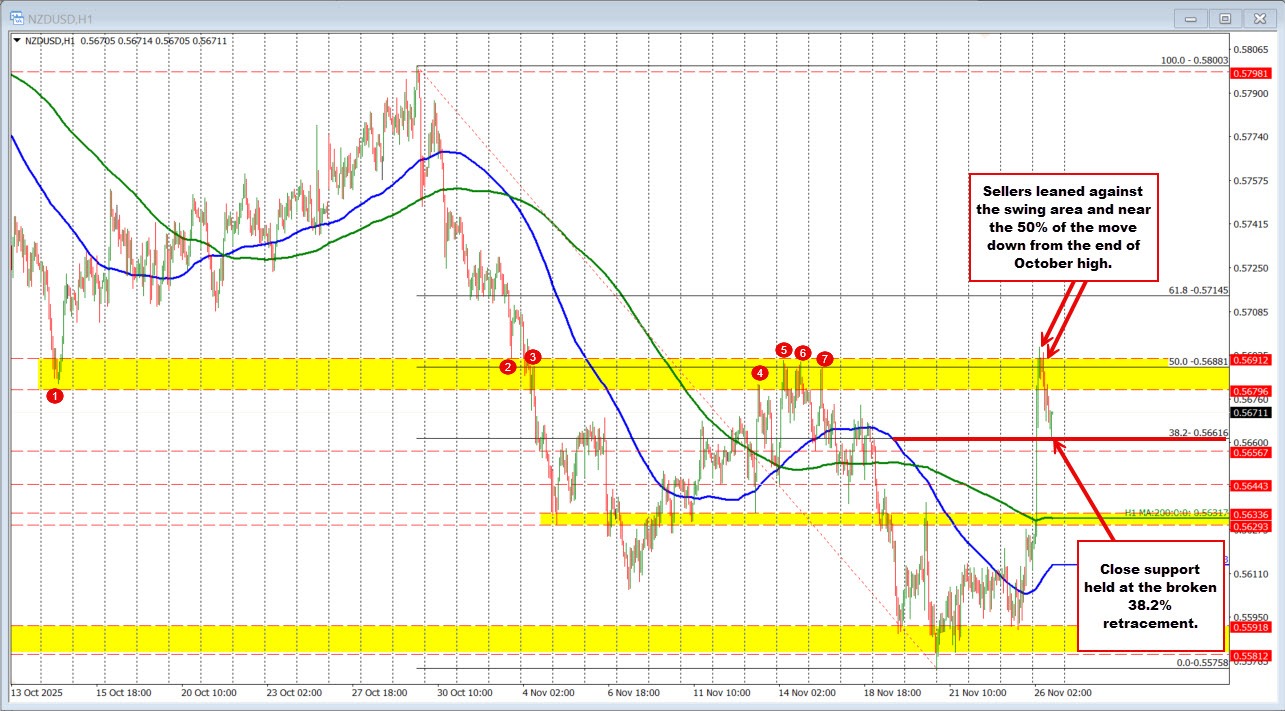

The RBNZ cut the Official Cash Rate by 25 bps to 2.25%, with the decision supported by a 5–1 committee vote. Policymakers noted that while annual consumer inflation increased to 3% in the September quarter, significant spare capacity in the economy should help bring inflation back toward 2% by mid-2026. Economic activity, which was weak in mid-2025, is beginning to recover, aided by lower interest rates that are supporting household spending and a stabilizing labor market. The Bank emphasized that future OCR moves will depend on how medium-term inflation and economic conditions evolve, with further reductions seen as helping to underpin confidence and offset the risk of a slower-than-desired recovery. The committee weighed holding the OCR at 2.50% versus cutting but ultimately opted for the reduction given the extent of excess capacity. The updated projections show the OCR at 2.25% in March 2026 (previously 2.55%) and 2.28% in December 2026 (previously 2.62%), highlighting the move lower today. Despite the cut, the prospect of the last rate cut has sent the NZDUSD higher. It is currently the biggest mover with a gain of 0.87% vs the USD. However, the pair did find willing sellers near the 50% of the move down from the end of October high, and swing area between 0.56796 and 0.56912 (high reached 0.5696).

In a Reuters article overnight, the Bank of Japan was reported to be preparing markets for a possible rate hike as early as December, shifting back to a more hawkish tone as the weak yen re-emerges as a key inflation risk. The article said BOJ officials have deliberately toughened their messaging in recent days to remind markets that a December move is still on the table, especially after a meeting between Prime Minister Sanae Takaichi and Governor Kazuo Ueda appeared to remove political resistance to further tightening. A growing number of board members now see conditions supportive of a hike, and even Ueda acknowledged the BOJ will discuss the “feasibility and timing” of raising rates at coming meetings. While the decision between December and January remains close and could hinge on the Fed meeting a week earlier, the BOJ increasingly views the yen’s decline as persistent and inflationary, giving it fewer reasons to delay normalization.

Australia’s October CPI came in hotter than expected, signaling renewed inflation pressure and effectively shutting the door on near-term RBA rate cuts. Headline inflation printed at 0.0% m/m (vs. -0.2% expected) and 3.8% y/y (vs. 3.6% expected), pushing further above the RBA’s 2–3% target band. Core measures were even more troubling: the trimmed mean rose to 3.3% y/y (2.9% expected, +0.3% m/m) while the weighted median hit 3.4% y/y (2.95% expected). With both headline and underlying inflation running too hot, the data strongly reinforces the RBA’s higher-for-longer stance. October’s release also marks the transition to the Monthly CPI as Australia’s primary inflation gauge, offering faster detection of inflation trends and more detailed breakdowns for policymakers. The AUDUSD is higher by about 0.42% to kickstart the US session.

The US stock indices are trading higher to start the day with the NASDAQ index leading the charge. The futures are currently employing

- Dow industrial average up 30 points

- S&P index of 14.37 points

- NASDAQ index up 96 points

Looking at the US debt market, yields are modestly higher:

- 2-year yield 3.471%, +1.2 basis points

- 5 year yield 3.572%, +0.7 basis points

- 10 year yield 4.007%, +0.6 basis points

- 30 year yield 4.659%, +0.2 basis points

Looking at other markets:

- Crude oil is down $0.13 and $57.80

- Gold is up $32 at $4163

- Silver is up $0.94 $52.39

- Bitcoin is down $719 and $86,612