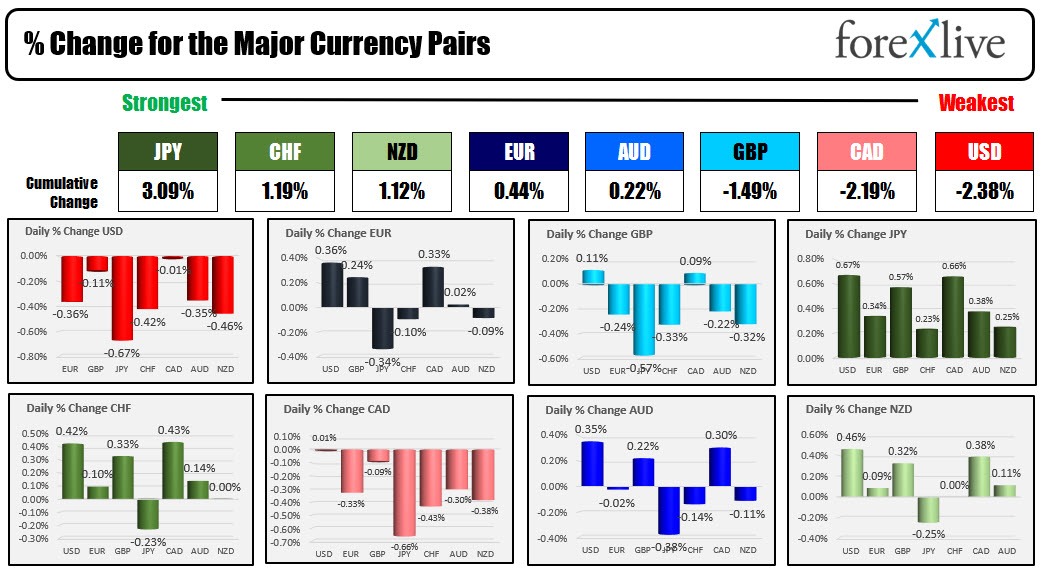

The JPY is the strongest of the major currencies after tumbling yesterday. The USD is inching out the CAD as the weakest of the major currencies. The GBP is also lower after weaker jobs and wage data.

This week the Big 3 (Fed, ECB and Bank of England) will announce rate decisions. Eamonn reported earlier, that Goldman Sachs analysts have revised their six-month forecast for the GBPUSD exchange rate, predicting an increase to 1.3000, contrasting with their earlier prediction of a decline to 1.2000 (the current rate is 1.2564). This adjustment is based on the expectation that the Bank of England (BoE) will be slower in reducing interest rates compared to its counterparts, the Federal Reserve in the U.S. and the European Central Bank (ECB). The analysts anticipate that the Fed and ECB will commence rate cuts in the first half of the year. They suggest that this earlier move to reduce rates by these central banks will position the BoE less as a "dovish outlier," which they believe will be significantly supportive of the British Pound. Current market pricing indicates expectations of approximately 115 basis points of easing by the Fed, 135 basis points by the ECB, and around 85 basis points by the BoE.

A CNBC released survey on Fed policy ahead of the rate decision tomorrow sees inflation coming down to 2.7% at the end of 2024. Participants see a 53% chance for a cut in June and a 69% chance in July. Finally, they see an end of year 2024 target at 4.53% and 3.73% for 2025. The current rate is targeting 5.25% to 5.50%

Today, US CPI data will be released at 8:30 AM ET and is the last look at inflation as the Fed starts its 2-day meeting. The expectations are showing:

Core CPI (Consumer Price Index) Month-to-Month (MM), Seasonally Adjusted (SA) for November

- Expected: 0.3%

- Previous: 0.2%

Core CPI Year-to-Year (YY), Not Seasonally Adjusted (NSA) for November

- Expected: 4.0%

- Previous: 4.0%

CPI Month-to-Month (MM), Seasonally Adjusted (SA) for November

- Expected 0.0%

- Previous 0.0%

CPI Year-to-Year (YY), Not Seasonally Adjusted (NSA) for November

- Actual: 3.1%

- Previous: 3.2%

In Europe today:

- British wage growth slowed significantly, causing a decline in 10-year yields. The average earnings index fell to 7.2% from 8.0% last month (and lower than the 7.7% expected). The claimant count change came in weaker at 16.0K vs 20.3K estimate

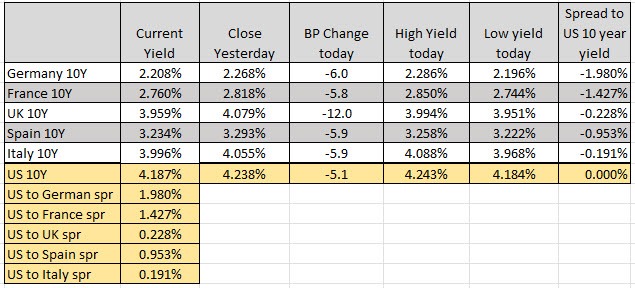

- Euro zone benchmark Bund yields is down around -5 bps and UK 10 year yield is down -12 bps at 3.957% and trades near the low from last week at 3.955% (lowest level since May.

Money markets are pricing in 135 basis points of ECB rate cuts in 2024, a decrease from earlier projections of about -150 basis points but still quite a bullish projection for 2024. .

US stocks are set to open higher (as implied by the futures). The US yields are lower by about 4-5 basis points ahead of the rate decision tomorrow.

A snapshot of the markets to kickstart the North American session shows:

- Crude oil is trading down -$0.37 or -0.53% at $70.94. At this time yesterday, the price was at $70.76

- Spot gold is trading up $7.01 or 0.36% at $1988.66. At this time yesterday, the price is at $1994

- Spot silver trading up $0.14 or 0.63% at $22.95 . At this time yesterday, the price was at $20.92

- Bitcoin is trading at $41,745 . At this time yesterday, the price was trading at $42,287

In the US stock market, the major indices are implying a higher opening after closing higher across-the-board yesterday. All three indices closed yesterday at the highest levels for 2023

- Dow Industrial Average futures are implying a gain of 72 points. Yesterday, the Dow Industrial Average rose 157.06 points or 0.43%.

- S&P index futures are implying a gain of 4.31 points. Yesterday, the S&P index rose 18.07 points or 0.39%.

- NASDAQ index futures are implying 42.76 points . Yesterday, the Nasdaq Index rose 28.52 points or 0.20%.

In the European equity markets, the major indices are trading

- German DAX, -0.14%. Yesterday the index rose 0.21%

- France's CAC, was 0.09% . Yesterday the index rose 0.33%

- UK's FTSE 100, was 0.32%. Yesterday the index fell -0.13%

- Spain's Ibex, -0.67%. Yesterday the index fell -0.25%

- Italy's FTSE MIB, unchanged (10 minute delay). Yesterday the index rose 0.07%

In the Asia Pacific market, major indices

- Japan's Nikkei index, 0.16%. On Monday, the index rose 1.5%

- China's Shanghai Composite Index, 0.40% . On Monday, the index rose 0.74%

- Hong Kong's Hang Seng index, 1.07%. On Monday, the index fell -0.81%

- Australia's S&P/ASX index, 0.50%. On Monday, the index rose 0.06%

In the US debt market, yields are trading higher:

- US 2Y T-NOTE: 4.684%, -4.2 basis points. At this time yesterday, the yield was at 4.758%

- US 5Y T-NOTE: 4.203%, -4.7 basis points. At this time yesterday, the yield was at 4.284%

- US 10Y T-NOTE:4.189%, -5.0 basis points . At this time yesterday, the yield was at 4.272%

- US 30Y BOND: 4.276%, -5.4 basis points. At this time yesterday, the yield was at 4.342%

- 2 – 10-year spread is trading at -49.3 basis points. At this time yesterday, the spread was at more affordable .4 basis points

- 2 – 30 year spread is trading at -40.9 basis points. At this time yesterday, the spread was at -35.7 basis points

In the European debt market, benchmark 10-year yields are trading lower led by the UK 10 year yield after weaker labour data: