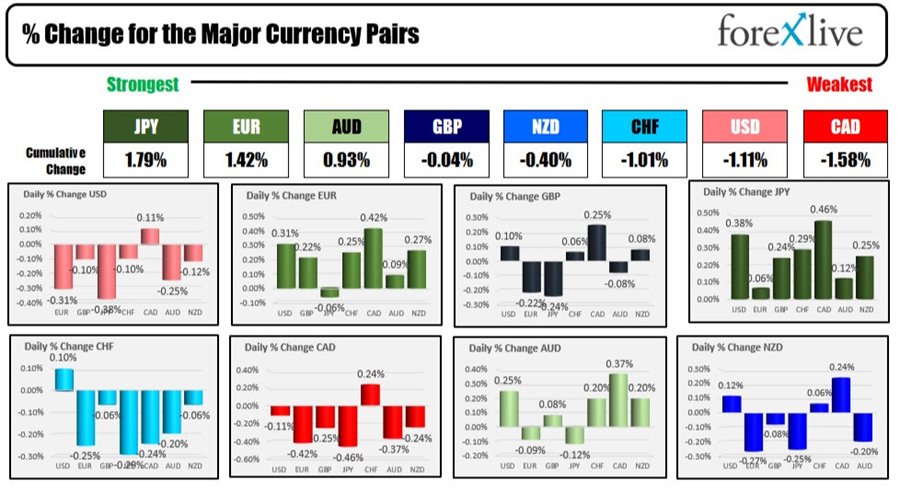

As the North American session gets underway, the JPY is the strongest of the majors (after being the runaway weakest yesterday). The CAD is the weakest. The USD is continuing to drift lower. Yesterday near the close, the USD was mostly lower (up vs the JPY but down or near unchanged vs the rest of the major currencies).

Interest rates are taking a breather in the US with the yields modestly lower. US stocks are mixed but little changed, although the Nasdaq is lower. Crude oil is higher and above $77 (the low in December reached $62.46). Bitcoin is trading down to $46,000 despite a report from Goldman Sachs saying that the digital currency could hit $100,000 in 2022, but with the caveat that it would need to take market share from gold as a safe haven asset.

The ADP release their estimate for payroll for December with expectations at 405,000. The US jobs report from the BLS will be released on Friday with estimates now showing a 426K expectations. The final Markit services PMI will be released at 9:45 AM (the preliminary came in at 57.5). Tomorrow, the ISM services PMI is expected to show a dip to 67.0 from 69.1. The FOMC meeting minutes will be released at 2 PM ET. The Dot plot at the December meeting showed three tightenings by the end of 2022 with the FOMC speeding up the taper so that he can be done near the end of the first quarter. In Europe this morning, the services PMI data was mostly weaker than expectations (Spain, Italy, France, EU are weaker then estimates while Germany was marginally higher).

A snapshot of the market currently shows

- Spot gold is up $3.28 or 0.18% at $1817.48

- Spot silver is down three cents or -0.09% at $23.02

- WTI crude oil is trading at $77.30 that's up $0.31 or 0.39%

- Bitcoin is trading at $46,124. That's little changed from the 5 PM level of $46,153

In the premarket for US stocks, the Dow industrial average is up modestly and has closed at a record level for two consecutive days in 2022. The NASDAQ index is lower as investors demand soured on Tuesday after the move higher on Monday. The futures are implying

- Dow industrial average up 10 points after yesterday's 214.59 point rise

- S&P index -3.5 points after yesterday's -3.04 point decline

- NASDAQ index -50 points after yesterday's -210.08 point decline

The European equity markets, the major indices are moving higher for the third consecutive day in 2022:

- German DAX +0.68% (+0.7% yesterday)

- France's CAC +0.5% (+1.3% yesterday)

- UK's FTSE 100 +0.1% (+1.5% yesterday)

- Spain's Ibex +0.1% (+0.6% yesterday)

- Italy's FTSE MIB +0.25% (+0.4% yesterday)

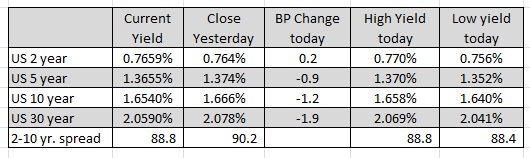

In the US debt market, the yields are modestly lower (with the exception of the two year which is 0.2 basis points). US yields were mixed yesterday with the shorter end lower, while the longer end moved higher. However, yields did come off their highest levels. The 10 year reached 1.686% and sniffed important resistance at 1.705% during trading yesterday.

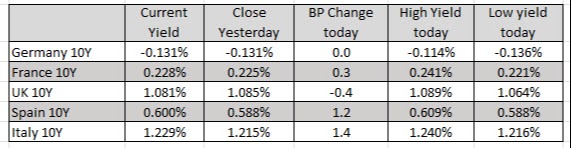

In the European debt market, the benchmark 10 year yields are mostly higher