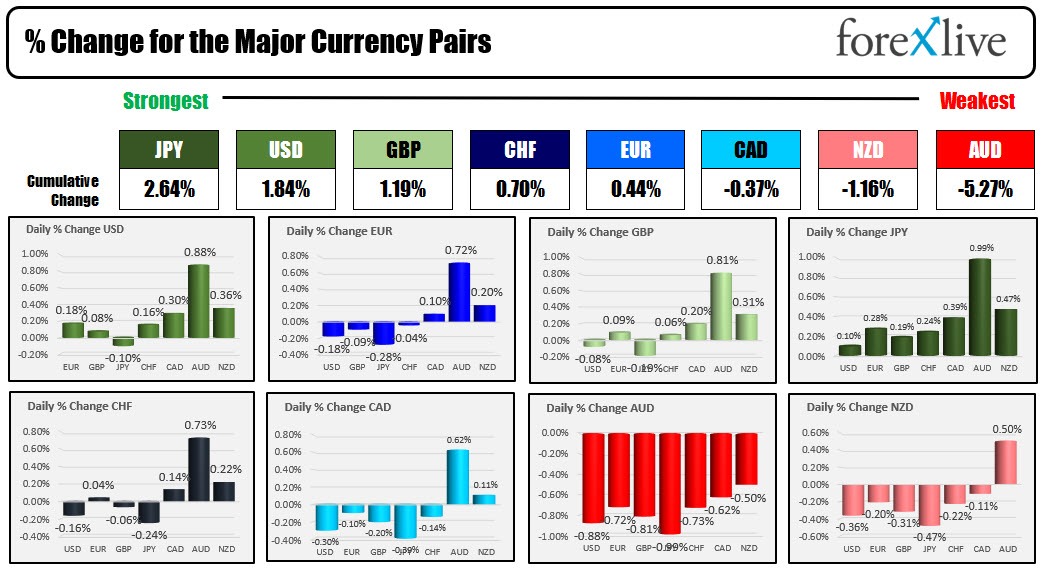

The JPY is the strongest, while the AUD is the weakest as the North American session begins.

Overnight, the Reserve Bank of Australia (RBA) decided to keep the cash rate steady at 4.35%. This decision which was expected to be a "hawkish pause", but instead leaned somewhat dovish. The RBA indicated that future adjustments in monetary policy would depend on incoming data and an evolving assessment of risks. The Board reaffirmed its commitment to bringing inflation back to the target range.

Key observations by the RBA included the following:

- Domestic economic data since November largely met expectations, but the outlook for household consumption remains uncertain.

- The October CPI indicator suggested a moderation in inflation, particularly in the goods sector, although there was less clarity on services inflation.

- Inflation expectations are still aligned with the target.

- Labour market conditions, while gradually easing, continue to be tight.

- The RBA also acknowledged uncertainties around the lagging effects of monetary policy changes.

The RBA highlighted that higher interest rates are helping to balance supply and demand in the economy more sustainably. By maintaining the current cash rate, the RBA aims to better assess the impact of recent rate increases on demand, inflation, and the labor market. This approach suggests a cautious stance in managing economic stability while navigating inflationary pressures and market uncertainties.

The USD/JPY currency pair experienced an increase following the release of Tokyo's inflation data. Although Tokyo's inflation remains well above the 2% target, it was slightly below expectations.

Bank of Japan policy board members have been in the media this and last week hosing down expectations of any pivot before the Spring wage talks:

- BOJ board member Noguchi said only a possibility the 2% inflation target is in sight

- BOJ's Nakamura says it'll be some time before easy money policy is changed

- Bank of Japan's Adachi denies speculation of ending negative interest rates

- BOJ official says yet to see positive wage-inflation cycle - easy policy to remain

Meanwhile, in the Eurozone, ECBs Schnabel, an executive board member of the European Central Bank (ECB), commented on recent inflation trends and monetary policy. She noted that the recent fall in core inflation rates is promising, but cautioned against setting long-term policy directions. Schnabel believes the current level of monetary restriction is adequate and is optimistic about meeting the 2% inflation target by 2025. However, she considers further rate hikes unlikely following the November inflation data, emphasizing the need for gradual progress and warning against declaring an early victory over inflation. She also indicated that there is no expectation of a prolonged recession and suggested that the economy might be starting to recover.

The US Federal Reserve is in its blackout ahead of its December 13 interest rate decision.

Today, the US JOLTs data will be released. The estimates are for job openings to fall to 9.3 million, down from 9.553 million on the last day of the prior month The ISM manufacturing PMI for November is expected to rise to 52.0 from 51.8 last month. Last month the employment index came in at 50.2. The new orders index came in at 55.5.

US stocks are lower after closing lower yesterday to start the trading week. European shares are mostly lower and Asian Pacific shares fell. US yields are lower. Crude oil is down modestly into trading back below $73 after reaching a high of $74.04 overnight. Gold is down modestly after reaching an all-time record yesterday at $2146.79 before backing off and closing lower yesterday.

A snapshot of the markets to kickstart the North American session shows:

- Crude oil is trading down $-0.14 for -0.22% at $72.93. At this time yesterday, the price was at $73.49.

- Spot gold is trading down down -$3.37 or -0.17% at $2025.31. At this time yesterday, the price is at $2068.74. The 38.2% retracement of the move up from the October law comes in a $2018.26. That will be a key barometer for both buyers and sellers going forward.

- Spot silver is trading down $-0.14 or -0.60% at $24.33. At this time yesterday, the price was at $25.16.

- Bitcoin is trading at $41,794. At this time yesterday, the price was at $41,859.

In the US stock market, the major indices are implying a lower opening after starting the week with declines yesterday

- Dow Industrial Average is trading down -74 points. Yesterday the Dow Industrial Average fell -41.06 points or -0.11%.

- S&P index is trading down -16.75 points. Yesterday the S&P index fell -24.87 points are -0.54%.

- NASDAQ index is down -83 points. Yesterday the Nasdaq Index fell -119.55 points or -0.84%.

In the European equity markets, the major indices are trading mixed.

- German DAX, is trading up 0.28%. Yesterday the German DAX fell -0.09%.

- France's CAC, is trading up 0.36%. Yesterday France CAC fell -0.18%.

- UK's FTSE 100, is trading down -0.48%. Yesterday UK's FTSE 100 fell -0.22%.

- Spain's Ibex, up up 0.29%. Yesterday Spain's Ibex rose 0.37%.

- Italy's FTSE MIB, and changed (10 minute delay). Yesterday Italy's FTSE MIB fell -0.05%.

In the Asia Pacific market major indices all fell:

- Japan's Nikkei index, -1.37%

- China's Shanghai composite index, -1.67%

- Hong Kong's Hang Seng index, -1.91%

- Australia's S&P/ASX index, -0.89%

In the US debt market, yields are trading :

- US 2Y T-NOTE: 4.612% -4.0 basis points. At this time yesterday, the yield was at 4.508%.

- US 5Y T-NOTE: 4.187% -5.2 basis points. At this time yesterday, the yield was at 4.190%.

- US 10Y T-NOTE: 4.226% -6.0 basis points. At this time yesterday, the yield was at 4.249%.

- US 30Y BOND: 4.384% -5.3 basis points. At this time yesterday, the yield was at 4.420%.

- 2 – 10-year spread is trading at -38.8 basis points. At this time yesterday, the spread was at -35.9 basis points

- 2 – 30 year spread is trading at -23.3 basis points. At this time yesterday, the spread was at -18.9 basis points

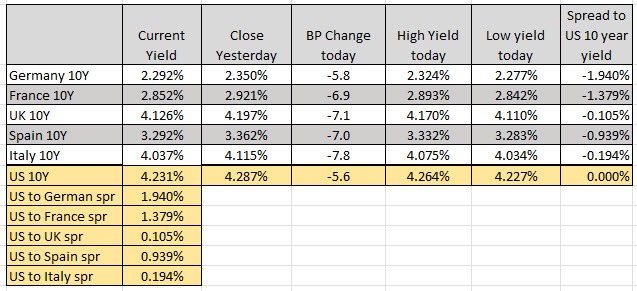

In the European debt market, benchmark 10-year yields are trading lower: