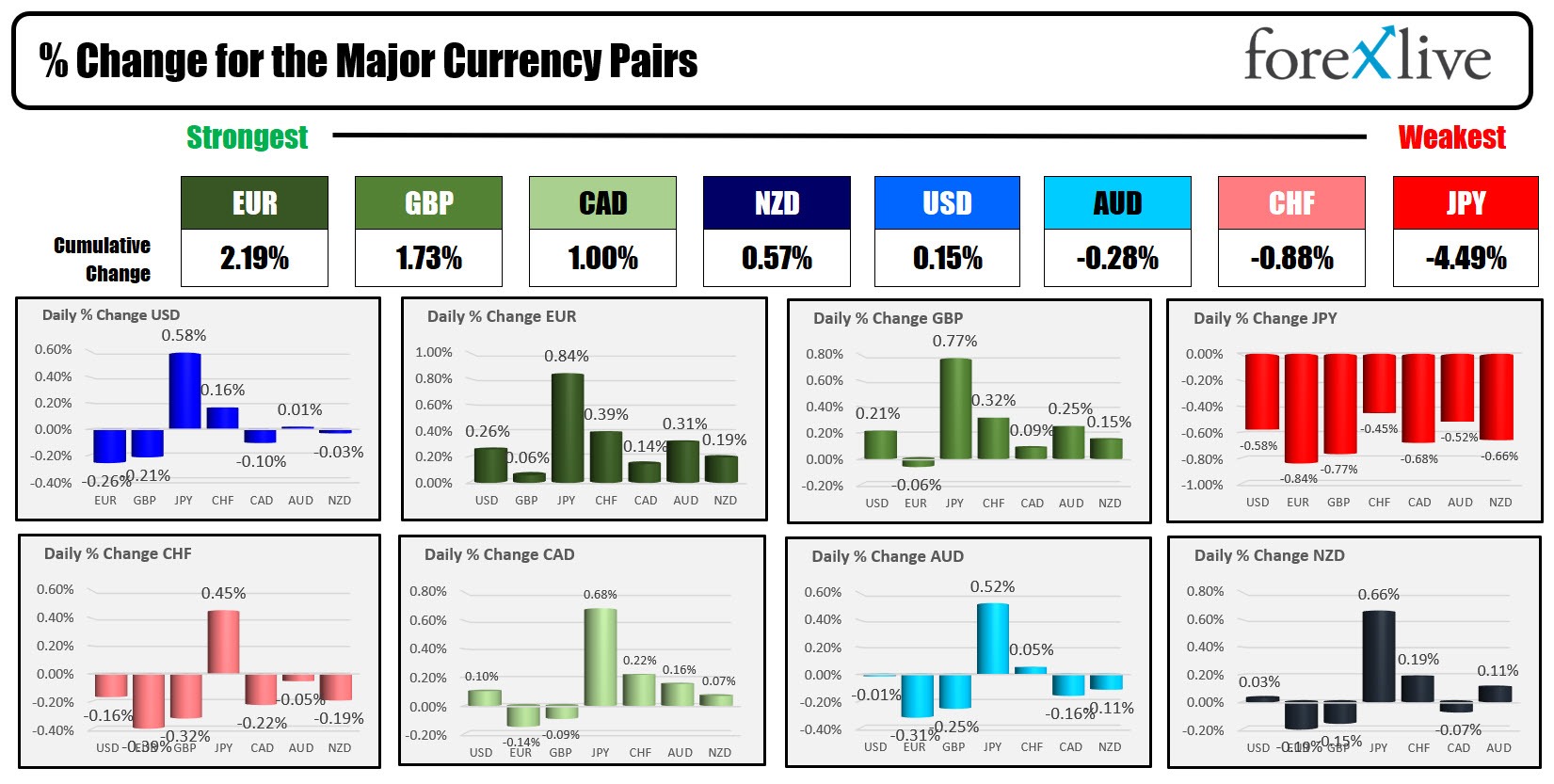

As the North American session begins, the EUR is the strongest while the JPY is the weakest. The USD is mixed to start the trading day with the greenback lower vs the EUR and GBP, and higher vs the JPY and CHF. The dollar is little changed vs the CAD, AUD, and NZD.

The focus today will be on the ADP employment data which will be released at 8:15 AM with expectations of 115K vs 103K last month. The weekly US initial jobless claims will also be a focus with expectations of 216K vs 218K last week. The more important BLS employment data for December will be released tomorrow at 8:30 AM ET. Expectations are for a gain of 168K versus 199K last month. The unemployment rate is expected to come in at 3.8% versus 3.7%. At 9:45 AM ET, the final S&P global services PMI index will be release with expectations of 51.3 versus the primary estimate of 51.3.

In Europe, their final Purchasing Managers' Index (PMI) data out of Europe today indicates mixed results, with some countries showing stronger data and others weaker:

Spanish Services PMI: It reported a figure of 51.5, which is slightly stronger than both the forecast of 51.1 and the previous value of 51.0. This indicates a modest expansion in the services sector.

Italian Services PMI: This came in at 49.8, exactly as forecasted, and higher than the previous value of 49.5. While this is an improvement, a figure below 50 still indicates a contraction in the sector.

French Final Services PMI: The French data showed significant strength, coming in at 45.7, which is higher than both the forecast and previous figure of 44.3. However, it's still below 50, indicating contraction, but it's an improvement over the previous period.

German Final Services PMI: This reported a figure of 49.3, stronger than the forecast of 48.4 and the previous figure, also 48.4. Like Italy, Germany's PMI is below 50, indicating contraction, but the data is showing improvement.

Eurozone Final Services PMI: The overall PMI for the Eurozone was 48.8, which is stronger than the forecast of 48.1 and the previous value of 48.1. This suggests a contraction in the services sector across the Eurozone but an improvement over the previous period.

UK Final Services PMI: The PMI for the UK was quite strong, reporting at 53.4, above the forecast and previous value of 52.7, indicating expansion in the services sector.

France's preliminary CPI came in at 0.1% versus 0.2% expected. The last four months have seen a decline of -0.5%, +0.1%, -0.2% and +0.1% (that sums to -0.5%). That's the good news. The bad news is that five months ago the price index rose 1.0%. Nevertheless over five months, the monthly CPI data shows a gain of 0.5% (average of 0.1% per month).

Germany's preliminary CPI data just came out at 0.1% versus 0.1% expected. The urine year came in at 3.7 versus 3.7% expected and 3.2% last month. The HICP preliminary data came in 2.2% versus 0.3% expected with year on year at 3.8% versus 3.0% expected

A snapshot of the markets as the North American session begins currently shows:

- Crude oil is trading up up $0.79 or 1.10% at $73.50. At this time yesterday, the price was at $70.79

- Gold is trading up up $5.13 or 0.25% at $2046.27. At this time yesterday, it was trading at $2046.51

- Silver is trading up unchanged at $22.97. At this time yesterday, it was trading at $23.30

- Bitcoin traded at $43,420. At this time yesterday, the price was trading at $45,452.

In the premarket for US stocks, the major indices are trading mixed after all three indices fell yesterday. The Dow Industrial Average and S&P indices are up in premarket trading. The Nasdaq index is down for the third consecutive day in the new year. The NASDAQ has lost -1.63% and -1.18% in the first two days of the year.

- Dow Industrial Average futures are implying a gain of 74 points.. Yesterday the index fell -284.85 points or -0.76% at 37430.20

- S&P futures are implying a gain of 1 point. Yesterday the index fell -38 points or -0.80% at 4704.82

- Nasdaq futures are implying a decline of -24.7 points. Yesterday, the index fell -173.73 points or -1.18% at 14592.21

In the European equity markets, the major indices are all trading lower:

- German DAX, +0.15 percent

- France CAC +0.25%

- UK FTSE 100 +0.27%

- Spain's Ibex +0.78%

- Italy's FTSE MIB was 0.22% major indices closed mixed:

Shares in the Asian Pacific markets were mostly lower:

- Japan's Nikkei 225, -0.53%

- China's Shanghai composite index , -0.43%

- Hong Kong's Hang Seng index, unchanged

- Australia S&P/ASX -0.39%

Looking at the US debt market, yields are trading higher:

- 2-year yield 4.349% +3.1 basis points. Yesterday at this time, the yield was at 4.353%

- 5-year yield 3.936% +4.2 basis points. Yesterday at this time, the yield was at 3.957%

- 10-year yield 3.953% +4.6 basis points. Yesterday at this time, the yield was at 3.976%

- 30-year yield 4.106% +4.9 basis points. Yesterday at this time, the yield was at 4.121%

- The 2-10 year spread is at -39.2 basis points. At this time yesterday, the spread was at -37.5 basis points

- The 2-30 year spread is at -24.0 basis points. At this time yesterday, the spread was at -22.8 basis points

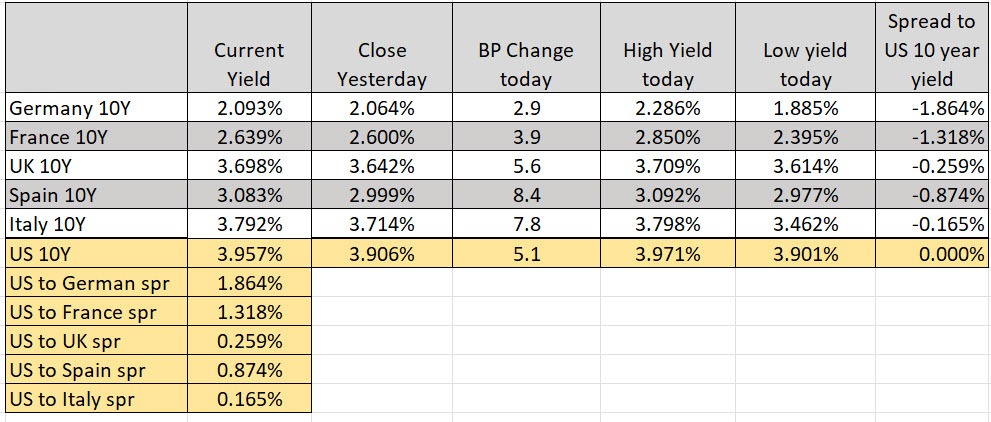

In the European debt market, the benchmark 10-year yields are higher: