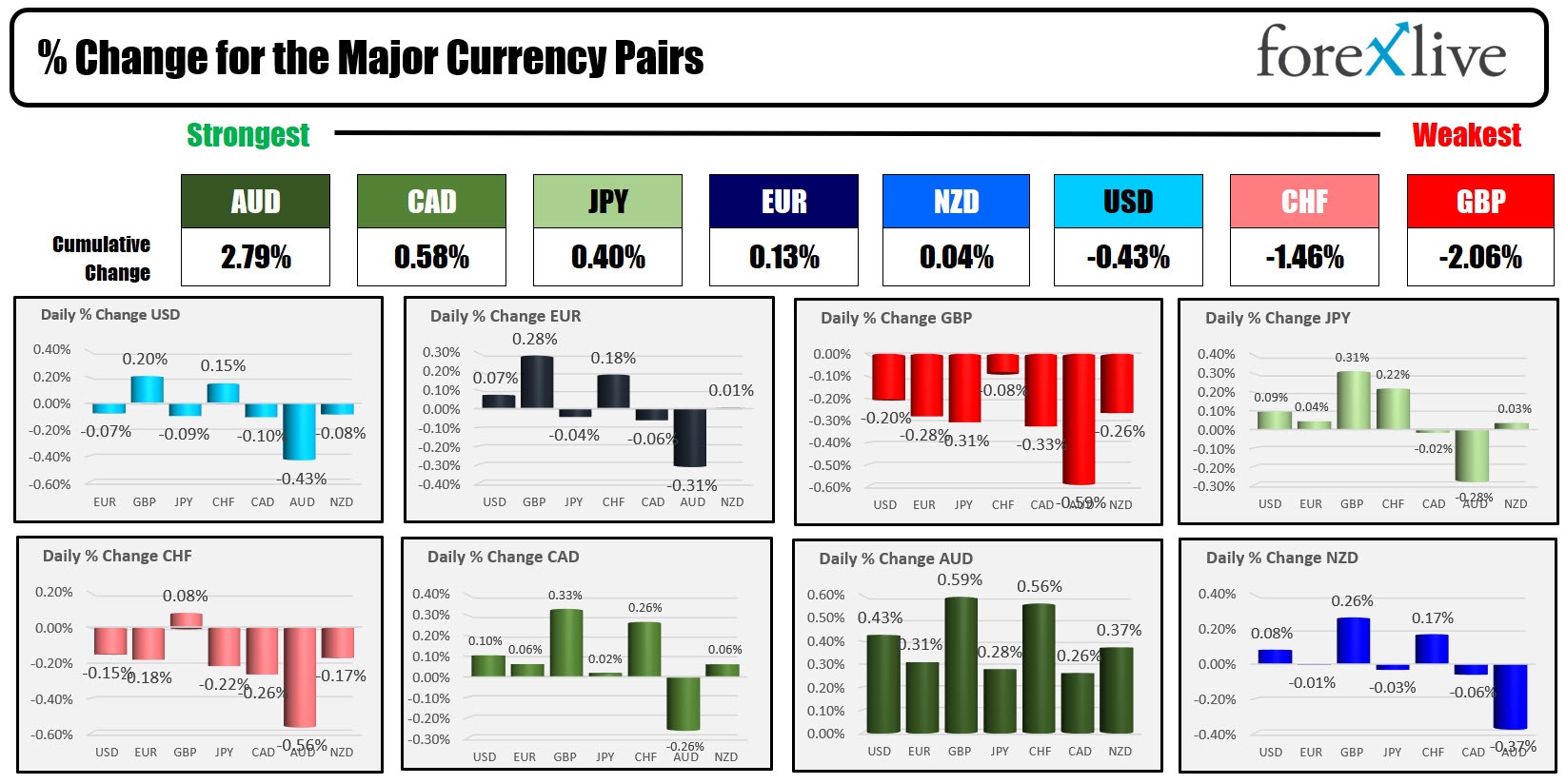

The AUD is the strongest and the GBP is the weakest as the North American session begins. The USD is mixed with the largest decline vs the AUD (-0.43%) and the largest increase vs the GBP (+0.20%)/ The other USD changes vs the major currencies are 0.15% or lower.

In Europe, the UK retail sales experienced a significant decline in retail sales, underperforming expectations across several key metrics. The headline number fell -3.2% vs -0.5% estimate. Excluding fuel, year-on-year (YY) sales decreased by -2.1%, notably below the anticipated 1.3% growth. The month-on-month (MM) figures were similarly disappointing, with a ex fuel -3.3% decline compared to an expected drop of just -0.6%, a stark contrast to the previous month's 1.5% increase (revised from 1.3%).

YoY, the headline retail sales fell by -2.4%, greatly missing the expected 1.1% increase. The Office for National Statistics (ONS) attributed part of this decline to consumers purchasing food and Christmas gifts earlier in November, which contributed to the steeper-than-expected drop in December sales.

Swiss PPI data showed a decline of -0.6% vs -0.6% estimate. That decline comes after a -0.9% decline last month. The SNBs Jordan said that additional rate hikes from the SNB are not necessary to maintain price stability

Today in the North American session, Canada will release their retail sales with expectations of unchanged versus 0.7% last month. Ex autos, the expectations are -0.1% (vs 0.6% last month). In the US, existing home sales for December are expected at 3.82M unchanged from last month. The Michigan consumer sentiment is expected at 70.0 vs 69.4 last month. The one-year inflation expectations last month came in 3.1%. The five year inflation came in 2.8%..

As a reference, the pre-pandemic one-year inflation expectations (going back to the end of 2016), was mostly between 2.3% and 3.0% (see chart below). If the expectations can move into that range, the confidence increases for cuts in 2024.

A snapshot of the markets as the North American session begins currently shows:

- Crude oil is trading unchanged at $73.95 At this time yesterday, the price was at $72.56

- Gold is trading up $9.89 or 0.48% at $2033.40. At this time yesterday, it was trading at $2015.91

- Silver is trading up $0.06 or 0.29% at $22.79. At this time yesterday, it was trading at $22.62

- Bitcoin traded at $41,314. At this time yesterday, the price was trading at $42,424

In the premarket for US stocks, the major indices are trading higher. Yesterday, all the indice moved higher. The S&P index in premarket trading is trading above the all-time high close of 4796.57. For the week, the major indices are mixed using the closes from yesterday:

- Dow Industrial Average futures are implying a gain of 200.1 points. Yesterday, the index rose 201.94 points or 0.54%. For the week, the index is down -0.33%.

- S&P futures are implying a gain of 26 points. Yesterday, the index rose 41.73 points or 0.80%. For the week, the index is down -0.06%.

- Nasdaq futures are implying a gain of 134 points. Yesterday, the index rose 200.03 points or 1.35%.. For the week the index is up 0.55%

In the European equity markets, the major indices are all trading higher, but for the week, the indices are all on pace for a lower close:

- German DAX, 0.19%. For the week, the index is down -0.62%

- France CAC +0.02%. For the week the index is down -0.83%

- UK FTSE 100 +0.37% . For the week the index is down -1.81%

- Spain's Ibex +0.08%. For the week the index is down -2.08%

- Italy's FTSE MIB 0.19% (delayed by 10 minutes).

Shares in the Asian Pacific markets were mixed. Shares for the week saw gains in Japan, but China, Hong Kong and Australia all declined.

- Japan's Nikkei 225, - +1.40%. For the week the index rose 1.08%

- China's Shanghai composite index , -0.47%. For the week, the index fell -1.72%

- Hong Kong's Hang Seng index, -0.54%. For the week,, the index fell -5.76%

- Australia S&P/ASX, +1.02%. For the week, the index fell -1.0%

Looking at the US debt market, yields are trading mixed with the shorter paint higher in the water and a lower.

- 2-year yield 4.356% unchanged. Yesterday at this time, the yield was at 4.320%

- 5-year yield 4.043% -0.5 basis points. Yesterday at this time, the yield was at 4.002%

- 10-year yield 4.134%, -0.8 basis points. Yesterday at this time, the yield was at 4.090%

- 30-year yield 4.359%, -1.3 basis points. Yesterday at this time, the yield was at 4.313%

- The 2-10 year spread is at -24.1 basis points. At this time yesterday, the spread was at -24.1 basis points

- The 2-30 year spread is at -1.7 basis points. At this time yesterday, the spread was at -1.7 basis points

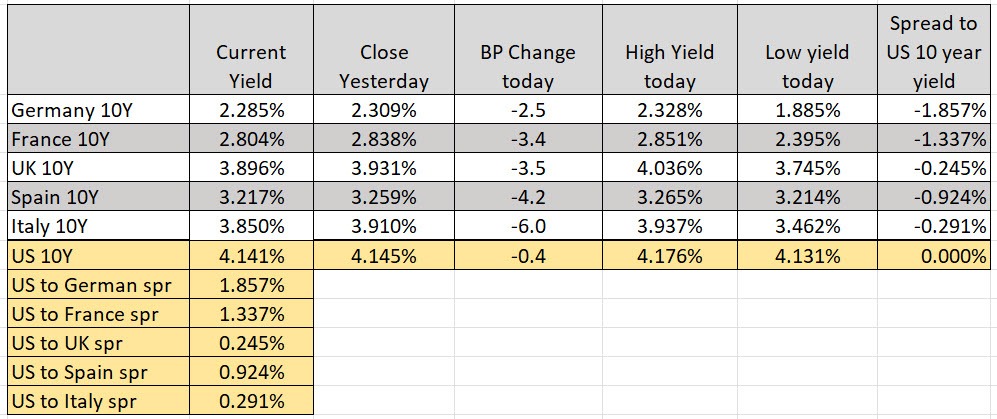

In the European debt market, the benchmark 10-year yields are lower: