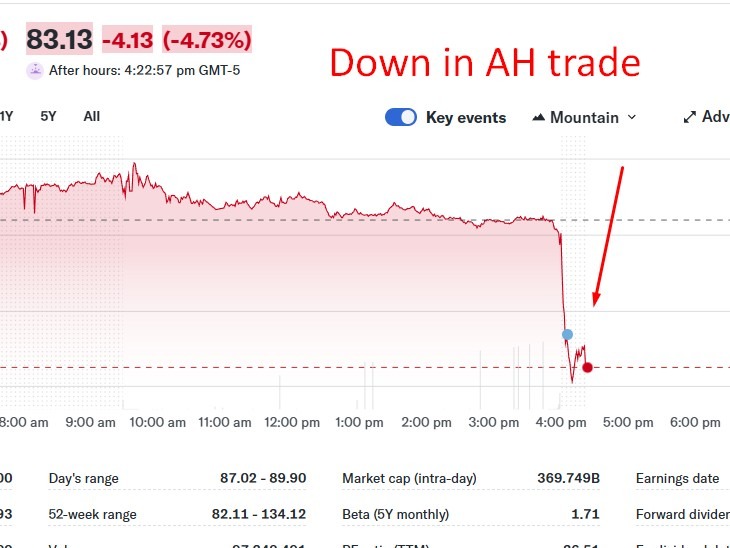

Netflix beat Q4 estimates but warned higher content spend and acquisition costs will weigh on margins before growth re-accelerates.

Summary:

Q4 earnings and revenue modestly beat expectations, with strong free cash flow.

Q1 operating income and margin guidance missed consensus.

Netflix plans a 10% increase in 2026 content spending, pressuring margins.

Warner deal adds $275m in costs and triggers a pause in buybacks.

Advertising revenue seen doubling in 2026, with stronger 2H income growth.

Netflix delivered a modest earnings beat in the December quarter but struck a cautious tone on near-term profitability, warning that higher content spending and acquisition-related costs will weigh on margins through 2026.

The streaming giant reported Q4 EPS of $0.56, narrowly ahead of expectations and up sharply from a year earlier, while revenue of $12.05bn also topped forecasts. Free cash flow came in well above estimates at $1.87bn, underscoring Netflix’s still-strong cash generation despite rising investment.

Looking ahead, however, guidance disappointed at the margin level. Netflix sees Q1 revenue broadly in line with consensus but forecast operating income and margins below expectations, reflecting higher production spending and incremental costs tied to its pending acquisition of Warner Bros. Discovery assets. Management said the transaction will add around $275m in costs this year and has prompted a pause in share buybacks to preserve balance-sheet flexibility.

For 2026, Netflix guided to revenue of $50.7bn–$51.7bn, broadly in line with market expectations, but operating margin guidance of 31.5% fell short of consensus. Free cash flow is seen at roughly $11bn, slightly below estimates, as the company plans to lift content spending by around 10% following approximately $18bn spent on programming in 2025.

Strategically, Netflix reiterated confidence in its longer-term growth profile. Management said operating income growth in the second half of 2026 is expected to exceed the first half, while advertising revenue is projected to roughly double versus 2025 levels as its ad-supported tier scales globally.

Subscriber momentum remained solid, with Netflix ending the year with more than 325 million subscribers, up nearly 8% year on year. Still, the outlook reinforced investor concerns that elevated content investment and integration costs could cap upside to margins in the near term, even as revenue growth and cash generation remain robust.