EUROPEAN SESSION

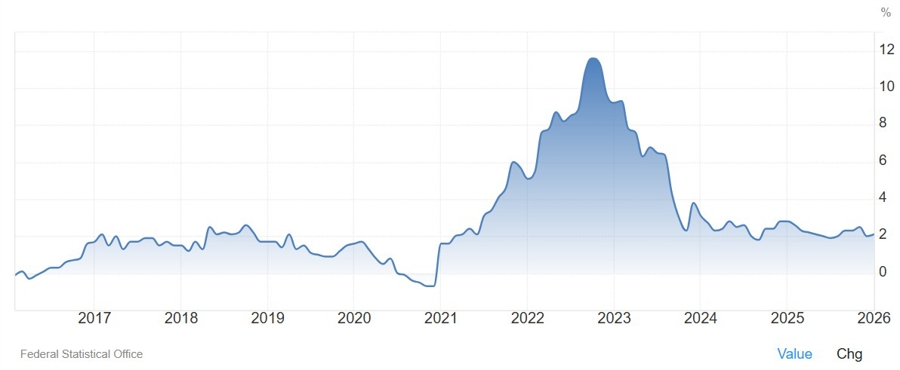

In the European session, the main highlight is going to be the German inflation data both the state readings and the national CPI. We will also get the French and Spanish inflation figures, but the German data is generally more market-moving because it carries more weight in the Eurozone CPI calculations. The German CPI Y/Y is expected at 2.0% vs 2.1% prior.

We also have the French and Swiss Q4 GDP reports, but these will be the final readings, so they won't be market-moving and won't change anything for the respective central banks.

AMERICAN SESSION

In the American session, the focus will turn to the Canadian GDP and the US PPI. The Canadian GDP for December is expected at 0.1% vs 0.0% prior. The data is very unlikely to change anything for the BoC at this point as the central bank wait for more recent data and especially the USMCA developments.

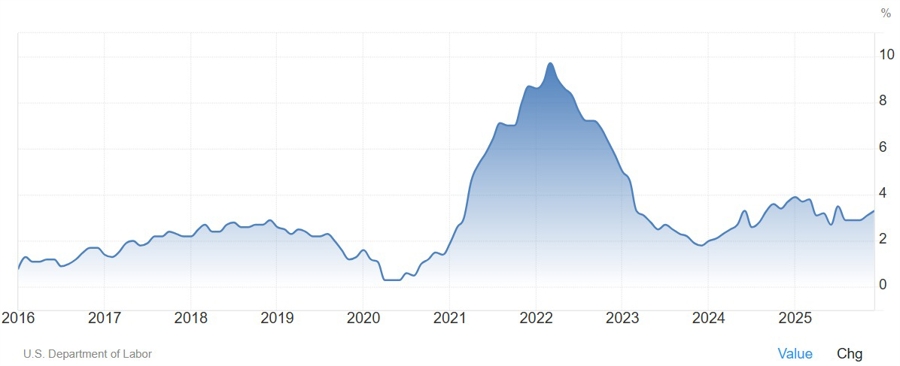

The US PPI Y/Y is expected at 2.6% vs 3.0% prior, while the Core PPI Y/Y is seen at 3.0% vs 3.3% prior. Several of PPI specific sub-components feed into PCE calculations, so we will get more precise PCE forecasts after the data. Right now, analysts see the Core PCE in January to have risen around 0.3% due to stubborn service-sector costs.

CENTRAL BANK SPEAKERS

- 13:00 GMT/08:00 ET - BoE's Pill (hawkish - voter)