Today things finally pick up on the data front as we get lots of economic releases. The highlights include the German inflation readings, the UK budget announcement, the Treausury refunding announcement and the US ADP report. We will also see the Q3 GDP report for the Eurozone and the US but, as always, GDP is old news as the market is already looking forward to Q1/Q2 2025.

Overall though, the focus remains on the US election and I feel like the market will largely ignore the data this week, especially given the negative distortions expected to make the US NFP report on Friday trickier to interpret.

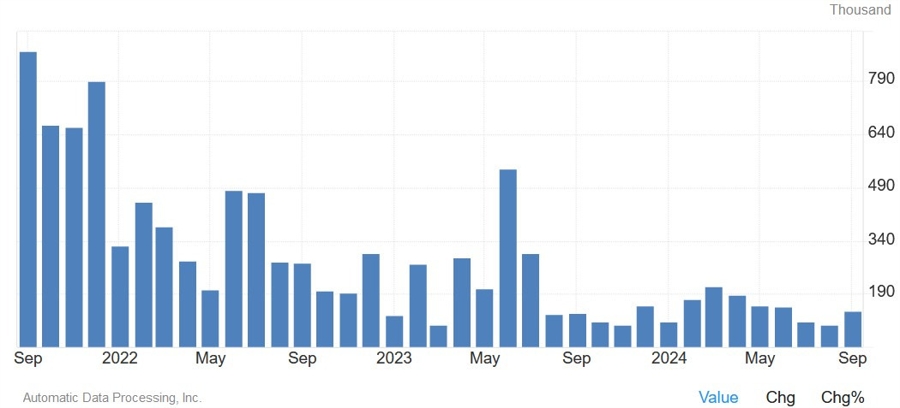

12:15 GMT/08:15 ET - US October ADP

The US ADP is expected to show 115K jobs added in October vs. 143K in September. The last report surprised to the upside triggering a hawkish repricing in interest rates expectations. Although the ADP has a poor track record in predicting the NFP data, the recent market’s sensitivity to labour market data makes it a bit more important.

Central bank speakers:

- 15:00 GMT/11:00 ET - ECB's Schnabel (neutral - voter)

- 20:15 GMT/16:15 ET - BoC's Macklem/Rogers