Monday

Monday was an empty day on the data front with just a couple of notable events:

- We haven’t seen a ground offence in Gaza over the weekend, although the airstrikes continued. Nonetheless, the risk sentiment improved as the ground operation is seen as the biggest risk by the markets. Later in the day, we have also got a report that Hamas was releasing two hostages in response to a Qatari-Egyptian mediation.

- Treasury yields fell across the board following a tweet from Bill Ackman where he said that he covered his bond short position due to “the economy slowing faster than the recent data suggests”. Later on, Bill Gross, former PIMCO fund manager, said that “higher for longer is yesterday’s mantra” as he sees a US recession in Q4.

Tuesday

Tuesday was the PMIs Day with most of them disappointing, except the US ones:

- Australia Manufacturing PMI 48.0 vs. 48.7 prior.

- Australia Services PMI 47.6 vs. 51.8 prior.

- Japan Manufacturing PMI 48.5 vs. 48.5 prior.

- Japan Services PMI 51.1 vs. 53.8 prior.

- Eurozone Manufacturing PMI 43.0 vs. 43.7 expected and 43.4 prior.

- Eurozone Services PMI 47.8 vs. 48.7 expected and 48.7 prior.

- UK Manufacturing PMI 45.2 vs. 44.7 expected and 44.3 prior.

- UK Services PMI 49.2 vs. 49.3 expected and 49.3 prior.

- US Manufacturing PMI 50.0 vs. 49.5 expected and 49.8 prior.

- US Services PMI 50.9 vs. 49.8 expected and 50.1 prior.

The rest of the UK’s labour market report beat expectations although it doesn’t change anything for the BoE at this point in time:

- Employment change -82K vs. -198K expected and -207K prior.

- Unemployment rate 4.2% vs. 4.3% expected and 4.3% prior.

RBA’s Governor Bullock just reaffirmed her focus on bringing inflation back to target “within a reasonable timeframe”:

- Focused on brining inflation to target within reasonable timeframe.

- There are risks inflation could return to target more slowly than forecast.

- Will not hesitate to raise rates if there is a material upward revision to inflation outlook.

- Australian dollar is relatively stable in trade-weighted terms, not a policy concern.

ECB’s Makhlouf (dove – non voter) is watching the developments in the Middle East closely as an expansion of the conflict could cause another wave of energy inflation:

- Far too early to tell consequences of Middle East situation.

- We are watching the developments very closely.

- They are bound to have economic implications for us to some extent.

- Don't want to jump to conclusions on extent of impact on economies, monetary policy.

ECB’s President Lagarde (neutral – voter) is acknowledging the positive developments on the inflation front but warns about stagnation in the next few quarters:

- Inflation fight is going well.

- Eurozone economy to stagnate in the next few quarters.

- Risks to inflation have become more balanced.

- Fiscal impasse is starting to turn into a headache.

China has approved $139bn in new bonds (1 trillion yuan) to bolster the economic recovery as the stimulus widens the deficit to 3.8% from 3.0% this year. This has led to a rally in Chinese risk assets, although the gains were completely erased the day after.

Wednesday:

The Australian Q3 CPI data beat expectations across the board leading the market to price in a higher chance of a 25 bps rate hike from the RBA in November:

- CPI Y/Y 5.4% vs. 5.3% expected and 6.0% prior.

- CPI Monthly Y/Y 5.6% vs. 5.4% expected and 5.2% prior.

- CPI Q/Q 1.2% vs. 1.1% expected and 0.8% prior.

- CPI Trimmed Mean Y/Y 5.2% vs. 5.0% expected and 5.9% prior.

- CPI Trimmed Mean Q/Q 1.2% vs. 1.1% expected and 1.0% prior (revised from 0.9%).

- CPI Weighted Mean Y/Y 5.2% vs. 5.0% expected and 5.4% prior (revised from 5.5%).

- CPI Weighted Mean Q/Q 1.3% vs. 1.0% expected and 1.0% prior.

The German IFO Business Climate Index beat expectations:

- IFO Index 86.9 vs. 85.9 expected and 85.8 prior (revised from 85.7).

- Current conditions 89.2 vs. 88.5 expected and 88.7 prior.

- Expectations 84.7 vs. 83.3 expected and 83.1 prior (revised from 82.9).

The BoC left interest rates unchanged at 5.00% as expected:

- BoC sees "clearer signs that monetary policy is moderating spending and relieving price pressures".

- "There is growing evidence that past interest rate increases are dampening economic activity and relieving price pressures".

- BoC repeated that it " is prepared to increase the policy interest rate further if needed".

- Sees inflation returning to 2% at the end of 2025 vs. "mid-2025" previously.

- The global economy is slowing, and growth is forecast to moderate further as past increases in policy rates and the recent surge in global bond yields weigh on demand.

- Weaker demand and higher borrowing costs are weighing on business investment.

- The surge in Canada’s population is easing labour market pressures in some sectors while adding to housing demand and consumption.

- The labour market remains on the tight side and wage pressures persist.

- A range of indicators suggest that supply and demand in the economy are now approaching balance.

- The BoC projects global GDP growth of 2.9% this year, 2.3% in 2024 and 2.6% in 2025, little changed from previously.

- Growth in the euro area has slowed further.

New forecasts:

- Cuts 2023 growth forecast to 1.2% vs. 1.8% prior.

- 2024 to 0.9% vs. 1.2% prior.

- 2025 to 2.5% vs. 2.4% prior.

- Raises 2023 inflation forecast to 3.9% vs. 3.7% prior.

- 2024 inflation to 3.0% vs. 2.5% prior.

- 2025 inflation to 2.2% vs. 2.1% prior.

Moving on to the Press Conference, BoC Governor Macklem and BoC’s Rogers gave their remarks on the policy decision:

- Inflation is on a higher path than we expected.

- Demand pressures have eased more quickly than we forecast in July.

- Overall inflation risks have increased since July.

- We held policy rate steady because we want to allow monetary policy time to cool economy.

- Worried higher energy prices and persistence in underly inflation are slowing progress.

- We've made a lot of progress but we're not there yet.

- We now expect oil prices to remain higher than we assumed in July.

- The exchange rate is part of how monetary policy works.

- Normally large rate hikes boost the currency but because the US is also hiking, the currency has been relatively stable.

- We don't target the exchange rate, but we take it into account.

- We are seeing clear evidence that higher rates are working.

- We left the door open to higher interest rates, if needed.

- We need to see clear downward momentum in core inflation.

- There could certainly be two or three quarters of negative growth.

- A path to a soft landing in Canada is narrower vs USA.

- Highlights the difference between US and Canadian mortgage markets.

- BoC’s Rogers: Relative to interest rates, we're not seeing the drop in housing prices we'd expect.

- BoC’s Rogers: Canada continues to suffer from a lack of housing supply.

- BoC’s Rogers: We're paying very close attention to the mortgage-renewal cycle.

- BoC’s Rogers: Will look more at housing in November Financial System Review.

- Government spending doesn't look like it's been adding undue inflation pressure in the past year.

- It's easier to get inflation down if governments and central banks are moving in the same direction.

- Now is not the time to discuss reductions in the overnight rate.

- Says he wouldn't use the term 'stagflation'.

- The risks that oil could go a lot higher have increased.

The following day we got comments from Macklem on CBC Radio where he said that the economy was not overheated anymore and if inflation were to cool as projected, the BoC wouldn’t have to raise rate further.

The Israeli PM Netanyahu delivered a speech late in the day that triggered risk aversion across the markets as he said that they were “preparing for a ground invasion”. This was preceded by a WSJ report where it was said that the US requested to delay the invasion so it could get more missile defences in place:

- Doing everything possible to bring hostages home.

- We are preparing for a ground invasion.

- I won’t give the details.

- Timing of the invasion will be reached by consensus.

- Civilians in Gaza should move to the South.

- We encourage Israel citizens to carry arms.

- I will have to answer for what happened on October 7.

Thursday

RBA Governor Bullock surprisingly downplayed the higher-than-expected CPI report with the markets trimming the rate hike odds as a consequence:

- The CPI was a little higher than we expected.

- But CPI was about where we thought it would come.

- Goods prices coming down, but services inflation remains persistent.

- Services inflation is higher than what we are comfortable with.

- Will have to build this into our forecasts.

- The longer inflation remains outside target band the more likely inflation expectations change.

- RBA has always had a low tolerance for inflation.

- RBA aims to slow the economy without tipping it into recession.

- She says the Bank is still thinking about if yesterday's inflation data showed a "material" change to policy outlook.

- Would not like to say if CPI makes a rate rise more likely.

- We are wary on inflation.

- We have made it clear we might have to hike interest rates again.

The ECB left interest rates unchanged as widely expected:

- Incoming information has broadly confirmed previous assessment of medium-term inflation outlook.

- Inflation is still expected to stay too high for too long.

- Past interest rate increases continue to be transmitted forcefully into financing conditions.

- This is increasingly dampening demand and thereby helps push down inflation.

- Key interest rates at levels that, maintained for a sufficiently long duration, will make a substantial contribution to ensure that inflation returns to its 2% medium-term target in a timely manner.

- Future decisions will ensure that policy rates will be set at sufficiently restrictive levels for as long as necessary.

- To continue data-dependent approach to determining the appropriate level and duration of restriction.

Moving on to President Lagarde’s Press Conference, she reiterated that rates held for longer will curb inflation and highlighted the weakening economic growth:

- Past hikes are increasingly dampening demand.

- Rates will make a 'substantial contribution' to curbing inflation.

- The eurozone economy remains weak.

- Tighter conditions are weighing on investment and savings; highlights drag from industrial sector.

- Economy is likely to remain weak for the remainder of this year.

- There are signs that the labour market is weakening.

- Food price inflation slowed again, though it remains high by historical standards.

- Risks to economic growth remain tilted to the downside.

- Domestic price pressures remain strong.

- Credit dynamics have weakened further.

- Now is not the time for forward guidance, it's time for data dependency.

- PEPP wasn't discussed at this meeting.

- Our determination to bring inflation to 2% is intact.

- Rise in yields is a spillover that we take into account, it helps bring inflation down.

- What we are seeing is a very-strong transmission of our monetary policy in the banking system in particular.

- Hold doesn't mean we will never hike again.

- We know that growth has weakened, we will have no forecasts in December.

- PMI numbers are not indicative of vigorous growth.

- Decision was unanimous.

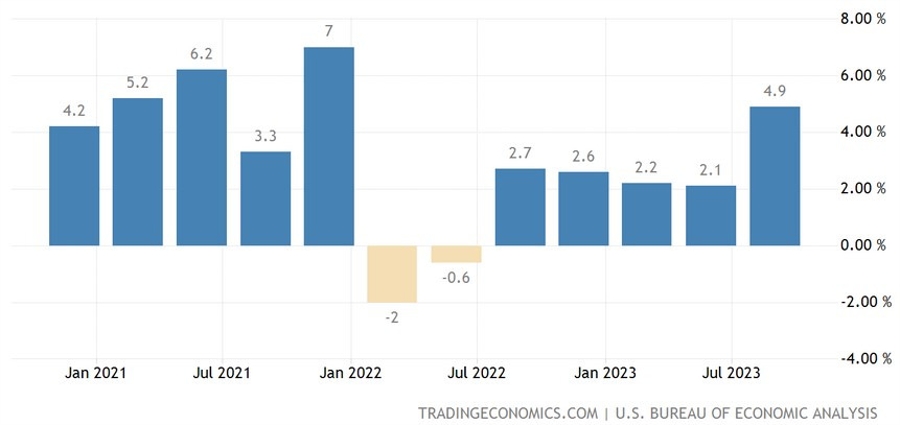

The US Q3 Advance GDP beat forecasts coming in at 4.9% vs. 4.3% expected:

- Final Q2 reading was 2.4% annualized.

- Q1 was 2.0% annualized.

- Best quarter since Q4 2021.

- Estimates ranged from 2.5%-6.0%.

Details:

- Consumer spending 4.0% vs. 0.8% prior.

- GDP final sales 3.5% vs. 4.5% expected and 2.3% prior.

- GDP deflator 3.5% vs. 2.5% expected and 2.2% prior.

- Core PCE 2.4% vs. 2.5% expected and 3.8% prior.

- Exports 6.2% vs. -9.3% prior.

- Imports 5.7% vs. -7.6% prior.

- Business investment 8.4% vs. 5.2% prior.

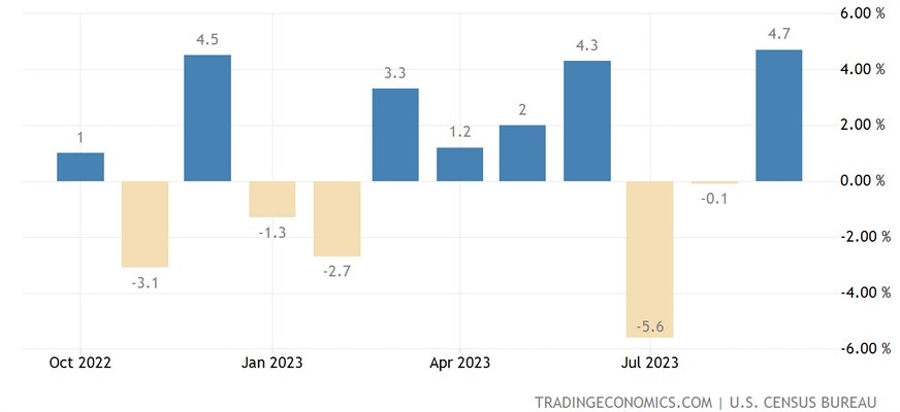

The US Durable Goods orders beat expectations:

- Durable Goods 4.7% vs. 1.7% expected and -0.1% prior (revised from 0.2%).

- Nondefense capital goods orders ex air 0.6% vs. 1.1% prior (revised from 0.9%).

- Ex Transportation 0.5% vs. 0.2% expected and 0.5% prior (revised from 0.4%).

- Ex Defense 5.8% vs. -0.7% prior.

- Shipments -$0.8 billion or -0.3 percent to $283.7 billion. This followed a 0.5 percent August increase.

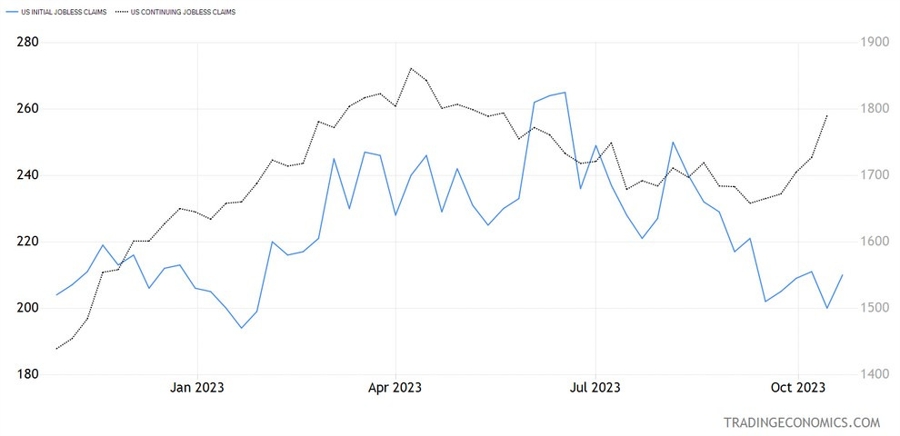

The US Jobless Claims missed expectations across the board this time with Continuing Claims now showing a strong upward trend:

- Initial Claims 210K vs. 208K expected and 198K prior.

- Continuing Claims 1790K vs. 1.740K expected and 1.727K prior (revised from 1.734K).

Friday

The Tokyo CPI, which is seen as a leading indicator for National CPI, came in higher than the prior figures:

- CPI 3.3% vs. 2.8% prior.

- CPI ex Food 2.7% vs. 2.5% expected and 2.5% prior.

- CPI ex Food and Energy 2.7% vs. 2.4% prior.

The Australian Q/Q PPI came in higher than the prior month:

- PPI Q/Q 1.8% vs. 0.5% prior.

- PPI Y/Y 3.8% vs. 3.9% prior.

The US PCE came in line with forecasts:

- PCE Y/Y 3.4% vs. 3.4% expected and 3.4% prior (revised from 3.5%).

- PCE M/M 0.4% vs. 0.3% expected and 0.4% prior.

- Core PCE Y/Y 3.7% vs. 3.7% expected and 3.8% prior (revised from 3.9%).

- Core PCE M/M 0.3% vs. 0.3% expected and 0.1% prior.

Consumer spending and income for September:

- Personal income 0.3% vs. 0.4% expected and 0.4% prior.

- Personal spending 0.7% vs. 0.5% expected and 0.4% prior.

- Real personal spending 0.4% vs. 0.1% prior.

The highlights for next week will be:

- Monday: Australia Retail Sales.

- Tuesday: Japan Jobs data, Japan Retail Sales and Industrial Production, Chinese PMI, BoJ Policy Decision, Swiss Retail Sales, Eurozone GDP and CPI, Canada GDP, US ECI, US Consumer Confidence, New Zealand Jobs data.

- Wednesday: Chinese Caixin Manufacturing PMI, US ADP, Canada Manufacturing PMI, US ISM Manufacturing PMI, US Job Openings, FOMC Policy Decision.

- Thursday: Swiss CPI, US Challenger Job Cuts, BoE Policy Decision, US Jobless Claims.

- Friday: Chinese Caixin Services PMI, Eurozone Unemployment Rate, Canada Jobs data, US NFP, US ISM Services PMI.

That’s all folks. Have a great weekend.