Monday:

China CPI missed expectations coming at 0.0% vs. 0.2% expected for the Y/Y reading and -0.2% vs. 0.0% expected for the M/M figure. Moreover, the PPI Y/Y came at -5.0% vs. -4.6% expected. These figures signal that China is sliding into deflation, and we should see stronger easing measures being adopted soon.

Fed’s Barr (hawk - voter) said that inflation is far too high and that they are attentive to bring inflation down to target. He acknowledged that they made a lot of progress on inflation and that they are close (to the end of the hiking cycle) but they still have a bit of work to do.

The NY Fed 1-year ahead inflation expectations eased to 3.8% vs. 4.1% previously, which is the lowest since April 2021. The bad news is that the 3-year ahead expected inflation remained unchanged at 3% and the 5-year expected inflation jumped to 3% vs. 2.7% previously.

Fed’ Mester (hawk – non voter) said that the Fed will need to tighten somewhat further to lower inflation as its policy is less restrictive compared to history. She continued saying that raising rates again will reduce the risk of more action in the future. She acknowledged that the rate hikes have been moderating the economic activity, but the economy proved stronger than expected. She also said that the Fed is closed to the end of its tightening campaign. She added that the gains in core inflation are too high and broad-based, and wages pressures remain too high to get inflation back to 2% target. She concluded that there’s no decision yet on the need for a July rate hike as more data is needed.

Fed’s Daly (hawk – non voter) said that the US economic momentum continues to surprise and therefore there’s more that they need to do with rate hikes. She added that they are data dependent but sees the need for two more rate hikes this year to lower high inflation amidst a robust labour market. She acknowledged that the precise number of rate hikes may be adjusted based on the economic data and more or fewer hikes may be needed. She concluded that the Fed should increase rates more slowly than last year to evaluate the economy’s response but thinks that the risk of underacting continues to outweigh the risk of overacting despite these risks being more balanced now.

BoE’s Bailey (hawk) said that UK inflation is unacceptably high, but it’s expected to decrease significantly. He acknowledged that both price and wage increases at current rate are inconsistent with the inflation target. He added that the MPC is monitoring developments in the labour market, wage growth and services price inflation.

Fed’s Bostic (dove – non voter) said that inflation is too high and not sustainable and that a lot of the strength is due to pandemic support. He added that the trajectory on inflation right now is in the right direction and the Fed will ensure that it continues. A recession is not his baseline outlook, but the biggest risk is not moving inflation back to target. He continued with saying that the policy is clearly in restrictive territory right now and the Fed can be patient as the economy is starting to slow down with job growth slowing and inflation coming down. He concluded that there is no expectation of needing to raise rates any further from here and that even with a 25 bps move at the next meeting, it will still require patience.

Tuesday:

The UK payrolls missed expectations coming at 102K vs. 125K expected and 250K prior. The unemployment rate has also increased to 4.0% vs. 3.8% expected and the 3.8% prior. The worst part of the report for the BoE were the wages data that surprised again to the upside. In fact, the average weekly earnings came at 6.9% vs. 6.8% expected and 6.5% prior (revised to 6.7%). The average weekly earnings ex-bonus printed at 7.3% vs. 7.1% expected and 7.2% prior (revised to 7.3%). The market started to price in a higher chance of a 50 bps hike from the BoE after the release.

ECB’s Villeroy (hawk) said that they are close to the peak in interest rates and once they hit the peak, they will need to stay at that level for a while. He acknowledged that they are starting to see good news on inflation, and it’s expected that it will continue to decline and be back to 2% by 2025.

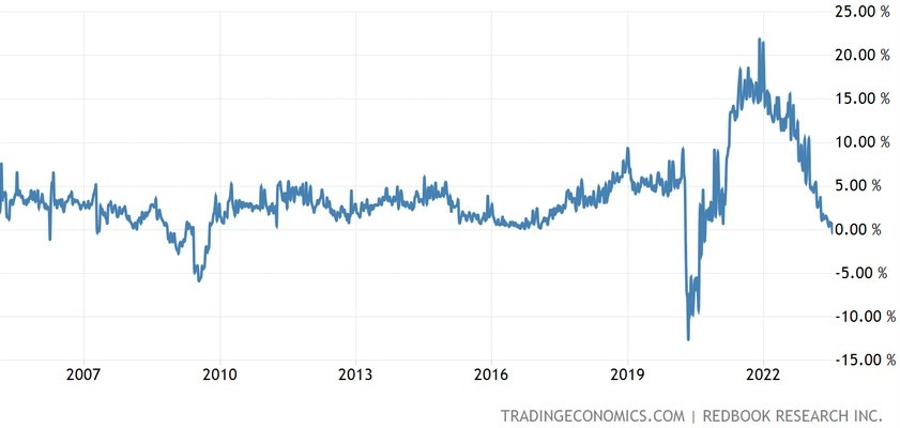

The US Redbook Y/Y got some attention as the index fell -0.4% vs. 0.7% last week and this was the first negative reading since the start of the pandemic.

Wednesday:

The RBNZ left its cash rate unchanged at 5.50% as widely expected. Below the key passages from the statement:

- The level of interest rates are constraining spending and inflation pressure as anticipated and required.

- The Committee agreed that the OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1 to 3% annual target range, while supporting maximum sustainable employment.

- Global economic growth remains weak and inflation pressures are easing.

- Global inflation rates continue to decline, assisted by the normalisation of international supply chains, and the decline in shipping costs and energy prices.

- The weaker global growth has led to lower export prices for New Zealand's goods.

- In New Zealand, inflation is expected to continue to decline from its peak, and with it measures of inflation expectations. Core inflation is expected to decline as capacity constraints ease.

- While employment is above its maximum sustainable level, there are signs of labour market pressures dissipating and vacancies declining.

- The Committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment.

RBA’s Governor Lowe said that it’s possible there will be more rate hikes still to come to return inflation back to target. He acknowledged that it remains to be determined whether monetary policy has more work to do as the picture on inflation is complex and there are significant uncertainties regarding outlook. He added that he’s very conscious that monetary policy operates with lag and the full effects are yet to be felt. He concluded that he’s “deadly serious” about getting inflation back to target and that he’s confident that higher interest rates are working.

The US CPI missed expectations across the board with the Y/Y figure coming at 3.0% (2.97% unrounded) vs. 3.1% expected and 4.0% prior. The M/M reading printed at 0.2% vs. 0.3% expected and 0.1% prior. The even better news is that Core Inflation figures have also missed expectations with the Y/Y rate coming at 4.8% vs. 5.0% expected and 5.3% prior, and the M/M figure printing at 0.2% (0.158% unrounded) vs. 0.3% expected and 0.4% prior.

Fed’s Barkin (hawk – non voter) was the first one to speak after the CPI release and he didn’t hint to any skip or pause at the July meeting, instead he said that inflation remains too high and there’s still a question whether inflation can settle while labour market remains as strong as it is. He concluded that he’s comfortable doing more with policy if incoming data does not confirm that inflation will return to target.

Fed’s Kashkari (hawk – voter) said that if high inflation persists, they may need to raise rates further. He added that the fight against inflation must succeed but acknowledged that higher rates could increase pressure on banks and that’s why bank supervisors should ensure that all banks are prepared to withstand higher rate environment.

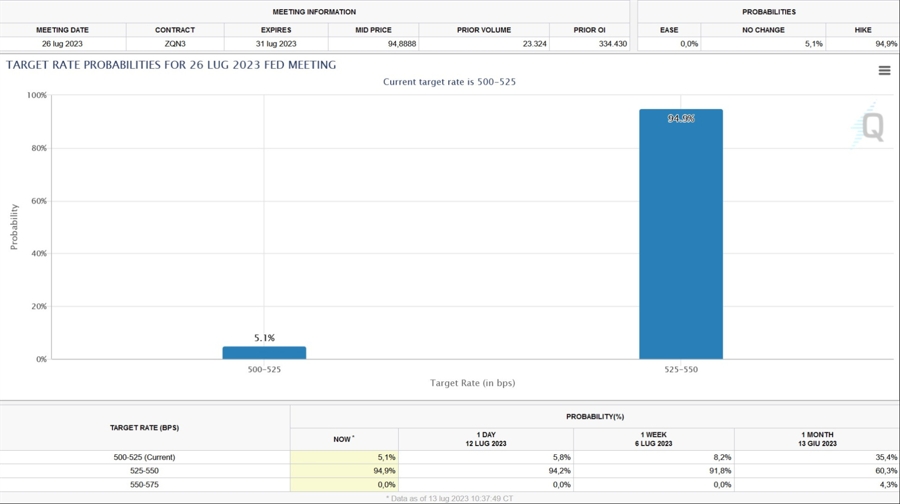

Given the tightness in the labour market and the lack of hints to a possible skip or pause from the Fed members, the market still expects the FOMC to hike by 25 bps at the July meeting. Notably, the “Fed whisperer” Nick Timiraos has also published an article after the CPI release stating that this report is unlikely to change the Fed’s course on a 25 bps hike at the upcoming meeting. Nevertheless, the chances of rate increases after the July meeting plunged.

ECB’s Vujcic (hawk – voter) said that the September ECB meeting is very open. He acknowledged that China is a risk to GDP outlook and that slowing down the pace of rate hikes is certainly a possibility. He concluded that even if they pause, they will still say that they can resume hiking.

ECB’s Lane (dove – voter) said that the typical length and monetary transmission mean that full economic impact of the tightening over the last year will only play out over the next couple of years.

The BoC raised interest rates by 25 bps to 5.0% as expected. The key lines from the statement below:

- Robust demand and tight labour markets are causing persistent inflationary pressures in services.

- Canada’s economy has been stronger than expected, with more momentum in demand.

- While the Bank expects consumer spending to slow in response to the cumulative increase in interest rates, recent retail trade and other data suggest more persistent excess demand in the economy.

- The housing market has seen some pickup. New construction and real estate listings are lagging demand, which is adding pressure to prices.

- In the labour market, there are signs of more availability of workers, but conditions remain tight, and wage growth has been around 4-5%. Strong population growth from immigration is adding both demand and supply to the economy: newcomers are helping to ease the shortage of workers while also boosting consumer spending and adding to demand for housing.

- As higher interest rates continue to work their way through the economy, the Bank expects economic growth to slow.

- While CPI inflation has come down largely as expected so far this year, the downward momentum has come more from lower energy prices, and less from easing underlying inflation. With the large price increases of last year out of the annual data, there will be less near-term downward momentum in CPI inflation.

- Moreover, with three-month rates of core inflation running around 3½-4% since last September, underlying price pressures appear to be more persistent than anticipated. This is reinforced by the Bank’s business surveys, which find businesses are still increasing their prices more frequently than normal.

- Governing Council remains concerned that progress towards the 2% target could stall, jeopardizing the return to price stability.

- Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation. In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the 2% inflation target.

BoC’s Governor Macklem said that they are concerned that if they are not careful, the progress to price stability could stall and if they get some upward surprises, inflation could even move back higher. He added that there was not a big benefit of waiting to raise rates, but they did discuss the possibility of keeping rates unchanged. The monetary policy is working but underlying inflationary pressures are proving more stubborn while the labour market remains tight, even if there are some signs of easing. He said that the Bank of Canada is prepared to raise rates further as if they don’t do enough now, they will likely have to do even more later.

Thursday:

The New Zealand Manufacturing PMI for June came at 47.5 vs. 48.9 previously. For a weaker reading one has to go back to August 2021 (39.0) when the Delta strain outbreak of COVID-19 invoked level-4 lockdowns.

The UK May monthly GDP came at -0.1% vs. -0.3% expected and 0.2% prior.

ECB’s Visco (dove – non voter) said that they are not very far from the peak in interest rates and that he somewhat disagrees with the preference for further tightening.

The ECB released the accounts of its June monetary policy meeting. Below the key lines:

· Members considered that there were both upside and downside risks to the inflation outlook.

· It was argued that market participants would be surprised by the upward revision of inflation.

· This could trigger a repricing of the forward curve.

· Members broadly concurred that inflation was still projected to remain too high for too long.

· It was argued that policymakers should not put too much emphasis on the behaviour of core inflation, as its mandate related to headline inflation.

· Maintaining a gradual tightening path would allow the ECB to monitor and assess the impact of past monetary policy decisions and ensure that financial conditions were adjusting in a way that was consistent with inflation moving back to the 2% medium-term target.

· Members generally agreed that the data-dependent approach to monetary policymaking.

· Policymakers should stress that fiscal policy needed to be tightened in order to dampen demand and support the disinflation process.

The US PPI missed expectations across the board with the Y/Y figure coming at 0.1% vs. 0.4% expected and 1.1% prior, while the M/M reading printed at 0.1% vs. 0.2% expected and -0.4% prior (revised from -0.3%). The Core PPI Y/Y figure came at 2.4% vs. 2.6% expected and 2.6% prior (revised from 2.8%), while the M/M reading printed at 0.1% vs. 0.2% expected and 0.1% prior (revised from 0.2%).

The US Initial Claims beat expectations coming at 237K vs. 250K expected and 249K prior. On the other hand, Continuing Claims missed expectations coming at 1729K vs. 1723K expected and 1718K prior.

Fed’s Daly (hawk – non voter) said that the good news on inflation this week is indeed good news. She acknowledged that saying that they needed 2 more rate hikes was a way to keep optionality open but it’s too early to say that we can declare victory on inflation. She continued saying that the lags in monetary policy are generally between 12 and 24 months and that there are still cumulative effects of monetary tightening that will work its way through the system. She added that they are going to continue to work on rate hikes until they are sure that inflation is on the path to come back down toward the 2% target. She acknowledged that if they wait for inflation to be 2% and have monetary lags, it’s better to head to a less restrictive policy to adjust for the last. In fact, as inflation starts coming down, they can start lowering the nominal rate to bring real rates down to neutral levels. She concluded that they are not there yet and the skip at the June meeting was because as they reach their destination, they want to slow the pace of hikes.

Friday:

Fed’s Waller (hawk – voter) said that he’s in favour of raising interest rates at the July FOMC meeting as he’s increasingly confident that the banking stress won’t derail the economy and that the cooler CPI data is welcome, but they need to see if it’s sustained given that inflation has shown false dawns before. He added that although the job market has slowed, it remains very strong and that coupled with the economic strength gives the Fed space to hike further. He still thinks that the Fed will likely need two more 25 bps hikes this year as the monetary policy changes are moving through the economy more quickly and the bulk of past rates hikes have already impacted the economy. He concluded that fighting inflation remains the Fed’s main goal and that they will succeed.

The Japanese media reported that the BoJ is likely to raise its FY2023 inflation forecast above 2%. They previously expected inflation falling down from September/October, but now they are not confident on such a scenario anymore. This might be another signal that a change in policy like a tweak to the YCC might be coming. Another possible hint came from the former BoJ director Hayakawa as he said that he expects the BoJ to tweak YCC at the July meeting (27-28th July) widening the target band to -/+ 1.00% from the current -/+ 0.50%.

Fed’s Goolsbee (dove – voter) said that there’s a way to curb inflation without a recession and that weaker inflation data shows that the Fed is making progress.

The University of Michigan Consumer Sentiment for July jumped to 72.6 vs. 65.5 expected and 64.4 prior. The Current Conditions index printed at 77.5 vs. 70.4 expected and 69.0 prior, while the Expectations index came at 69.4 vs. 61.8 expected and 61.5 prior. The 1-year inflation expectations ticked higher to 3.4% vs. 3.3% prior and the 5-year inflation expectations printed at 3.1% vs. 3.0% prior.That's a really strong release.

The highlights for next week include:

- Tuesday: US Retail Sales, Canada CPI.

- Wednesday: NZ CPI, UK CPI.

- Thursday: PBoC LPR, Australia Jobs Report, US Jobless Claims.

- Friday: Japan CPI.

That’s all folks, have a great weekend!