- Prior was -10

- Services +9 vs -8 prior

- Manufacturing shipments -2 vs -13 prior

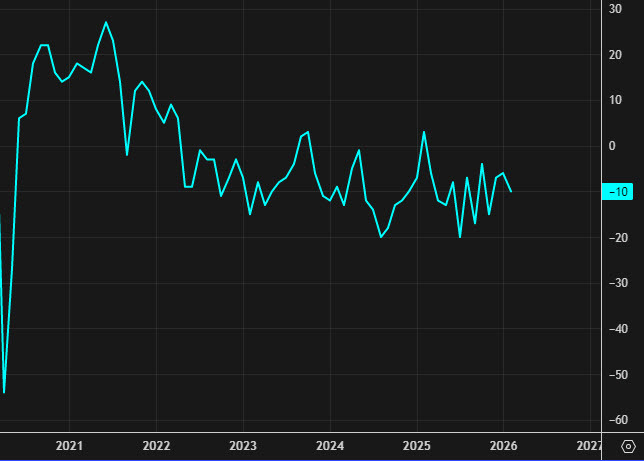

This is a nice bounce and the zero reading on the headline is the best since February 2025.

Current Conditions:

Shipments: -2 vs -13 prior

New Orders: +4 vs -9 prior

Employment: -2 vs -7 prior

Backlog of Orders: -10 vs -14 prior

Capacity Utilization: -5 vs -12 prior

Vendor Lead Time: +13 vs -1 prior

Local Business Conditions: -5 vs -15 prior

Capital Expenditures: -6 vs -5 prior

Finished Goods Inventories: +5 vs +7 prior

Raw Materials Inventories: +4 vs +11 prior

Equipment & Software Spending: -8 vs -8 prior

Services Expenditures: -14 vs -20 prior

Wages: +14 vs +18 prior

Availability of Skills Needed: -12 vs -15 prior

Price Trends (12-month % change):

Prices Paid: 6.11% vs 6.52% prior

Prices Received: 4.85% vs 4.25% prior

New orders flipped positive for the first time in recent months. Vendor lead times surged, suggesting potential supply-side tightening. Services spending remains deeply negative. Firms still expect price growth to moderate over the next 12 months, though prices received accelerated in March.