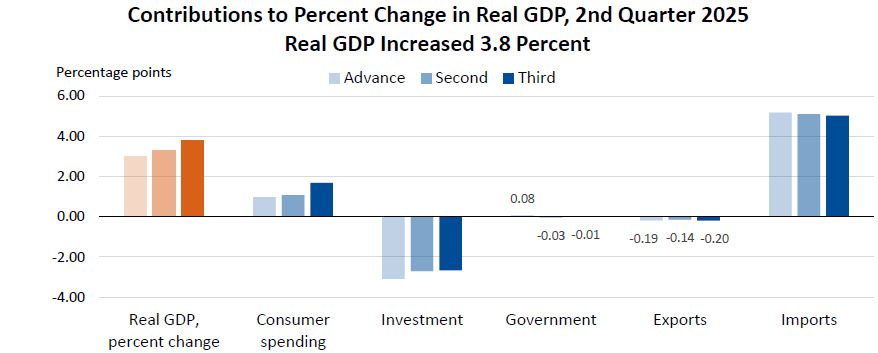

- Second reading was +3.3%

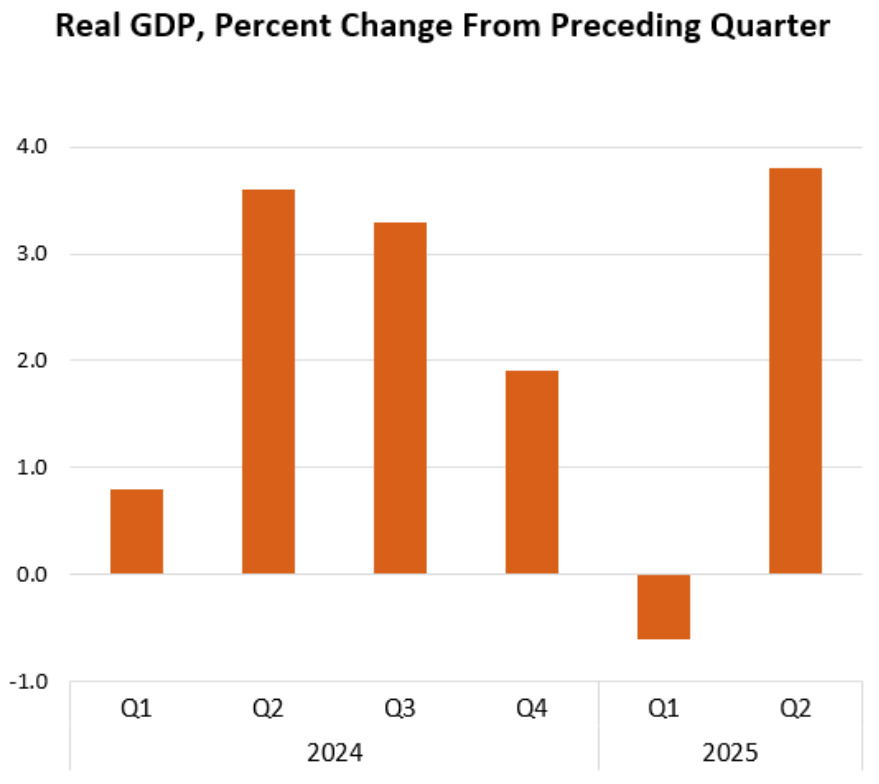

- Final Q1 was -0.5%

- GDP final sales +7.5% vs 6.8% second reading

- Consumer spending final +2.5% vs +1.6% second reading

- Core PCE final +2.6% vs +2.5% second reading

- Full report

This is an impressive revision led by a much-more impressive consumer.

Digging through the data, there is still a big impact on the whipsaw effect from tariffs but looking ahead, there is some more good news as the August goods trade balance number was better than anticipated.