- Prior was +2.9%

- PCE M/M +0.3% vs +0.3% expected

- Prior +0.4%

- Core PCE Y/Y +2.8% vs +3.1% expected

- Prior +3.0%

- Core PCE M/M +0.4% vs +0.4% expected

- Prior +0.4%

Consumer spending and income for January:

- Personal income +0.4% vs +0.5% expected

- Prior +0.3%

- Personal spending 0.4% vs +0.4% expected

- Prior +0.3%

- Real personal spending +0.1% vs +0.1% prior

This is a problematic report for the Federal Reserve doves. The numbers were mostly in-line with expectations but if you zoom in, that's back-to-back months of +0.4% core PCE. You don't need too many more months like that to get to 2% inflation and those numbers will stay in the y/y calculation for the next 10 months. In addition, the energy price shock is coming.

For some background, the Personal Income and Outlays report, published monthly by the Bureau of Economic Analysis, includes the Personal Consumption Expenditures price index — the Federal Reserve's preferred measure of inflation. Unlike the CPI, which uses a fixed basket, the PCE index accounts for changes in consumer behavior through a chain-weighted methodology, giving it a broader and more adaptive scope.

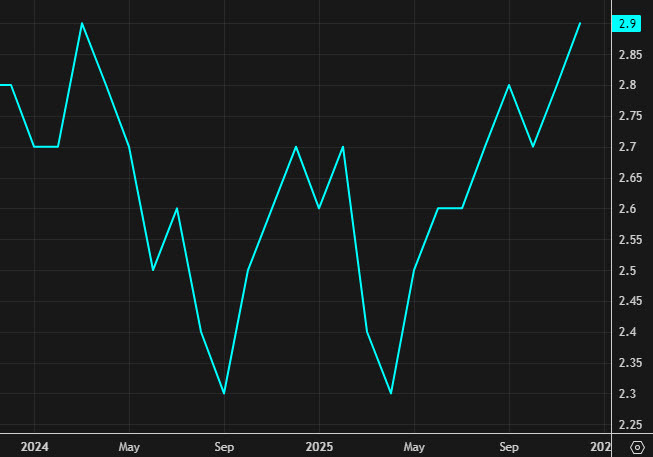

In December 2025, the headline PCE price index rose 0.4 percent month over month, an acceleration from 0.2 percent gains in both October and November. On a year-over-year basis, headline PCE climbed to 2.9 percent, up from 2.8 percent in November and continuing a gradual upward drift from the 2.5–2.7 percent range that prevailed through mid-2025. Core PCE, which strips out food and energy, also rose 0.4 percent on the month and reached 3.0 percent year over year — its highest reading since February 2025 and a notable step up from the 2.8 percent pace that had held relatively steady for several months.

On the spending side, nominal PCE increased 0.4 percent, but after adjusting for inflation, real spending grew just 0.1 percent, a deceleration from November. Services spending drove the gains while goods spending contracted in real terms. Personal income rose 0.3 percent, though real disposable income was essentially flat. The personal saving rate slipped to 3.6 percent, its lowest since October 2022 and down from 4.9 percent as recently as May, suggesting consumers were increasingly drawing down savings to sustain spending.

The December report was released on February 20, delayed from its original late-January date due to the government shutdown. The uptick in core PCE reinforced expectations that the Fed would hold rates steady in the near term, with markets attentive to whether the reversal of the disinflationary trend would persist into 2026.