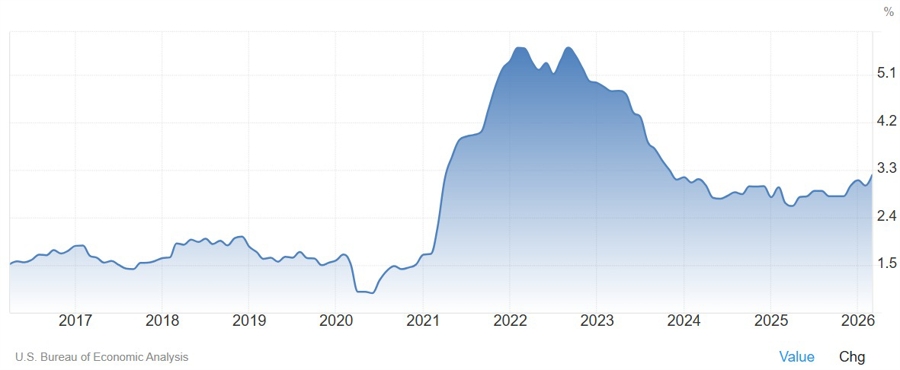

Core PCE (excluding food & energy):

- Core y/y +3.2% vs +3.2% expected

- Prior was +3.0%

- Core m/m +0.3% vs +0.3% exp

- Prior +0.4%

Consumer spending and income for February:

- Personal income +0.6% vs +0.3% expected. Prior month -0.1% (revised to 0.0%)

- Personal spending +0.9% vs +0.9% expected. Prior month +0.5% (revised to +0.6%)

- Real personal spending +0.2% vs +0.1% prior (revised to +0.3%)

The inflation figures are all as expected, so there's nothing to see there. With Core PCE now well above 3.0%, you can see why some FOMC policymakers wanted to drop the easing bias.

The Fed has been missing its 2% target since 2021 and the reluctance to adopt a clear hawkish bias kept the market in a dovish reaction function. Financial conditions never really tightened enough to bring inflation sustainably back to target. Inflation continues to run around 3% and the US-Iran war is expected to add more upward pressure.

We also got the US jobless claims data at the same time and well, they are pointing to a reacceleration in the labour market. The US Employment Cost Index for Q1 has also surprised to the upside coming in at 0.9% vs 0.7% in the prior quarter.

Following all the data release, US interest rate futures slightly increased odds of a rate hike by the end of 2026.