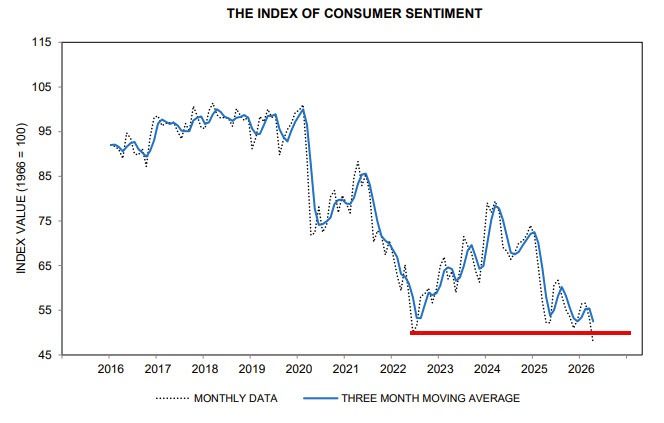

- Prior month 53.3

- Consumer Sentiment 47.6 vs 52.0 estimate. Worst on record. Year on year -8.8%

- Current conditions 50.1 versus 55.8 last month.Year on year -16.2%

- Expectations and 46.1 versus 51.7 last month. Year on Year -2.5%

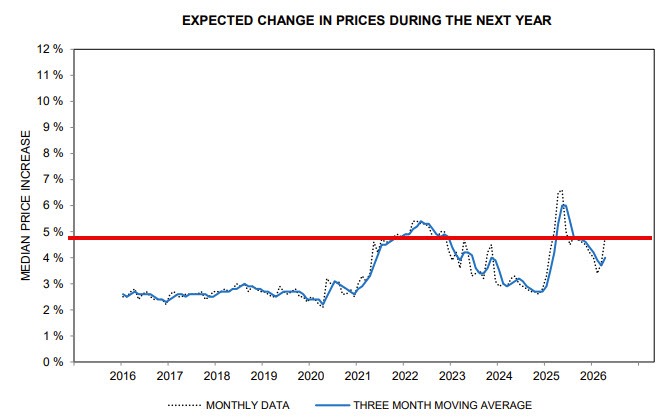

- 1 year inflation expectations 4.8% versus 3.8% last month

- 5 year inflation expectations 3.4% versus 3.2% last month

Needless to say, the war in Iran is having its impact on the survey data. The data is the worst on record.

When you go to war. When gas prices spike higher ($4.15 is the National average now - from $2.89 before the war). When the end to the war is unknown, the consumer sentiment suffers.Inflation is simply too high and going higher. 2% target is now a long way away and with it, go hopes even for a Warsh cut when he takes over the Fed.

Having said that, survey data can be very fickle and move around. Nevertheless, the confidence decline is real, and people know it by going to the gas pump. If this price at the pump is to go back down, it will be "happy days again", but until then the consumer will worry.

If there is any bright spot, the 5 year inflation expectation only moved up to 3.4% from 3.2%. The 1-year inflation expectation was not so good with a 1% jump to 4.8%.

Comments from Director Joanne Hsu:

Consumer sentiment sank about 11% this month, extending a decline that began with the start of the Iran conflict, and is currently about 9% below a year ago. Demographic groups across age, income, and political party all posted setbacks in sentiment, as did every component of the index, reflecting the widespread nature of this month’s fall. One-year expected business conditions plunged about 20% and is now 6% below last April. Assessments of personal finances declined about 11%, with consumers expressing a substantial increase in concerns over high prices and weaker asset values. Buying conditions for durables and vehicles worsened, again on the basis of high prices. Open ended comments show that many consumers blame the Iran conflict for unfavorable changes to the economy. Note that 98% of interviews were completed prior to the April 7th announcement of a temporary cease-fire. Economic expectations will likely improve after consumers gain confidence that the supply disruptions stemming from the Iran conflict have ended and gas prices have moderated.

Year-ahead inflation expectations surged from 3.8% in March to 4.8% this month, the largest one-month increase since April 2025 (see chart, black dashed line and black circle). The current reading exceeds those seen in 2024 and remains well above the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations ticked up from 3.2% last month to 3.4% this month, the highest reading since November 2025. In 2024, values ranged between 2.8% and 3.2%, while in 2019 and 2020, they were consistently below 2.8%.