The Always awesome Europe Market Open from the lads at Newsquawk

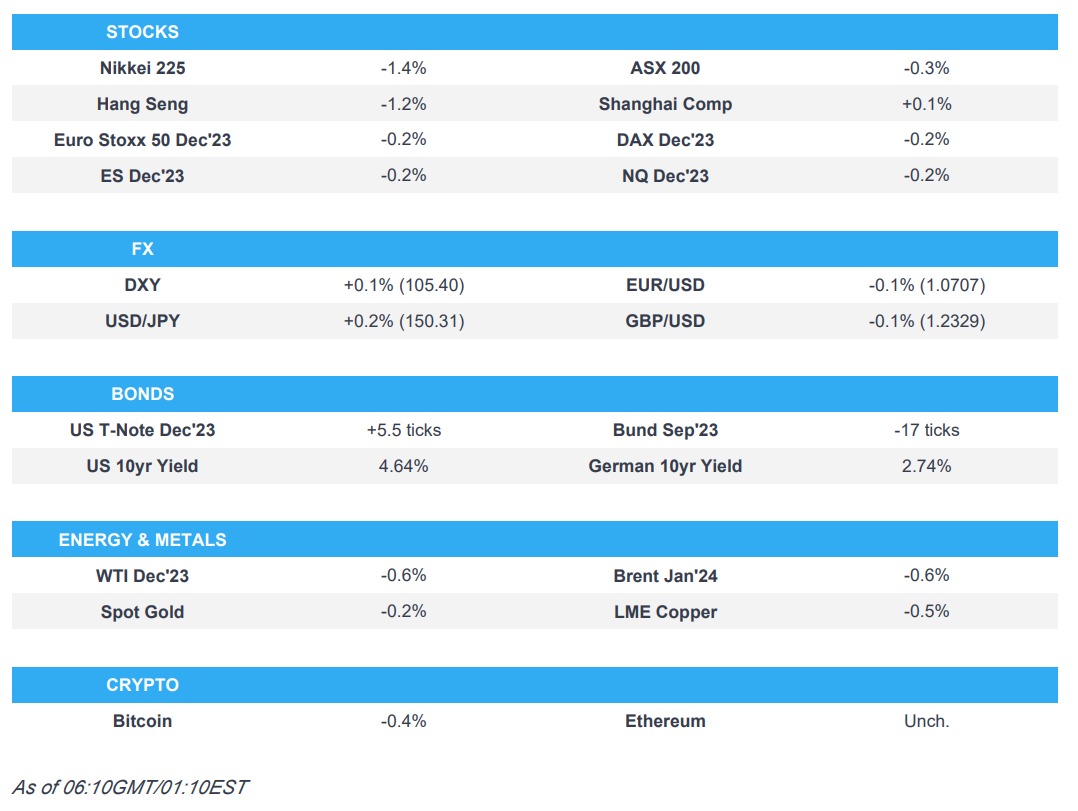

- APAC stocks were softer across the board following the prior day’s gains and the choppy/mixed lead from Wall Street.

- DXY gradually inched higher towards the top end of a 105.25-42 APAC range with G10s softer against the Buck to varying degrees.

- RBA hiked its Cash Rate by 25bps as expected to 4.35% from 4.10%, while forward guidance saw a dovish tweak.

- European equity futures are indicative of a softer open with the Eurostoxx 50 -0.3% after cash markets closed -0.4% yesterday.

- Israeli PM Netanyahu says Israel is open to "short pauses" in Gaza, but ruled out a ceasefire.

- Looking ahead, highlights include EZ, German, French & Italian Construction PMI, US International Trade, IBD/TIPP, Manheim Index, NY Fed Q3 Household Debt & Credit Report, UK King's Speech, Speeches from ECB’s de Guindos; Fed’s Schmid, Williams, Logan, Barr & Waller, supply from UK.

- Earnings: Capgemini, CNH Industrial, Daimler Truck, Persimmon, Watches of Switzerland, UBS, eBay, Occidental Petroleum Corp, Datadog.