- Feb final services was 51.0

- Manufacturing 49.8 vs 51.7 expected

- Prior manufacturing was 52.7

- Composite PMI 53.5 vs 51.6 prior

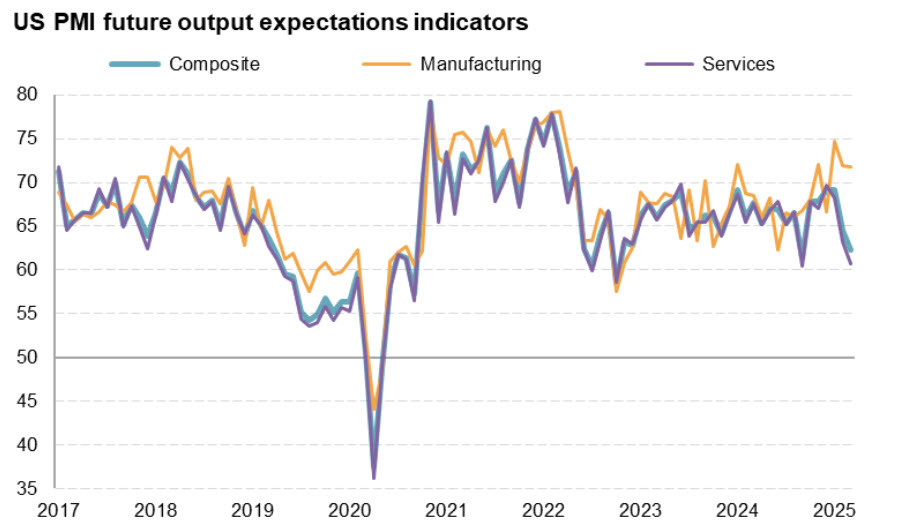

- Services optimism about the coming year fell for a second successive month, and is at the second lowest since Oct 2022

- Factory optimism remained high

- Employment rose slightly in April

- Input costs increased at the sharpest rate for 23 months

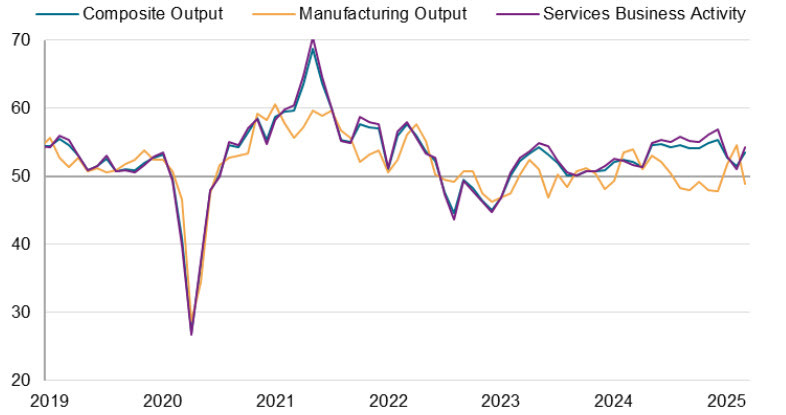

The services PMI peaked near 57 after the election but it's has trended lower since the tariff talk ramped up. This month, we got a nice rebound on the services side but manufacturing fell below the 50 level. Overall, the services side is a much more important component of the US economy so I take this as good news. That said, S&P says this number isn't exactly pointing to gangbusters growth.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence"

“A welcome upturn in service sector activity in March has helped propel stronger economic growth at the end of the first quarter. However, the survey data are indicative of the economy growing at an annualized 1.9% rate in March and just 1.5% over the quarter as a whole, pointing to a slowing of GDP growth compared to the end of 2024.

"Near-term risks also seem tilted to the downside. Growth is concentrated in the service sector as manufacturing fell back into decline after the front- running of tariffs had temporarily boosted factory output in the first two months of the year. Similarly, some of the March upturn in services was reportedly due to business picking up after adverse weather conditions had dampened activity across many states in January and February, which could prove a temporary bounce.

"Business confidence in the outlook has also darkened, souring further from the buoyant mood seen at the start of the year to one of the gloomiest readings seen over the past three years, largely caused by growing worries over negative impacts from recent policy initiatives from the new administration. Most widely cited were concerns about the impact of Federal spending cuts and tariffs.

"A key concern over tariffs is the impact on inflation, with the March survey indicating a further sharp rise in costs as suppliers pass tariff-related price hikes on to US companies. Firms' costs are now rising at the steepest rate for nearly two years, with factories increasingly passing these higher costs onto customers. Thankfully, from the Federal Reserve’s perspective, services inflation remains relatively subdued, but this reflects the need to keep prices low amid weak demand, which will harm profits."

More to come