- Prior was -5

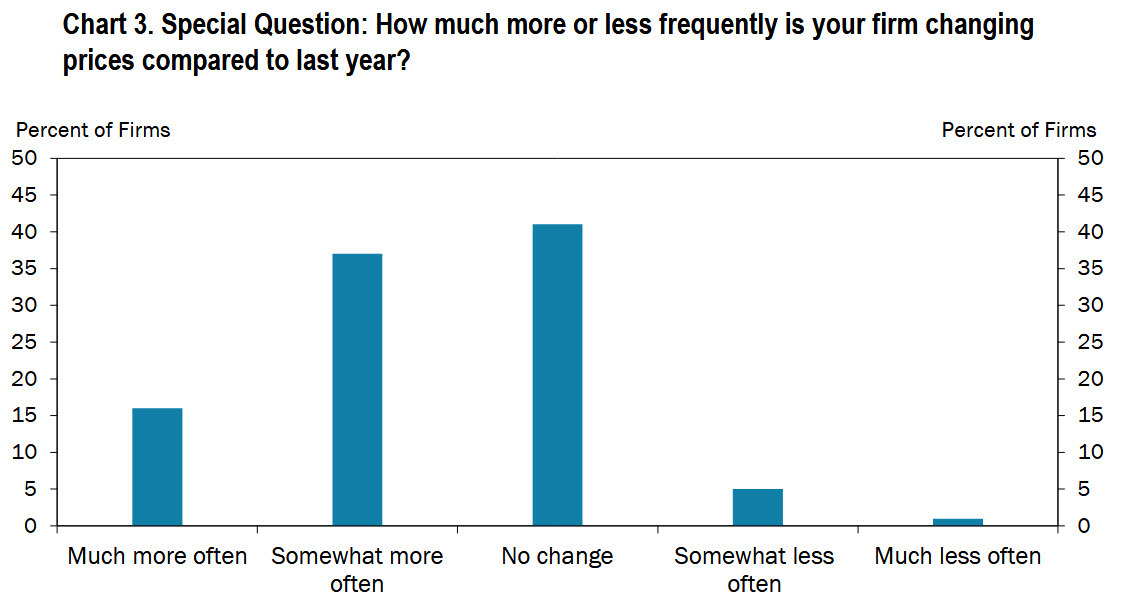

- About half of firms (52%) reported their hiring plans for the remainder of 2025 have not changed since the beginning of the year, while 34% expect them to decrease and 14% expect to increase hiring plans

- Prices paid +34 vs +42 prior

- Prices received +17 vs +29 prior

- Composite index -3 vs -4 prior

- New orders for exports -21 vs -10 prior

This has bounced around but it's above the -13 low in February. The pricing indexes improved from extreme levels in a sign that tariff angst has peaked.

Comments in the survey:

- “Current business volume not sustainable long-term.”

- “Some inventory we are reducing considerably due to significantly lower sales. Some inventory is quite a bit higher due to opportunity buys.”

- “Our business is in the biggest supply shortage in history. Demand is excellent at the moment, not sure how long that lasts given the shortages our customers are experiencing.”

- “Year started strong but seems to be tapering off for at least the near term.”

- “Domestic conditions are better, but still much potential for volatility.”

- “Lots of uncertainty about landed costs of raw materials and capital expenditures. We will adjust who we buy from and what we charge our customers based on current situation, not future speculation.”

- “Trade policy continues to impact business. The constant uncertainty around overall policy is negative for consumers and for us.”

- “We are insourcing equipment builds which will drive growth and allow for us to purchase capex manufacturing equipment and hire three more employees.”