- Barclays flags strongest stock buy signal in a year as sentiment resets

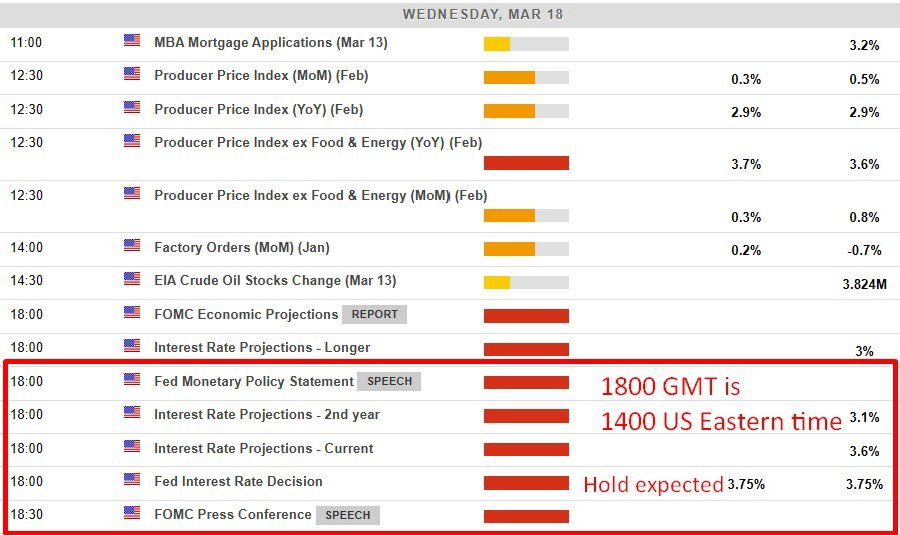

- Fed set to hold as Deutsche Bank flags geopolitics clouding outlook

- China approves Nvidia H200 AI chip sales as licences granted to multiple firms

- China firms ramp up FX hedging as yuan strength threatens export earnings

- PBOC sets USD/ CNY mid-point today at 6.8909 (vs. estimate at 6.8798)

- India is working with Iran to secure safe passage for key fuel shipments through Hormuz,

- Projectile strikes near Iran’s Bushehr nuclear plant, no damage reported

- Japan exports beat forecasts but lose momentum from prior surge

- Australia leading index steady. Growth outlook softens to below trend on rate hikes & war

- Japan firms set for strong wage hikes as labour shortages persist, outlook uncertain

- Japan manufacturers sentiment hits four-year high, but outlook dims on Middle East risks

- Iraq, KRG agree to resume Ceyhan oil exports as Hormuz disruption tightens supply

- RBA hikes to 4.10%. Split decision. Inflation risks & demand pressures. Where to now?

- Recap: RBA lifts rate to 4.1%. Split decision. Inflation risks & capacity pressures build

- Private survey inventory shows a huge headline crude oil build much larger than expected

- US weighs easing Venezuela oil sanctions to boost supply amid global disruptions

- US major indices close higher for the 2nd consecutive day. Gains led by small-cap stocks.

- investingLive Americas market news wrap: A divergence appears between oil and stocks

At a glance:

Iran launches retaliatory strikes after Larijani killing

Oil slips despite tensions, no fresh escalation signals

Iraq and the Kurdistan Regional Government agreed to resume Ceyhan oil exports

Mixed US inventory data: crude build, gasoline draw

Japan exports slow; US auto shipments and China demand weaken

Japan–US to announce ¥11tn+ investment package

FX subdued ahead of Fed; BoJ decision due Thursday

Both Fed and BoJ expected to hold policy steady

China firms reportedly approved to buy Nvidia H200 chips

War-driven inflation risks rising, but growth headwinds building

Iran launched retaliatory strikes on Israel and US-linked assets following the killing of security chief Ali Larijani in an airstrike, though oil prices edged lower as markets saw no clear sign of further escalation or de-escalation. Price action was also weighed by mixed US private inventory data, with a larger-than-expected crude build offset by a deeper-than-forecast draw in gasoline. Official inventory data will follow on Wednesday morning US time. Iraq and the Kurdistan Regional Government agreed to resume Ceyhan oil exports.

In Japan, export growth slowed, reflecting weaker auto shipments to the US and softer demand from China amid Lunar New Year disruptions. Separately, Japan and the US are expected to unveil a joint statement outlining more than ¥11 trillion in additional investment commitments, marking a second tranche of economic cooperation.

Major FX pairs traded in subdued ranges ahead of today’s Federal Open Market Committee (FOMC) decision, with markets also looking ahead to the Bank of Japan policy announcement on Thursday (Japan time). Both central banks are widely expected to leave rates unchanged.

In tech, multiple Chinese firms were reportedly granted approval to purchase NVIDIA H200 AI chips, suggesting some easing at the margin in cross-border semiconductor flows.

Looking ahead, once the Fed decision passes, attention is likely to shift more fully to the economic implications of the Iran conflict. While the policy tone may lean hawkish with renewed emphasis on inflation risks, particularly via energy, there is a growing recognition that downside risks to employment and household income are also building.