- BLS preliminary annual jobs revision down by - 911K versus -682K estimate

- White House: Assured Qatar that a strike on their soil will not happen again

- US August NFIB small business optimism index 100.8 vs 101.0 expected

- U.S. Treasury sells $58 billion of the 3 year notes at a high yield of 3.485%

- Blackrock Reider: I think the Fed should cut by 50 basis points next week

- Qatar: Condemns the attack by Israel on Hamas delegation

- The BOJ has some officials tilting to a hike sending the USD/JPY lower

Markets:

- Gold down $5 to $3630

- US 10-year yields up 3.6 bps to 4.08%

- WTI crude oil up 50-cents to $62.76

- S&P 500 up 18 points to 6513

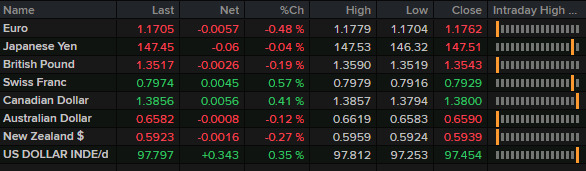

- JPY leads, CHF lags

The Bureau of Labor Statistics, showed that previous jobs reports through March were overstated by 911,000 jobs. It was the largest revision on record and cut the level of US employment by 0.6%.

The drop wasn't entirely unexpected as the economist consensus was 682K. Initially the US dollar dropped but evidently the market was braced for something even worse as the dollar quickly rebounded from the 20-pip blip on the headlines and continued steadily higher. Powell had warned at Jackson Hole that payrolls would be "revised down materially." The Fed rate path didn't reprice on news and the odds of a 50 bps cut next week actually slipped on the day.

Otherwise the market didn't have much to chew on. The US dollar steadily rose as Treasury yields ticked higher. Equities were bid into the close yet-again and the Nasdaq notched another record high.

In FX, the euro was under some pressure and that was tied back to French political drama but the euro did slightly outperform the Swiss franc.

Tomorrow we get US PPI and that will build towards Wednesday's CPI report.