- Prior 50.9

- Composite PMI 52.6 vs 52.6 prelim

- Prior 50.7

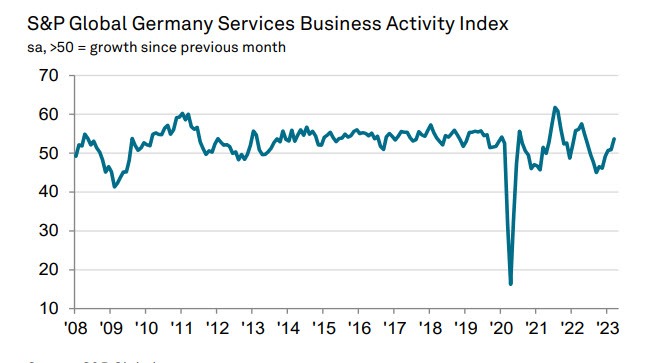

The headline reading is a 10-month high, even with the slight revision lower. This comes as demand strengthens and employment conditions also pick up towards the end of Q1. Cooler input costs and output charge inflation are also welcome developments, even if both remain elevated by historical standards. S&P Global notes that:

"Germany's service sector enjoyed a positive end to the opening quarter of the year, with the upturn in business activity gathering pace as demand continued to recover from the lull seen towards the end of last year.

"However, it remains to be seen if March's solid performance is enough to prevent the economy from entering a technical recession – as defined as back-toback quarterly contractions in GDP – given the carry over effects from the downturn in activity seen late last year. With business confidence stalling in March and manufacturing new orders still under pressure, modest economic growth is probably the best we can hope for in the next quarter.

"With the improvement in demand in March came a pick-up in hiring activity across the service sector, which will likely fuel concerns about wage pressures in the economy and the implications for inflation . Price increases in the service sector are easing, but even so the rate of inflation remained stubbornly high in March, pointing to persistently strong core price pressures and the potential for yet more interest rate rises."