- Prior 49.6

- Manufacturing PMI 50.2 vs 49.5 expected

- Prior 50.1

- Composite PMI 48.3 vs 49.3 expected

- Prior 49.9

It's not a good look for France's economy at the end of Q1 with business activity slumping to a five-month low. The services sector was the main drag, also seeing its weakest showing in five months as it falls further into contraction territory. While manufacturing activity was a two-month high, it belies the underlying performance of the sector with output falling to a four-month low.

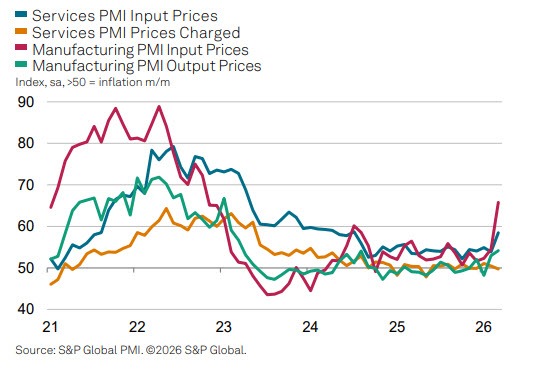

Amid higher energy prices, a key focus of the report is on prices. And we're already seeing evidence of the Middle East crisis having an impact with input cost inflation accelerating sharply to its strongest since November 2023. That in particular for the manufacturing sector. Trouble, trouble.

HCOB notes that:

"It's clear from March 'flash' PMI data that Europe's susceptibility to international supply-side disruption remains high. Soaring oil and oil-product prices, rising fuel costs and disrupted maritime supply chains have led to the worst delivery delays from vendors in over three years and pushed up input prices for French companies to an extent not witnessed since late-2023. We saw a very limited pass-through to selling prices, however, likely because prevailing demand conditions prior to the war in the Middle East were subdued. This dynamic could play a crucial role in determining how much of this supply shock filters through to the wider economy.

"March was further complicated by local elections, with firms reporting that clients held back on spending as a consequence. For that reason, April may give us a better indication of the true state of the economy, but for now, France's burgeoning recovery looks to be on ice. A sharp reduction in business confidence backs this assessment, with the threat of higher inflation, prolonged supply-side disruption and heightened near-term uncertainty prompting a re-evaluation of the outlook."