- Prior 48.4

- Composite PMI 49.9 vs 49.9 prelim

- Prior 49.1

No changes to the initial estimates as France's services sector registers a second successive month of falling business activity. The survey highlights that panelists attributed the decline in output to a mix of harsh weather conditions, project delays and elevated uncertainty.

In terms of price dynamics, France is arguably the only major economy in the region to see more benign inflation pressures. So, there's not much to comment on this front for the time being.

HCOB notes that:

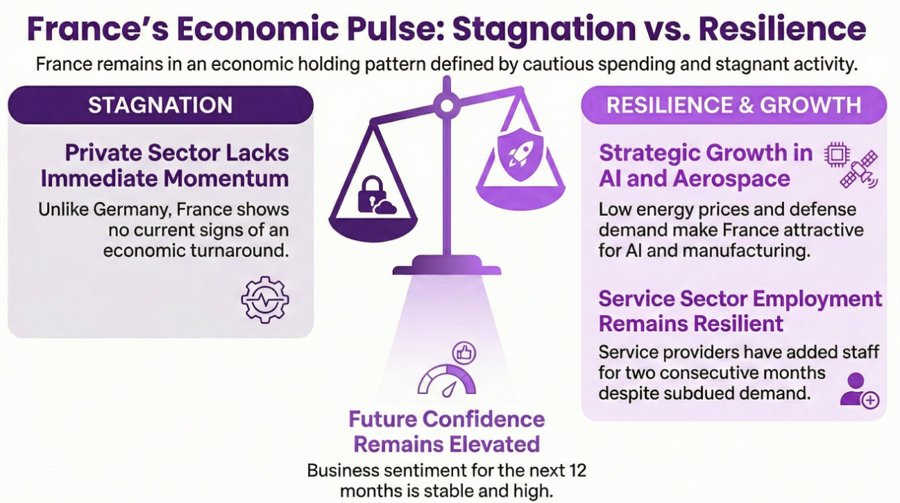

"France’s private sector is lacking momentum. Although the composite index has edged up slightly, the overall level remains far from encouraging. A comparison with Germany further illustrates this weakness, with the early stages of an economic turnaround there evident in the earlier-released flash PMI. No such shift is currently observable in France. Nonetheless, we still see potential for growth, with tailwinds in defence-related manufacturing like the aerospace sector, and France might be especially attractive for AI capex, given the comparative advantage in energy prices.

"Business activity in the service sector broadly stagnated in February. Many firms report persistent uncertainty, which delays investment decisions and weighs on new business. Demand remains subdued, reflecting customers’ cautious spending behaviour. This effect is exacerbated by declining foreign demand, with the corresponding sub-index below the 50.0 mark for seven consecutive months.

"On a more positive note, confidence regarding the service sector outlook for the next twelve months remains elevated. After surging in January, sentiment has stabilised at this higher level. This aligns with recent labour market developments, as service providers have added staff over the past two months. The fact that companies are hiring rather than cutting jobs highlights their cautious yet constructive approach to a potentially improving economic environment.

"Meanwhile, price dynamics in the French services sector appear benign. Input price inflation is below the long-term average, but interestingly, some firms reported higher hardware costs, which corresponds with recent indications of renewed semiconductor supply constraints. Output prices rose only marginally, reflecting attempts to pass higher costs on to customers."