- Prior 51.9

- Manufacturing PMI 51.4 vs 49.4 expected

- Prior 50.8

- Composite PMI 50.5 vs 51.0 expected

- Prior 51.9

The manufacturing sector is the only bright spot, with Germany leading the recovery in that regard. That being said, manufacturing output was softer than what the main index indicates with it being a two-month low. Meanwhile, the drag in the services sector pretty much brings overall business activity close to stalling with activity there being a ten-month low.

Looking at other details, employment conditions continue to struggle with it falling for a third month running. Staffing levels decreased in Germany and France, while the rest of the euro area posted the weakest rise in employment since November 2023.

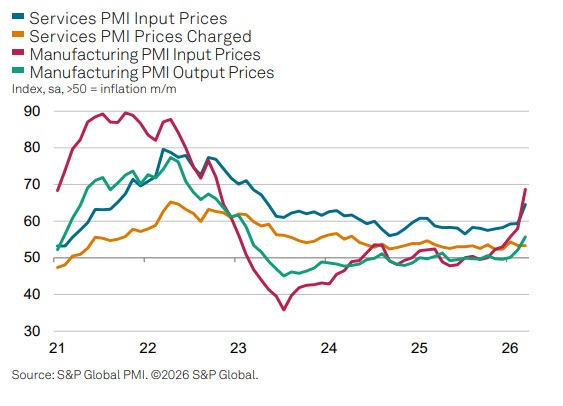

Besides that, prices were a key focus amid higher energy prices and we're already seeing clear signs of the US-Iran conflict leaving a mark. Of note, input prices increased at the fastest pace since February 2023 with steeper inflation registered across both the manufacturing and services sectors.

HCOB notes that:

“The flash Eurozone PMI is ringing stagflation alarm bells as the war in the Middle East drives prices sharply higher while stifling growth. Firms’ costs are rising at the fastest rate for over three years amid the surge in energy prices and choking of supply chains resulting from the war. Supplier delays have jumped to their highest since mid-2022, largely linked to shipping issues.

“Output growth has meanwhile slowed to nearstagnation thanks to a slump in business confidence and deterioration of new orders. The drop in future output expectations was the largest recorded since Russia’s invasion of Ukraine in 2022.

“The survey data are indicative of eurozone GDP growth slowing to a quarterly rate of just below 0.1% in March with the forward-looking indicators pointing to a heightened risk of a downturn the coming months. The survey’s price gauge is meanwhile indicative of consumer price inflation accelerating close to 3%, with cost pressure likely to add still further to selling price inflation in the coming months.

“The outlook depends on the duration of the war and any potential lasting impact on energy and supply chains, but the flash PMI data underscore how the European Central Bank is no longer in a “good place” with respect to growth and inflation, and will have to tread a cautious path with respect to policy in the face of a clear and rising risk of stagflation in the coming months.”