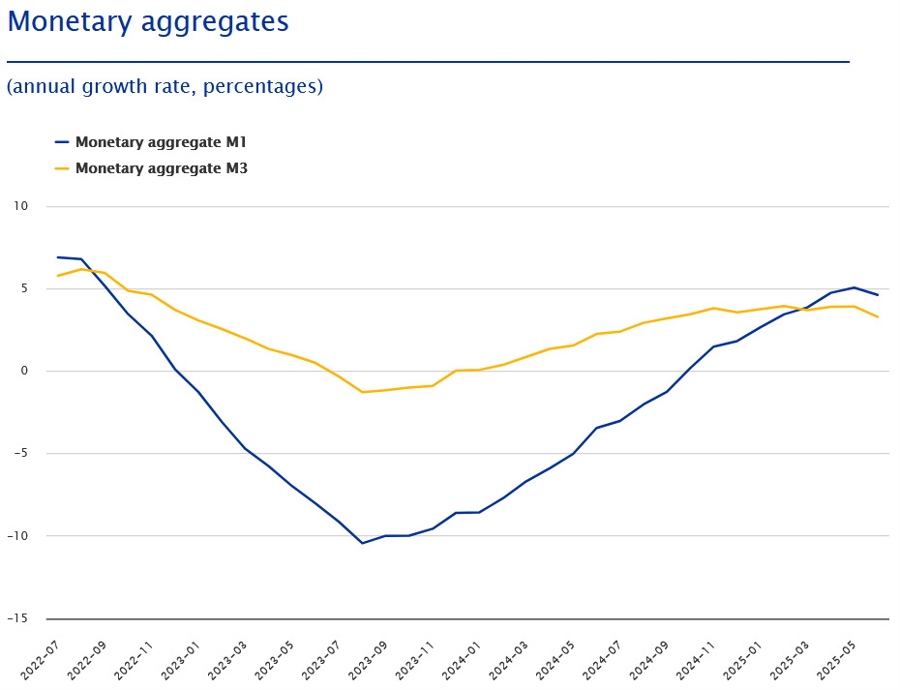

- Prior +3.9%

- Loans to households Y/Y +2.2% vs +2.0% prior

- Loans to companies Y/Y +2.7% vs +2.5% prior

This is not a market moving release. The money supply growth was expected given the ECB easing.

This is not a market moving release. The money supply growth was expected given the ECB easing.

Most Popular

Japan Reuters Tankan showed manufacturers sentiment rising to +18 (vs +13 prior), highest since 2021, while non-manufacturers held at +25. Outlook softened, with June seen at +14/+21 amid Middle East risks and weak external demand.

LKQ beats revenue but misses EPS, down 13%. FLWS, POOL, ADT also slide post-earnings.

Casino stocks mixed: PENN up 11% on revenue beat, FLUT down 11% despite growth. MCRI steady.

Bitcoin's Citi target cut to $112k, with 120% upside vs 25% downside risk.

BJ's dips 2% on missed EBITDA, TGT jumps 3% on strong EPS beat. COST leads with 9.2% revenue growth.

Iraq and the KRG agreed to resume oil exports via Turkey’s Ceyhan pipeline, offering limited supply relief as Hormuz disruptions slash output. The restart provides an alternative route, though global oil markets remain tightly constrained.

Big Tech's $720B AI spend fuels TSMC's growth. Its P/E of 23.6 is a discount, but risks remain.

Must Read