- Prior 48.8

Euro area manufacturing activity ticks up in January, moving closer to the growth threshold. Of note, manufacturing output increased in January for the tenth time over the past eleven months. However, the mood was slightly dampened by a fall in new factory orders since December. Overall, job losses also gathered pace but at least business confidence rose to its highest level since February 2022 while pricing power appeared to be limited amongst manufacturers in the region. HCOB notes that:

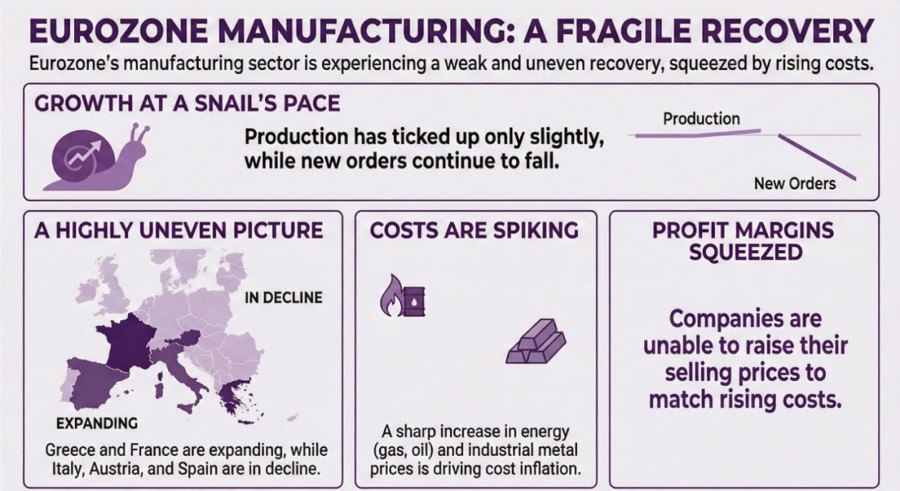

“Some progress can be seen in the manufacturing sector, but it’s happening at a snail’s pace. After dropping in December, production ticked up slightly at the start of the year, essentially continuing the growth path we saw between spring and fall last year. Order intakes haven’t been much help, though — they fell again, even if not quite as sharply as at the end of last year. Right now, it’s hard to say what might put an end to the ongoing rundown of inventories, which makes a strong shortterm upswing rather unlikely. Still, when looking twelve months ahead, companies are feeling a bit more upbeat than last month about expanding their production.

“There are some encouraging signs from Greece, France, and Germany. In Greece, growth in the manufacturing sector has picked up notably. In France, expansion has also gained momentum, and in Germany, December’s sharp slump has given way to only a mild decline. Italy, in contrast, paints a less optimistic picture, with the industry stuck in contraction territory. Next door in Austria, conditions have worsened significantly compared with the previous month. Spain, which had been in pole position among the four largest eurozone economies for most of the last two years, has seen its manufacturing industry decline for two straight months. All in all, this highly uneven picture across the eurozone is not exactly laying the groundwork for a sustained upswing.

“The noticeable rise in cost inflation stands out. The sharp increase in natural gas prices in January, and to a slightly lesser extent higher oil prices, likely played a role here. The spike in energy costs could prove temporary, as it seems largely tied to the unusually cold winter in Europe and the US. At the same time, a range of industrial metals became more expensive in January compared with the previous month, which, in itself, is not necessarily a bad sign, as it can point to stronger global industrial demand. But for companies relying on metals like copper, aluminium, or nickel, this - together with pricier energy - puts pressure on profit margins. They don’t appear to have the ability to raise their selling prices accordingly. In fact, their prices seem to be largely flat.”