- Prior +3.5%

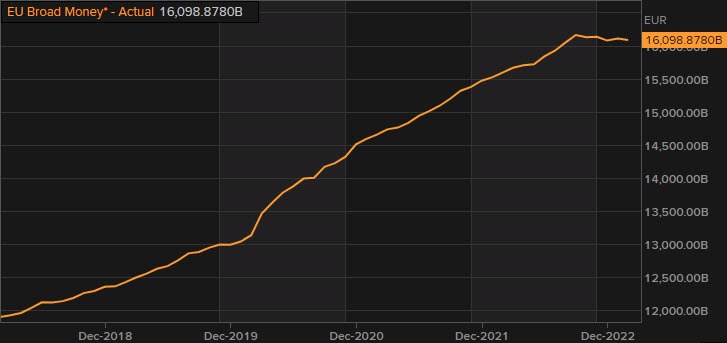

Broad money growth in the euro area continues to stagnate as the ECB drains up liquidity via their monetary actions but policymakers are reaffirming that banks in the region won't see a similar episode to SVB.

Broad money growth in the euro area continues to stagnate as the ECB drains up liquidity via their monetary actions but policymakers are reaffirming that banks in the region won't see a similar episode to SVB.