- Prior month 45.3

- Canada may manufacturing PMI 46.1

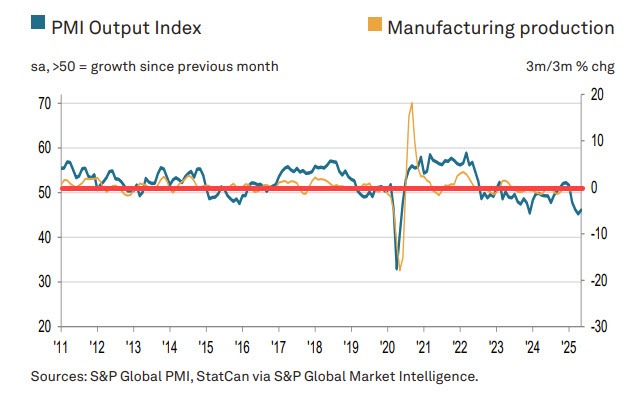

Looking at the details from the S&P global:

Headline PMI: 46.1 in May (up from 45.3 in April)

Below 50.0 for the 4th consecutive month → continued contraction

Production & Orders:

Output and new orders declined again; contractions remained steep

International demand especially weak; export orders fell more than domestic

Clients hesitant to place new orders due to tariff uncertainty

Inventories & Supply Chains:

Input and finished goods inventories cut further to reduce stock costs

Some firms dipped into inventories due to supplier delays

Vendor delivery times worsened again amid port congestion and customs delays

Prices & Inflation:

Input cost inflation accelerated, near March’s 31-month peak

Tariffs cited as key reason for higher input prices (e.g., livestock, metals, plastics)

Firms raised output prices, though the rate of increase was at a 3-month low

Employment & Capacity:

Job losses for 4th straight month; steepest since June 2020

Backlogs of orders declined but less sharply than in April

Spare capacity remains elevated

Purchasing Activity:

Purchasing volumes cut for 5th straight month (since January)

Contraction in buying reflects lower production needs

Business Sentiment:

Confidence remained subdued

Hopes for macro stability, but trade policy concerns dominate outlook

U.S. trade flows remain weak

Paul Smith, Economics Director at S&P Global Market Intelligence said:

"With manufacturers continuing to be hit by tariffs and trade uncertainty, May saw the sector experience a further significant contraction. Although declines were softer than in April, both production and new orders again fell to noticeable degrees amid reports that market demand was weak – again largely because of tariffs.

“Moreover, the hard to predict nature of trade policies means the outlook for production remains extremely uncertain and given the recent scale of the downturn in the sector, job losses are mounting. Indeed, latest data showed the steepest decline in employment since the height of the COVID pandemic in 2020 with spare capacity and rising costs also an increasing problem for many firms.

"Unsurprisingly, tariffs remain the primary source of price pressures, whilst also leading to an intensification of supply side delays. No wonder firms therefore remained circumspect in their purchasing and inventory management decisions during May, with the survey again revealing declines in both input buying and stocks."