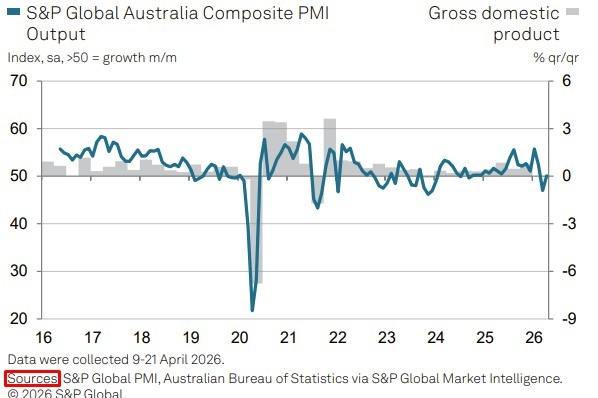

Australia S&P Global PMI composite (April 2026 preliminary): 50.1 (prior 46.6)

- Manufacturing PMI: 51.0 (prior 49.8)

- Services PMI: 50.3 (prior 46.3)

- New orders fall again, highlighting weak domestic demand

- Cost inflation hits highest since Aug 2022 on fuel, freight surge

Australia’s private sector returned to growth at the start of the second quarter, though the improvement masks ongoing weakness in demand and rising inflation pressures tied to the Middle East conflict.

Flash data from S&P Global showed the composite PMI rose to 50.1 in April from 46.6 in March, signalling a stabilisation in overall business activity after a sharp contraction the previous month. The move back above the 50 threshold indicates a return to marginal growth, but the underlying picture remains uneven.

The recovery was driven almost entirely by the services sector, where activity rebounded to 50.3 following a steep decline in March. Services firms reported a modest pickup in output and stronger hiring, helping lift overall activity. However, this rebound was relatively subdued, reflecting ongoing softness in demand conditions.

In contrast, manufacturing continues to struggle beneath the surface. While the headline manufacturing PMI edged into expansion territory, output has now declined for three consecutive months, pointing to continued weakness in the industrial sector. Order books, employment and inventory levels also showed declines, reinforcing the view that manufacturing remains in a retrenchment phase.

Demand conditions across the economy remain fragile. Total new business fell for a second straight month as heightened uncertainty linked to geopolitical tensions weighed on client activity. Domestic demand was particularly soft, although export orders showed a modest increase, supported by demand from key regions including North America, Asia and New Zealand.

At the same time, inflation pressures are intensifying. Input costs rose at the fastest pace since August 2022, driven by higher fuel and shipping expenses linked to disruptions in global supply chains. These pressures are increasingly being passed on to customers, with output price inflation accelerating to a multi-year high.

Supply chain conditions have also deteriorated, particularly in manufacturing, where delivery times lengthened at the fastest pace since mid-2022 amid shipping delays and logistical disruptions tied to the Middle East conflict.

Business confidence has weakened, falling to its lowest level in nearly two-and-a-half years, reflecting concerns over both demand and cost pressures. Despite this, firms increased hiring to work through existing backlogs, suggesting some resilience in underlying activity.

Overall, while the headline PMI signals stabilisation, the combination of weak demand, rising costs and supply disruptions highlights a fragile economic backdrop, with risks tilted toward stagflation-like conditions if pressures persist.

---

The report leans mildly stagflationary. Growth has stabilised but remains weak, while cost pressures are accelerating sharply due to energy and supply disruptions. This complicates the policy outlook, reinforcing expectations that central banks will remain cautious as inflation risks persist despite soft demand.

---