Australia’s manufacturing sector returned to contraction in March as demand weakened and cost pressures surged. Middle East-related supply disruptions and rising input costs weighed on activity, while confidence deteriorated sharply.

Summary:

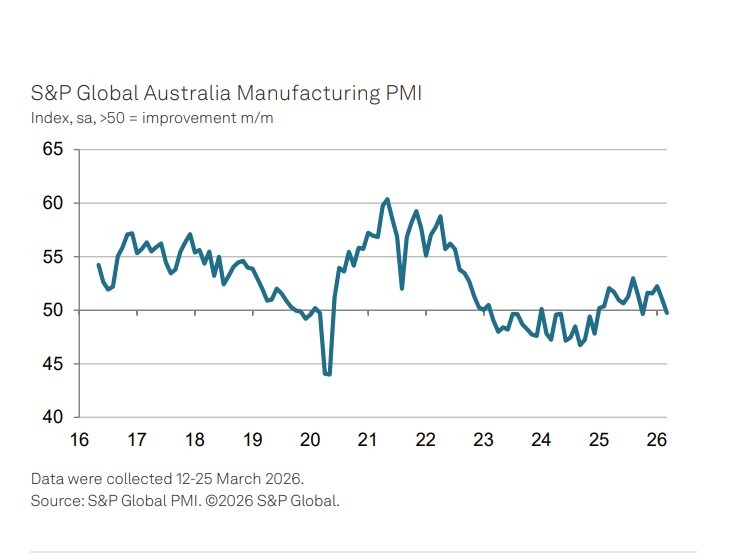

- Australian manufacturing PMI fell back into contraction at 49.8 (prev. 51.0) in March

- New orders declined for the first time in five months, signalling weakening demand

- Input cost inflation surged to a 3.5-year high, driven by energy and freight costs

- Supply chains deteriorated amid shipping delays linked to the Middle East conflict

- Business confidence dropped sharply to the lowest level in 20 months

Australia’s manufacturing sector slipped back into contraction in March, as weakening demand and intensifying cost pressures highlighted the growing economic impact of global geopolitical tensions.

The S&P Global Manufacturing PMI fell to 49.8 from 51.0 in February, dropping below the neutral 50 threshold and signalling a marginal deterioration in operating conditions. The decline was driven primarily by a renewed fall in new orders, which decreased for the first time in five months as customer demand softened and confidence weakened.

Production also declined for a second consecutive month, reflecting both weaker demand and ongoing supply-side constraints. Firms reported increasing difficulty sourcing materials, with supplier delivery times deteriorating sharply. Shipping delays, often linked to disruptions stemming from the Middle East conflict, contributed to longer lead times and reduced operational efficiency.

At the same time, cost pressures intensified significantly. Input prices rose at the fastest pace in three-and-a-half years, with higher oil prices feeding through to freight and fuel costs. Around 40% of surveyed firms reported rising input costs, underscoring the breadth of inflationary pressures across the sector. Output prices also increased, indicating that some of these costs are being passed on to customers.

Despite weakness in domestic demand, export orders remained a relative bright spot, rising at the fastest pace since mid-2021. However, this strength was insufficient to offset broader softness in overall activity.

Labour market conditions also deteriorated, with employment falling for the first time in five months as firms responded to lower workloads and rising costs. Purchasing activity and inventories declined, reflecting cautious business behaviour amid uncertainty.

Looking ahead, confidence weakened sharply, falling to its lowest level in 20 months. Firms cited concerns over the persistence of geopolitical tensions and their impact on demand and supply chains. While some manufacturers remain hopeful that exports and stabilising conditions could support a recovery, the near-term outlook remains highly uncertain.