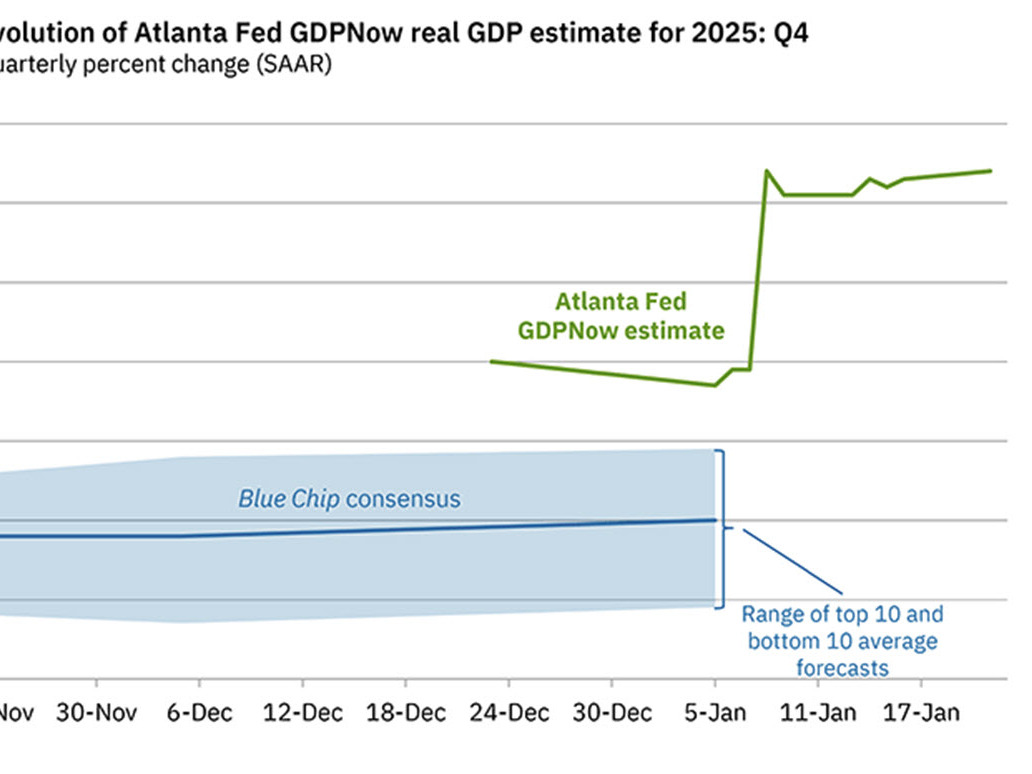

The latest Atlanta Fed GDPNow tracker is out and it's up to 5.4% annualized in the fourth quarter from 5.3% previously. It's a tough quarter to track because so much of the data has been screwed up by the long US government shutdown.

Today's construction spending numbers along with some recent data has been led to the change:

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2025 is 5.4 percent on January 21, up from 5.3 percent on January 14. After recent releases from the US Census Bureau, the US Bureau of Labor Statistics, and the Federal Reserve Board of Governors, increases in the nowcasts of fourth-quarter real personal consumption expenditures growth and fourth-quarter real gross private domestic investment growth from 3.1 percent and 5.1 percent, respectively, to 3.2 percent and 6.4 percent, were partially offset by a decrease in the nowcast in the contribution of net exports to fourth-quarter GDP growth from 1.99 percentage points to 1.88 percentage points.

The economists over at Pantheon Macroeconomics aren't buying it.

In a new note to clients, Chief US Economist Samuel Tombs called the forecast "highly questionable" and "far too optimistic."

The crux of the argument from Pantheon is that the GDPNow model is a black box that spits out a number without any "sensible judgment calls" on data quirks or shifting trends.

There is almost no hard data for December, very little for November, and even October has gaps. They remind us that at this stage in the game, the GDPNow model has a historical average error of 1.2 percentage points—and has missed by as much as 3.6 points in the past.

The real difficulty is that GDPNow is projecting 3.1% growth in consumer spending. Pantheon calls this "hard to fathom." Specifically, the model sees 1.8% growth in goods spending, while Pantheon’s own mapping and Bloomberg’s Second Measure indicator suggest spending on goods is actually flat.

Along the same lines, while the Fed model sees 3.7% growth in services spending, Pantheon’s "high-frequency indicators"—like hotel occupancy, TSA passenger counts, and even Google searches for "cancelling subscriptions"—suggest the sector is losing momentum.

Pantheon also notes a weird tension in the projections. The model assumes a massive 2.0 percentage point contribution from net foreign trade and a 0.8 point boost from inventories. Historically, these two usually move in opposite directions.

Trump was touting the quarterly annualized number as if it was an annual number today at Davos, but even if we do get 5.4% q/q annualized growth in Q4 and the Q3 number of 4.3% holds up (the final report is tomorrow), then that's only 3.16% GDP growth for the year. That's very good but it's not amazing.