First quarter economic grown, advance reading, is due today from the US at 1230GMT (Friday 27 April 2018)

- expected 2.0%

- prior 2.9%

Some bank expectations:

Barclays:

- We expect Q1 GDP to grow by 1.5% q/q saar, representing a slowdown from Q4.

- Incoming data during the quarter have suggested less momentum in activity, especially household spending on durables. In addition, some of the shortfall in Q1 growth is likely to be statistical - residual seasonality continues to hamper the BEA's estimate of Q1 data.

- We look for private consumption growth to rise by 1.0% q/q saar, and expect the drag from net exports to be almost fully offset by higher inventory accumulation.

Note - since this ealier preview Barclays have bumped up their forecast: Barclay raises GDP estimate for 1Q to 1.8% from 1.5%

Nomura:

We expect the first reading of Q1 real GDP growth to come in at 1.6% q-o-q saar, the first sub-2% print since Q1 2017.

- Consumer spending has been tepid over the past three months, contrasting somewhat with elevated consumer optimism and firm fundamentals. Thus, we expect somewhat soft PCE growth in Q1 to be largely temporary.

Besides weaker-than-expected personal spending, net exports and residential investment are likely to add some drag on growth.

- Imports in Q1 likely rose by a notable 8.5% while export growth decelerated to 2.1%, from 7.0% in Q4 2017.

- Residential investment likely pulled back as hurricane rebuilding efforts waned and new home sales softened. We expect non-residential investment to be mixed: a fall in equipment investment should be more than offset by positive contributions from structures and intellectual property products.

The largest contributor to Q1 GDP growth is likely to be a robust build-up in inventories.

- We expect that inventory accumulation overall will contribute 1.4pp to top-line GDP growth in Q1.

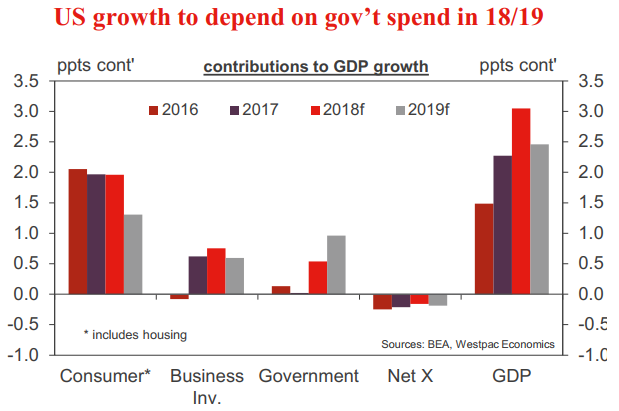

Finally, government spending likely picked up modestly in Q1, but we expect the quarters ahead will show much larger increases as the Congressional spending deal goes into effect.

Westpac:

- The detail of the Q4 GDP outcome was much stronger than the headline reading made out. This was true of the first estimate of 2.6% annualised as it was the third at 2.9%. In comparison, Q4 domestic final demand growth came in at 4.8% annualised, driven higher by strength across household consumption; residential investment; and business investment as well as an uplift in government spending.

- Come Q1 2018, a similar outcome is expected, circa 2.8%. However, the make-up of growth will be quite different. Retail and PCE data point to a soft consumer; and business investment has struggled to move higher. It is also likely too early for the government to add materially to growth.

- The component that is like to fill the gap is inventories which have exhibited strength of late. Domestic final demand is therefore likely to come in at 2.3% annualised - or lower.