In a note to clients today, Deutsche Bank argues that there

is a new reason for traders to stay bullish on the USD and expresses

that via EUR/USD short positions. According to DB, a new

dollar-supportive driver is emerging beyond the widely understood

central bank divergence story: the rising cost of dollar funding.

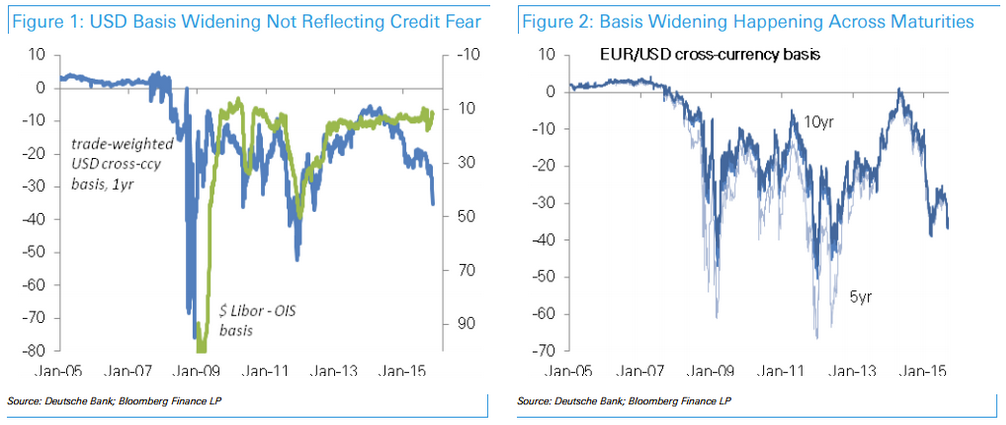

"Over the last few weeks the cross-currency basis, representing the

additional cost of borrowing dollars in the FX swap market over and

above the rate differential, has ballooned to the highest since 2011,"

DB notes.

DB outlines 4 important nuances to this phenomenon that are worth mentioning.

"First, the widening is happening against multiple

currencies, in contrast to previous episodes that have been mostly

focused on the yen or euro.

Second, widening basis does not seem to be driven by

rising credit risk, similar to Lehman and the Eurozone crisis.

Alternative credit metrics such as the USD Libor-OIS spread have

remained very well-behaved.

Third, the move seems to go beyond traditional

year-end funding constraints because even longer-dated cross-currency

basis has widened out.

Fourth, the cross-currency basis move is coming at a

time when US rates are rising for the first time since the end of the

financial crisis while everyone else is at zero. This matters because

the low starting point of rates means the proportionate impact of a

widening basis on the rate differential can be big," DB clarifies.

"Overall, a combination of year-end funding constraints, lack

of liquidity, regulatory pressure nd precautionary demand for dollars

ahead of FOMC liftoff seem to all be driving the move in the basis

...This adds to the bullish dollar view, on top of the

fact that traditional metrics such as the real rate differential already

point to a move down to parity in EUR/USD," DB concludes.