Australian capital expenditure result for Q3 and projections ahead are due from Australia on Thursday 28 November 2018 at 0030GMT

The data is another input to Q3 GDP (due on December 5), which has already gotten off to a shaky start this morning here:

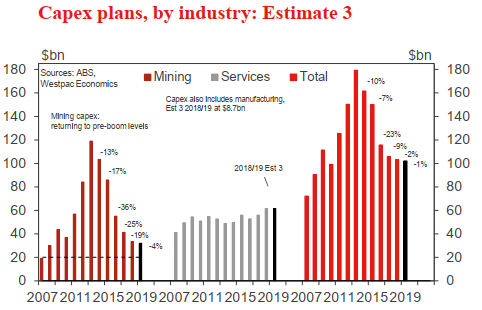

Via Westpac, on what to expect for the headline private capex.

Firstly, on its recent path:

- Private business capex spending was mixed over the first half of 2018, down 2.5% in Q2 after a 1.2% rise in Q1.

- This followed a 4.2% rise in capex in 2017, after four years of decline, on a diminished drag from the mining investment wind-down and with non-mining investment trending higher.

For Q3

- we expect a soft result, up only 0.4%

- Building & structures is expected to be broadly flat.

- Equipment spending is forecast to rise by 0.8%, reversing a 0.9% fall in Q2, to be 5% above the level of a year ago - supported by rising profits and higher capacity utilisation levels. Service sectors are lifting spending but growth is choppy and the underlying pace is modest of late

And, ahead, plans for expenditure 2018/19:

- the 4th estimate of capex spending plans for 2018/19.

- Est 3 for 2018/19 was $102bn, some 1% below Est 3 a year ago. … mining capex in 2018/19 being lower than in 2017/18 (with the completion of the gas projects) and broadly flat capex across the non-mining economy.

- For Est 4 on Est 4 to be at -1% (matching the Est 3 outcome) would require an upgrade of 6% to $108bn - an upgrade which is in line recent historical experience, including last year. Accordingly, an Est 4 of $108bn is plausible, with risks potentially tilted to the upside.

- Our central case forecast is for business investment to edge higher in 2018/19, up 1%. This is supported by sectors (education and health) and assets (computer software) excluded from the capex survey. That is, the capex survey understates the outlook for business investment.