Forex and Bitcoin news for Asia trading Thursday 31 May 2018

- China Com Min says it'll ease restrictions on foreign investment into some sectors

- China Commerce Ministry on US trade tensions - warns on countermeasures …

- More Australian data (from earlier): Private sector credit for April +0.4% m/m (in line)

- AUD - Australian Q1 Capex, headline 0.4% (vs. expected at 1.0% q/q)

- PBOC sets USD/ CNY reference rate for today at 6.4144 (vs. yesterday at 6.4207)

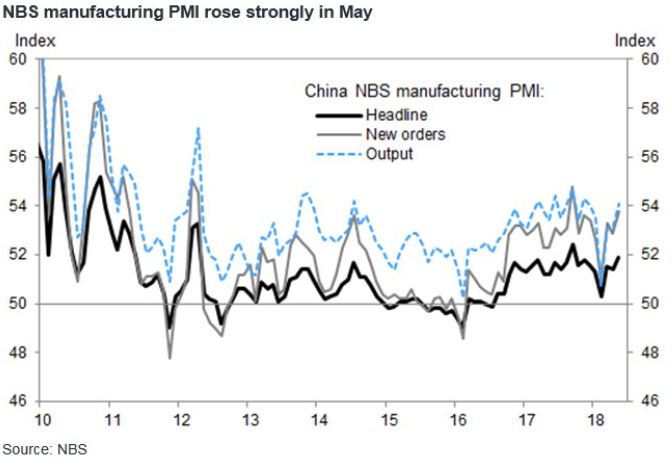

- China manufacturing PMI for May 51.9 (vs. expected at 51.4)

- NZ data - Business confidence for May: -27.2 (prior -23.4)

- Japan - Industrial Production for April, flash: +0.3% m/m (expected 1.4%)

- Reports that North Korea's Yongbyon nuclear research complex is still active

- GBP data - Lloyds Bank's index of business confidence up to 35 (from prior 32)

- UK - GfK Consumer Confidence for May: -7 (vs. expected -8)

- Trump to impose metal tariffs on Canada, Mexico & the EU says the Washington Post

- Trade ideas thread - Thursday 31 May 2018

May is drawing to a close with a whimper on forex markets here in Asia today with not a lot of movement. We got some relevant news and data hitting but despite this moves in FX were minor only.

Early on a report in US media that President Trump is set to impose metals tariffs on Mexico, Canada and Europe as soon as Friday (announcement expected Thursday see bullet above for more). MXN lost ground but CAD and EUR didn't move nearly so much.

There were also reports that North Korea's Yongbyon nuclear research complex is still active, but the impact of the item (yen appreciated a little early in the session, seeing USD/JPY below 108.60) was muted somewhat by being based on satellite imagery date May 6. Again, see bullet above for more (including pic of the Trump / Kim summit! Yes, srsly!). Data from Japan today showed a miss on flash IP numbers (for April).

Official PMIs from China today - both the manufacturing and non-manufacturing came in at beats, and a solid result indeed. Goldman Sachs were impressed:

Also from China we got some balanced comments from the Commerce ministry on US trade actions (see bullets above) - balanced in the sense that they expressed a degree of warning but also conciliatory comments alongside.

From Australia it was the day of the much awaited capex data 9for Q1 of 2018); not only does the data contain in input to first quarter GDP (for publication on June 6 ... can't wait!) it also provides information on how investment plans are coming along. In a nutshell the data was softer than expected and weighed somewhat on the Australian dollar after release (despite the positives from China's PMIs).

GBP/USD has had a decent session, its up nearly 30 points and testing its overnight US high as I update. there was some minor data today and no particularly relevant news I have seen.

EUR, CHF, CAD, NZD … all relatively sedate against the USD today.

Still to come: