Due at 0130 GMT,GMT, Australian labour market report for May

- Employment Change: K expected 19.0K, prior 22.6K

- Unemployment Rate: % expected 5.5%, prior 5.6%

- Full Time Employment Change: K prior was +32.7K

- Part Time Employment Change: K prior was -10.0K

- Participation Rate: % expected 65.6%, prior was 65.6%

I posted an earlier preview here (via ANZ):

This now via …

(bolding mine)

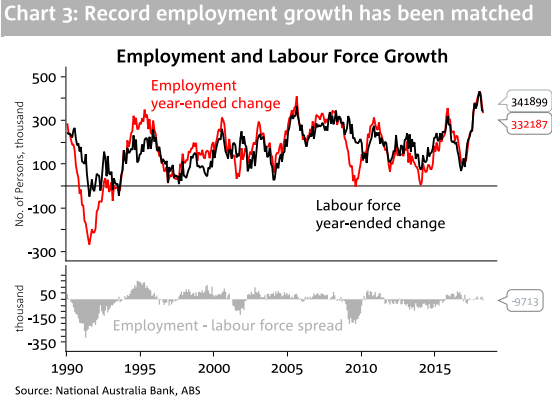

NAB:

- Last month saw stronger-than-expected employment growth of 22.6k (mkt: 20k), but a tick up in the unemployment rate to 5.6%.

- Despite a series of upside surprises on employment growth, the unemployment rate has tracked sideways over the past year, still hugging 5.5%. Forecasts from the RBA, Treasury (and NAB) look for a clear decline in unemployment over the year ahead- a necessary pre-condition for stronger wages growth. It's the sharp rise in the participation rate that has surprised markets and the RBA. While the number of people employed and the size of the labour force tend to be highly correlated, both have grown sharply (nearly one-for-one) over the past year.

- This month, NAB expects May employment growth to soften to 15k, but the participation rate to remain unchanged at 65.6%. Given these numbers, the unemployment rate is expected to remain at 5.6%.

Also contained in the May Labour Force data is the quarterly update on the underemployment rate, another key measure of labour market slack. The underemployment rate has declined slightly over the past year to 8.4%, but remains around 1ppt higher than where its historical relationship with unemployment would suggest. Further, some models of wages growth suggest that underemployment may be a more useful measure of labour market slack- so markets will be watching how this variable moves in the May data.

CBA:

- The May labour force numbers will include a quarterly reading of underemployment.

- Despite good jobs growth over the past 18 months or so the unemployment rate remains stuck around 5½% and underemployment is elevated. The leading indicators of employment are solid and suggest decent jobs growth over the next six months or so.

RBC:

- Job creation has been slowing thus far in 2018 and is now a far cry from the consistent 30k+ gains of mid 2017. That said, we expect labour market conditions to remain mostly favourable this year, and residual momentum from forward-looking indicators including vacancy rates/job ads suggests that some strength should still be seen in May, despite a recent fall in leads which may impact later reads.

- After two negative prints in February and March, we expect a second month of ~20k gains, with unemployment down a touch to 5.5% and the part rate steady at 65.6%.