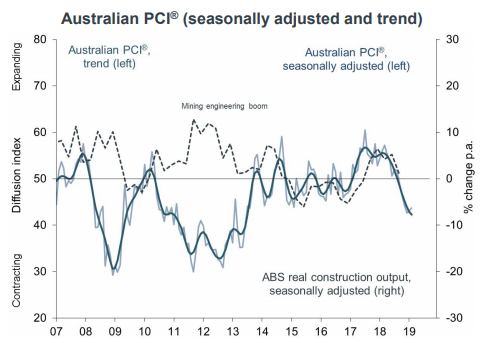

This is the Australian Industry Group Performance of Construction Index for February

Comes in at 43.8, an improvement on the month and still deep in contraction territory

- from January's 43.1

Major points:

- milder contraction ... reflected less pronounced falls in activity and employment

- both new orders and deliveries from suppliers contracted at slightly steeper rates … businesses attributing this to overall sluggish demand conditions

- All four sectors … contracted in February

- Weighing heavily on industry conditions was continued weakness in the house and apartment building sectors where rates of decline in new orders were the most marked since mid-2013.

- Commercial construction fell further into negative territory while engineering construction declined for a third month due to a shallower pool of new work to replace completed and more advanced projects.

- Residential building respondents to the Australian PCI mainly commented on slow market conditions due to soft new orders, tight lending conditions, falling prices and caution by prospective buyers.

---

Earlier in the month we had the other PMIs:

- Australia Manufacturing PMI (Feb): 54.0 (prior 52.5)

- Australia manufacturing PMI (CBA /Markit, February final): 52.9 (prelim was 53.1)

- Australia - AiG Performance of Services Index for February 44.5 (prior 44.3)

- Australia CBA / Markit services PMI for February, final: 48.7 (prelim was 49.3)

I had a bit of a moan about the services PMIs, specifically about how the market tends to ignore them despite services being the bigger part of the economy than manufacturing. I think you might all agree, given the AUD moves we've had this week, that the contraction-level services PMIs were a nice heads up.