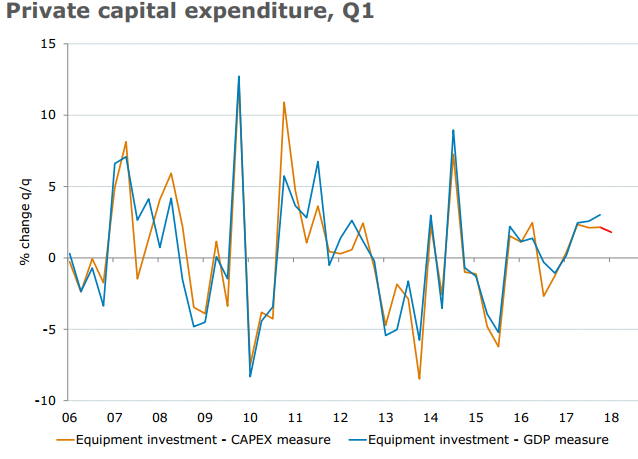

Capital expenditure (capex) for the first quarter (January - March 2018)

Due at 0130 GMT

'Headline'

- expected +1.0% q/q, prior -0.2%

Some bank previews, via....

ANZ:

- We believe capital expenditure rose only fractionally in Q1.

- We expect the key input to GDP from the release - plant and machinery spending - to record solid growth; although the softness in non-residential building this week is expected to weigh down the headline number.

- We also expect a solid upward revision in firms' spending plans for 2018-19, given the strength in business conditions and business survey reports of rising capacity utilisation. We will release a detailed capex preview on Monday

CBA:

- The first estimate of 2018/19 capex plans came in at $84bn. The figuring implied a lift in non-mining investment of around 6% when compared with 2017/18 and a fall in mining capex of around 6%. All up, a modest lift in total nominal investment of around 3% (note that the capex survey excludes a number of large and important industries which include agriculture, health and education).

- Second estimates for spending plans can vary significantly from actual spending. A comparison of previous second estimates with actuals shows that non-mining firms will almost always underestimate their capex plans at both their first and second stabs. But the magnitude of the miss can vary greatly in any given year. We consider a second estimate that comes in larger than $63bn as an upgrade on the first estimate and also a good outcome. Less than $63bn would imply a downgrade.

- Non-mining investment has lifted over the past 1½ years and policymakers will want to see that trend continue, particularly as the unemployment rate has been stuck at 5½% over the past 9 months. The last reading from three months ago implied a 4% increase in nominal capex this financial year. The detail suggested a fall in mining capex of 5% and a solid 8% increase in non-mining investment. We anticipate that we won't see too much change in the estimate for mining capex. But we expect an upgrade in non-mining investment of around 3%.

- We consider a sixth estimate that comes in larger than $118bn as an upgrade on the fifth estimate. Less than $118bn would imply a downgrade. We expect the actual volume of Q1 capex to rise by 1.5% after a 0.2% fall in Q4 2017. Such an outcome would leave annual growth 4.3% higher.

- The actual spending data will help us to firm up our estimates of Q1 GDP (due 6 June). While employment growth has eased, the business surveys remain strong. And job vacancies continue to lift in the resources sector. On balance, these factors point to some modest upside risk on our forecasts for 2018/19 capex expectations.